You've got an offer in hand. The salary is solid. The product is interesting. The team looks sharp. Then you reach the equity line and the confidence drops a notch.

The offer says you're getting options. Maybe it lists a share count, a strike price, and a vesting schedule. Maybe it doesn't. Either way, the hard question is the same: should this change how you value the job?

For most tech professionals, private company stock options sit in an uncomfortable middle ground. They're too important to ignore, but too easy to overestimate. They can absolutely matter. They can also become an expensive spreadsheet artifact if you don't understand the mechanics, the taxes, and whether the company has a believable path to liquidity.

That gap between “this could be meaningful” and “what is this worth to me?” is where bad decisions happen. People anchor on a big option number, compare it to nothing, and assume future upside will sort itself out.

Historically, options were never a standard benefit across the whole labor market. In 1999, grants of stock options were made to 1.7% of all private-sector workers, which shows how selective equity compensation already was in practice, especially in firms using it to attract talent without paying all-cash compensation upfront, according to the U.S. Bureau of Labor Statistics National Compensation Survey.

Private company stock options still work that way. They're a recruiting tool, a retention tool, and sometimes a real wealth-building tool. But only if you know how to interrogate the offer like an operator, not like a hopeful bystander.

A common version of this story goes like this. You're talking to a startup that's clearly trying to hire above its weight class. The company can't match late-stage or public-company cash, so it leans on mission, growth, and equity.

Then the recruiter says something like: “We're offering 10,000 options at a $1.50 strike price.”

That sounds precise. It feels valuable. It also tells you almost nothing by itself.

The share count is the easiest part of the package to misunderstand. A large number of options can feel impressive because humans are bad at evaluating denominators they can't see. If you don't know the company's total share count, the current common share value, the option type, and the rules for exercising, you can't tell whether the grant is generous, average, or cosmetic.

Early in a career, many people treat startup equity like a lottery ticket. Later, after seeing a few companies miss milestones or remain private for years, they start treating it like a contract with operational, tax, and liquidity terms attached.

Private company stock options are less like bonus cash and more like a right you may be able to turn into value later, under specific conditions.

The point isn't to become a tax lawyer before signing an offer. The point is to understand what trade you're making.

If you're accepting lower cash in exchange for equity, you're taking concentrated risk in a company where your paycheck, your career momentum, and part of your potential upside all ride on the same outcome. That can be a very rational move. It can also be a bad bargain if the grant is small relative to the risk or if the company has no realistic liquidity path.

A useful mindset is to treat equity as one part compensation, one part financing decision, and one part bet on execution. You're not just asking, “How many options am I getting?” You're asking, “What would have to happen for these to become real money, and do I believe this team can get there?”

Options are easiest to understand if you stop thinking about them as stock and start thinking about them as a ticket with rules.

The company gives you a ticket that may let you buy shares later at a fixed price. Whether that ticket becomes useful depends on timing, vesting, and whether the company's stock becomes worth more than the price you're allowed to pay.

Here's the practical translation of the jargon you'll see in an offer letter.

Two more pieces often matter just as much as the headline grant.

First is the cliff. Many grants don't vest gradually from day one. Instead, nothing vests until you hit a specific milestone in tenure, after which a larger chunk vests at once and the rest continues on schedule.

Second is the post-termination exercise window. If you leave the company, you may have a limited period to exercise vested options. If that window is short and the exercise cost is meaningful, you can end up forced to choose between writing a large check for illiquid shares or walking away.

Practical rule: If your offer letter doesn't make the strike price, vesting schedule, option type, and exercise window obvious, ask for the details in writing before you sign.

A plain-English primer like Underdog's startup equity basics for job seekers is useful here because it helps translate the offer into the questions you need to ask.

Use this sequence:

If any one of those answers is missing, you don't yet understand the offer.

A common startup mistake goes like this: someone hears “they're ISOs,” assumes that means “better,” and stops asking questions. Then they leave the company, lose ISO status after termination, face a tax bill they did not expect, or realize they never had the cash to exercise in the first place.

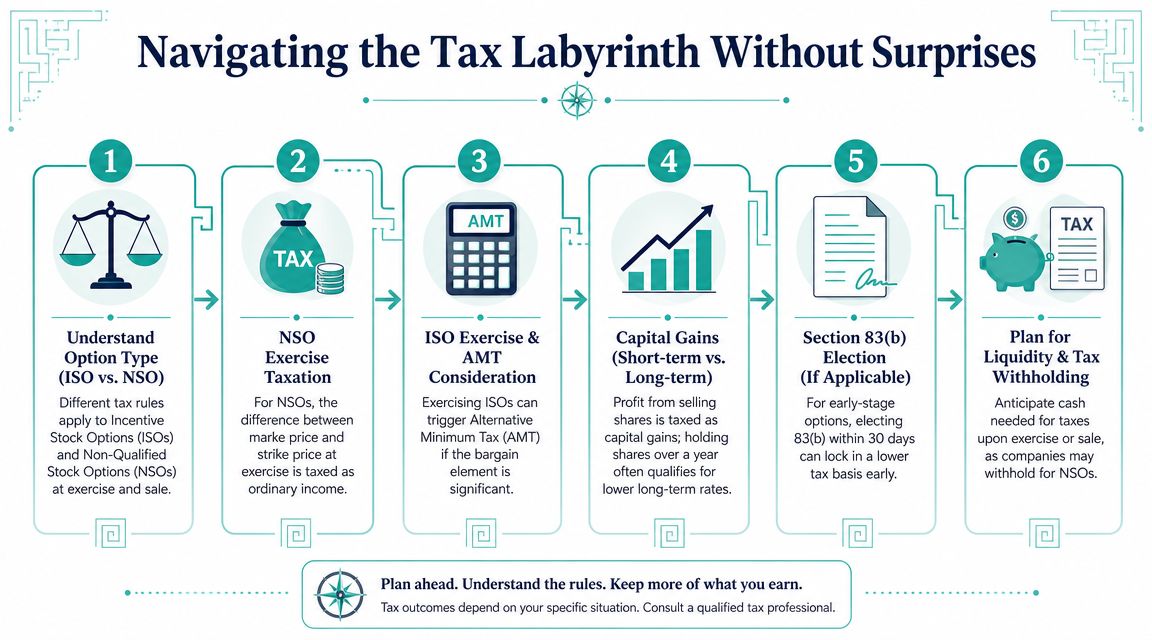

ISO vs NSO is not a prestige label. It tells you how the option behaves under tax rules and who can receive it. That matters because the same share count can lead to very different cash needs, tax timing, and decision pressure.

Incentive stock options (ISOs) are a U.S. tax-law category for employees only. If you exercise them and satisfy the required holding periods, the eventual sale may get capital gains treatment rather than ordinary income treatment. That upside is real. So is the catch. ISOs come with more conditions, and they can create Alternative Minimum Tax exposure even when you have not sold the shares.

Non-qualified stock options (NSOs) are more flexible. Companies can grant them more broadly, including to contractors or advisors in many cases. The trade-off is that the tax hit usually shows up sooner. In plain terms, NSOs are often simpler to issue, but they can be less forgiving for the person exercising them.

| Feature | Incentive Stock Option (ISO) | Non-Qualified Stock Option (NSO) |

|---|---|---|

| Who can receive it | Employees only | Employees and other service providers |

| Main tax angle | May get favorable treatment if the holding rules are met | Spread at exercise is generally taxed as ordinary income |

| Exercise risk | Can trigger AMT before any liquidity event | Can trigger a regular tax bill at exercise |

| If you leave the company | Often converts to NSO treatment if not exercised within the ISO window | No ISO-status issue, but the exercise window still matters |

| Best fit | You expect growth, can fund exercise, and can afford to hold | You want fewer ISO-specific rules, but still need to plan for taxes |

For a job candidate, the practical question is not “Which one sounds better?” It is “What decision will this force me to make later?”

ISOs can be attractive if the strike price is low, the company still has room to grow, and you have enough cash to exercise without putting your personal balance sheet in a bad spot. They reward patience, but they also ask you to take more risk earlier. You may need to buy and hold illiquid shares for a long time to get the better tax outcome.

NSOs are often more straightforward conceptually. You exercise, and the tax consequences are usually easier to identify. But easier to identify does not mean easier to afford. If the spread between strike price and current fair market value is large, exercising NSOs can feel like getting paid and taxed on money you cannot spend yet.

That is why option type belongs in the same conversation as company stage, exercise window, and your own cash reserves. A useful startup equity calculator for job offers can help you model the exercise cost and ownership outcome, but it will not remove the core trade-off: paying now for something that may stay illiquid for years.

One more nuance matters. Option type does not tell you whether the grant is economically good. A mediocre grant can be packaged as ISOs. A strong grant can be packaged as NSOs. The better test is whether the percentage ownership, strike price, post-termination terms, and company valuation make sense together. If you need a refresher on how valuation frames that conversation, Jumpstart Partners' valuation guide is a useful reference.

Ask these questions before you sign:

A strong answer on option type is not “these are ISOs, so you're good.” A strong answer is specific enough that you can estimate the cost, the tax timing, and the downside if the company never reaches liquidity.

A candidate gets 20,000 options from one startup and 5,000 from another, then assumes the first offer is richer. That conclusion is often wrong.

Option count is the easiest number to remember and the least useful one to compare across companies. A grant only starts to mean something when you know how much of the company it represents, what price you would pay to buy the shares, and how that pricing relates to the company's current valuation.

Ask one question early: what percentage of the company does this grant represent on a fully diluted basis?

Fully diluted means the denominator includes the shares and share-like claims that matter to actual ownership, not just the currently issued common shares. Founders, investors, the option pool, and other outstanding rights all count. If your recruiter or hiring manager can only give you the raw option count, you are missing the unit that makes comparison possible.

Share count works like saying you own one slice of pizza without telling you whether the pie was cut into 6 slices or 600,000.

This is also where candidates get tripped up by headline numbers. A large grant at a company with a huge capitalization can leave you with less ownership than a smaller grant at an earlier-stage startup. For career decisions, percentage is usually the better lens because it lets you compare upside across very different cap tables.

Private companies usually rely on a 409A valuation to set the fair market value of common stock, which is what helps determine your strike price. For you, the practical question is simple: how expensive will it be to buy these shares if you choose to exercise?

Candidates often mix up three different numbers:

Those numbers serve different purposes. Investor pricing reflects the terms investors negotiated. Your 409A is part of the company's process for pricing common stock for employee equity. They are related, but they are not interchangeable.

That distinction matters because a company can announce an impressive valuation and still grant options with economics that are less attractive than they first appear. If you want a clean refresher on how financing valuation works, Jumpstart Partners' valuation guide is a useful reference point.

You do not need the whole cap table to pressure-test an offer. You need a few answers that management should be able to provide without drama.

Each answer changes the story. A low strike price can make exercise affordable. A stale 409A can mean the current pricing no longer reflects the company's actual stage. A planned option pool expansion can dilute employees after they join, even if the grant looked solid on day one.

If you want to compare two offers side by side, use a startup equity calculator for job offers once you have those inputs. The calculator will not tell you whether the company wins, but it will force the offer into numbers you can compare.

They do not compare grants by share count alone. They compare ownership, strike price, likely dilution, and how believable the path to liquidity is.

They also do not treat internal valuation numbers as spendable wealth. Private company options are an opportunity with conditions attached. The value on paper can change, the exercise cost is real, and the timeline to cash may be much longer than the recruiting pitch suggests.

That is the essential task here. Translate a flattering share count into ownership, cost, and risk before you sign.

Vesting means you've earned the right. Exercising means you decide to use it.

That distinction matters because people often say “I have equity” when what they possess is vested or unvested options that still need a separate decision, and usually money, to convert into shares.

The core calculation is simple:

number of vested options × strike price = exercise cost

If you've vested in options and the strike price is low, the cost may feel manageable. If you've been at the company long enough to vest a large portion, the exercise cost can become substantial. That's before taxes or transaction fees enter the picture.

You should also confirm what your company's exercise process looks like. Some use specialized equity platforms. Some still require old-school forms and approvals. Operational sloppiness here is a real risk because deadlines matter.

There isn't one correct answer to “When should I exercise?” There are trade-offs.

Some people exercise earlier because the total purchase cost is lower when fewer options have vested, or because they want to start the clock on potential holding periods. Others wait because they don't want to spend cash on illiquid private shares in a company whose outcome is still uncertain.

That decision sits at the intersection of conviction, cash, and tax exposure.

Don't exercise just because your shares are “in the money” on paper. In a private company, paper value and spendable value are different things.

The most painful surprises often happen after someone resigns.

A former employee may have a meaningful block of vested options and suddenly discover there's a narrow post-termination window to exercise them. That creates a brutal decision under time pressure. Write a check for stock you can't easily sell, or let the options lapse.

Review these terms before you join:

Good planning is boring and specific. Keep a copy of your grant documents. Track vesting dates. Know your deadlines before you need them. If the company grows quickly, revisit the exercise decision periodically instead of saving all thinking for the week you leave.

Most expensive option mistakes don't come from ignorance of finance theory. They come from delay, assumptions, and documents nobody read carefully enough.

Tax is where startup equity stops being abstract.

This is also where a lot of smart employees make preventable mistakes because they confuse “I haven't sold anything” with “I definitely don't owe anything yet.” Sometimes that assumption is right. Sometimes it's very wrong.

The first source of confusion is that tax timing can differ between option types. With NSOs, tax consequences often become visible when you exercise. With ISOs, people hear “favorable tax treatment” and stop listening too early.

The second source of confusion is that private-company illiquidity doesn't protect you from every tax issue. You can end up with a tax problem tied to shares you still can't sell easily.

The attractive part of ISOs is real. Under the ISO framework described by Nasdaq Private Market and summarized earlier, gains may receive long-term capital gains treatment if the statutory holding periods are met. But that doesn't mean every ISO exercise is painless.

The practical problem is cash planning. If you exercise into private shares, you may need money for the exercise itself and money for any related tax exposure while still holding an illiquid asset.

That's why tax review should happen before exercise, not after.

You don't need to become your own CPA. You do need a pre-exercise checklist.

If you're trying to organize option documents, grant records, and tax forms before that conversation, a tool like Finance Tax Document Analyzer can at least help you pull key details into one place for review.

A paper gain can still create a real cash planning problem. Treat exercise as a tax event review, not just a portfolio decision.

Keep the questions simple and direct:

| Question | Why it matters |

|---|---|

| What tax consequences might apply if I exercise now? | You want timing clarity before acting |

| What happens if I hold the shares after exercise? | Holding can change risk and tax outcomes |

| Do I need to reserve cash beyond the strike price? | Exercise cost is often only part of the total |

| What records should I keep for later sale reporting? | Missing documentation creates avoidable pain |

A good advisor won't promise a magical answer. They'll help you understand scenarios, deadlines, and the cash you need to stay out of trouble.

You join a late-stage startup, vest for four years, and your equity dashboard shows a healthy paper gain. Then you ask the key question. How do you turn any of it into cash?

That is the liquidity problem.

Private company options are not like public-company shares you can sell on Tuesday if you need the money by Friday. They work more like a lottery ticket with company-controlled rules on when, whether, and how you can cash out. For a job candidate, that changes how you should value the grant. A large option package with no credible path to liquidity can be less useful than a smaller grant at a company that has already created employee sale opportunities.

Employees usually anchor on three outcomes:

Each path has different consequences for timing, control, and price.

An IPO can create liquidity, but often not immediately. An acquisition can produce cash fast, but the details may be worse than employees expect if the deal price is disappointing or some equity is rolled over. A secondary can be the most practical option in a long-lived private company, but companies do not have to offer one, and they often limit who can sell and how much.

Do not stop at, "What is this grant worth today?"

Ask, "What has to happen before I can sell, and who controls that decision?"

That one question gets you closer to the actual value of the equity than another round of math on share count. In permanently private companies, illiquidity can drain the practical value of options because exercising may only convert one restricted asset into another. NASPP makes that point in its discussion of equity compensation for companies that never go public.

Candidates should listen for specifics.

This is one of the few equity topics where company behavior matters more than recruiting language. If leadership says, "We expect to be public eventually," that is not a liquidity policy. If they say, "We ran a tender offer last year and expect to review employee liquidity annually," that is a usable data point.

A company that stays private longer may keep compounding in value. It may also leave employees holding an asset they cannot sell when they want to. Founders and investors can tolerate that better than many employees can, because their balance sheets, timelines, and ownership levels are different.

That is why I treat liquidity as part of job-fit, not just upside. If you are considering a startup partly because the equity could help fund a house down payment, cover family obligations, or materially change your net worth, you need more than a hopeful exit story. You need evidence that the company has thought through employee liquidity as an operating issue.

If you are still in offer-stage discussions, it helps to review how to negotiate stock options in a startup offer before you accept the default framing.

Ask questions a recruiter or hiring manager can take back to finance or legal:

Those answers will not predict the future. They will tell you whether the company treats employee equity like compensation with a cash path, or just a retention story with a spreadsheet attached.

A startup offer with equity is not something you accept on vibes. It's a package you interrogate.

The companies worth joining usually won't mind serious questions. In fact, good operators expect them.

Use this list directly in the process.

This part matters just as much.

| Self-check | Why it matters |

|---|---|

| Would I take this job if the equity ended up worth little or nothing? | It keeps you honest about the role itself |

| Could I afford to exercise if needed? | A grant isn't useful if you can't act on it |

| Am I comfortable with concentrated risk? | Your salary and upside may depend on the same company |

| Do I understand the tax implications well enough to plan? | Confusion gets expensive fast |

If you want a negotiation-specific framework, Underdog's guide to negotiating stock options is a practical reference for framing the discussion around grant size, ownership, and the company terms that move value.

A good equity grant can be meaningful. A vague equity grant is just narrative until proven otherwise.

Treat private company stock options like any other serious financial decision. Ask for the denominator. Ask about the exercise window. Ask about liquidity. Ask what happens if things go well, and what happens if the company stays private far longer than anyone hopes.

Then decide with open eyes.

If you're exploring startup roles and want a clearer view into how early-stage companies structure compensation, Underdog.io is a curated marketplace where tech candidates can get introduced to vetted startups and compare opportunities, including the equity side of the offer, with more context than a typical job board.