A startup equity calculator translates the confusing numbers in your offer letter — share counts, strike prices, vesting schedules, and dilution — into concrete projected dollar values across different exit scenarios. This guide walks through every key input, shows how dilution actually works in your favor during funding rounds, runs a full step-by-step worked example, and covers the advanced factors like liquidation preferences and cap tables that determine what you actually walk away with.

That startup offer in your inbox is exciting, but the equity part? It can feel like trying to read a foreign language full of terms like stock options, vesting schedules, and strike prices. It’s often the most compelling part of the package, but also the most confusing.

This is exactly where a startup equity calculator comes in. It’s the tool that translates all that abstract jargon—the share counts, the percentages, the fine print—into something tangible: potential dollar values.

A startup equity calculator is a financial modeling tool that converts the abstract figures in your equity grant into real projected dollar values across a range of future exit scenarios.

When you receive a startup offer, the equity section typically reads something like: "25,000 stock options at a $2.00 strike price, vesting over 4 years with a 1-year cliff." Those numbers mean very little in isolation. A startup equity calculator takes them and answers the question you actually care about — what could this realistically be worth?

You input your grant size, strike price, the company's current valuation, and the total number of fully diluted shares. The calculator then models your stake's value at different exit valuations — say, an acquisition at $200M or an IPO at $1B — while accounting for dilution from future funding rounds. The output is a clear, data-backed spectrum of possible financial outcomes that lets you compare offers objectively, negotiate from a position of knowledge, and make a major career decision with your eyes wide open rather than on gut feel alone.

A job offer from a high-growth startup is more than just a salary. The real X-factor is the equity grant, that promise of a slice of the company's future success. But figuring out what that slice is actually worth is another story entirely.

Think of it like this: your equity grant isn't a check. It’s more like a complex financial instrument with its own set of rules. A startup equity calculator acts as your personal financial modeler, allowing you to peek into the future and see what your stake could be worth under different growth scenarios. It helps you see beyond the initial numbers and analyze the true potential of your offer.

Before we dive into the calculator itself, it helps to have a quick reference for the terms you'll be plugging in. These concepts are the building blocks for understanding your equity's value.

Think of this table as your cheat sheet. These are the core variables that a calculator uses to project your potential financial outcomes.

Just knowing you've been granted 10,000 options or 0.1% of the company isn't enough. The real value is hidden in the future, and a calculator is what helps you model those potential outcomes. Here’s why it’s so critical:

Understanding how to model your equity's future worth isn't just a bonus skill; it's fundamental for anyone serious about building wealth in the tech industry. It shifts your perspective from being a passive recipient of an offer to an active analyst of your financial future.

Of course, before you can start plugging numbers into a calculator, you need a solid grasp of the mechanics behind stock options. If you're new to this, we highly recommend reading our guide to startup equity basics for job seekers. It lays the foundational knowledge you'll need.

Now, let's get into the nitty-gritty. This guide will walk you through exactly how these calculators work, what numbers to input, and how to interpret the results to make the best decision for your career.

An equity calculator is a powerful tool, but it's only as sharp as the numbers you feed it. To get a realistic picture of what your equity could be worth, you first have to get a handle on the core inputs that drive the whole calculation. These aren’t just abstract terms on an offer letter; they're the actual levers that will shape your financial outcome.

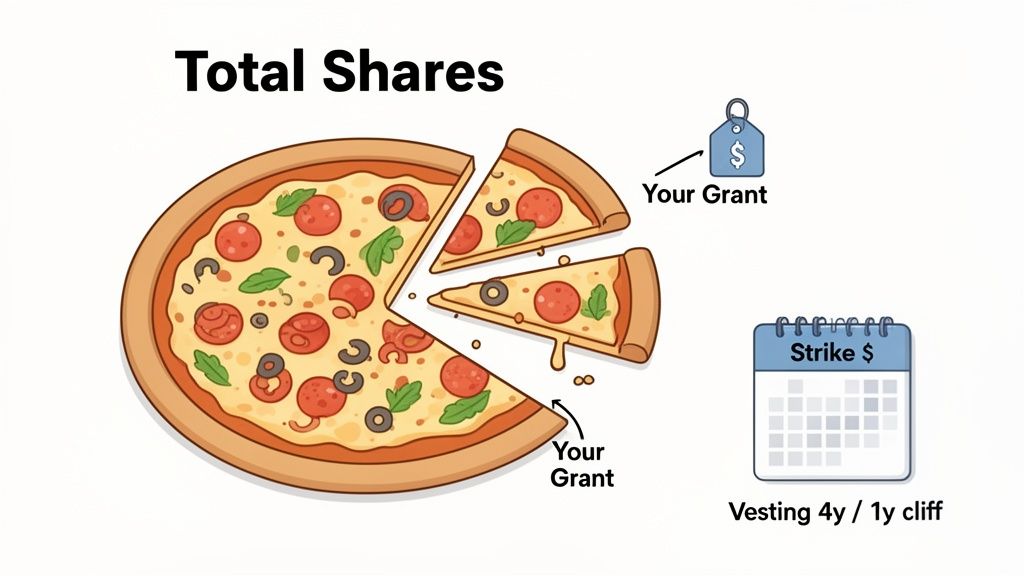

It helps to think of the startup as a giant pizza. Each input helps you figure out the size of that pizza, how many slices you've been offered, what you’ll have to pay for them, and when you actually get to claim them.

First things first: you need to understand how your grant fits into the big picture. Two numbers are key here:

A grant of 20,000 shares might sound huge, but that number is totally meaningless without knowing the total share count. For instance, 20,000 options in a company with 10 million total shares (0.2%) is a much, much stronger offer than 20,000 options in a company with 100 million shares (0.02%).

A larger number of options isn't always better. The critical metric is the percentage of the company your grant represents, which you find by dividing your grant by the total fully diluted shares.

Once you know how many slices you have, the next critical number is the strike price. This is the fixed price per share you’ll pay to purchase your stock options if and when you decide to exercise them.

A lower strike price is always better for you. Plain and simple. It means your cost to acquire the shares is lower, which directly increases your potential profit down the road.

Let's say you want to exercise 10,000 options. With a $1.00 strike price, it costs you $10,000. But if the strike price were $3.00, that same grant would cost you $30,000 to exercise. That $20,000 difference comes straight out of your pocket.

So, where does this price come from? It's set by the company's 409A valuation, which is an independent appraisal of the fair market value (FMV) of the company's stock. An early-stage company will naturally have a much lower FMV—and therefore a lower strike price for you—than a more mature one.

Here’s a reality check: your stock options aren't actually yours on day one. You earn them over a period of time through a vesting schedule. This is the company's way of making sure you stick around and help build the value of those shares.

The industry standard vesting schedule is pretty straightforward:

Let's run a quick scenario. Imagine you were granted 48,000 options.

Understanding your vesting schedule is absolutely crucial. It dictates how much equity you'll actually own if you decide to leave before the full four-year term is up. A good equity calculator will let you play with different departure dates, giving you a clear picture of what you’ve earned at any point in time.

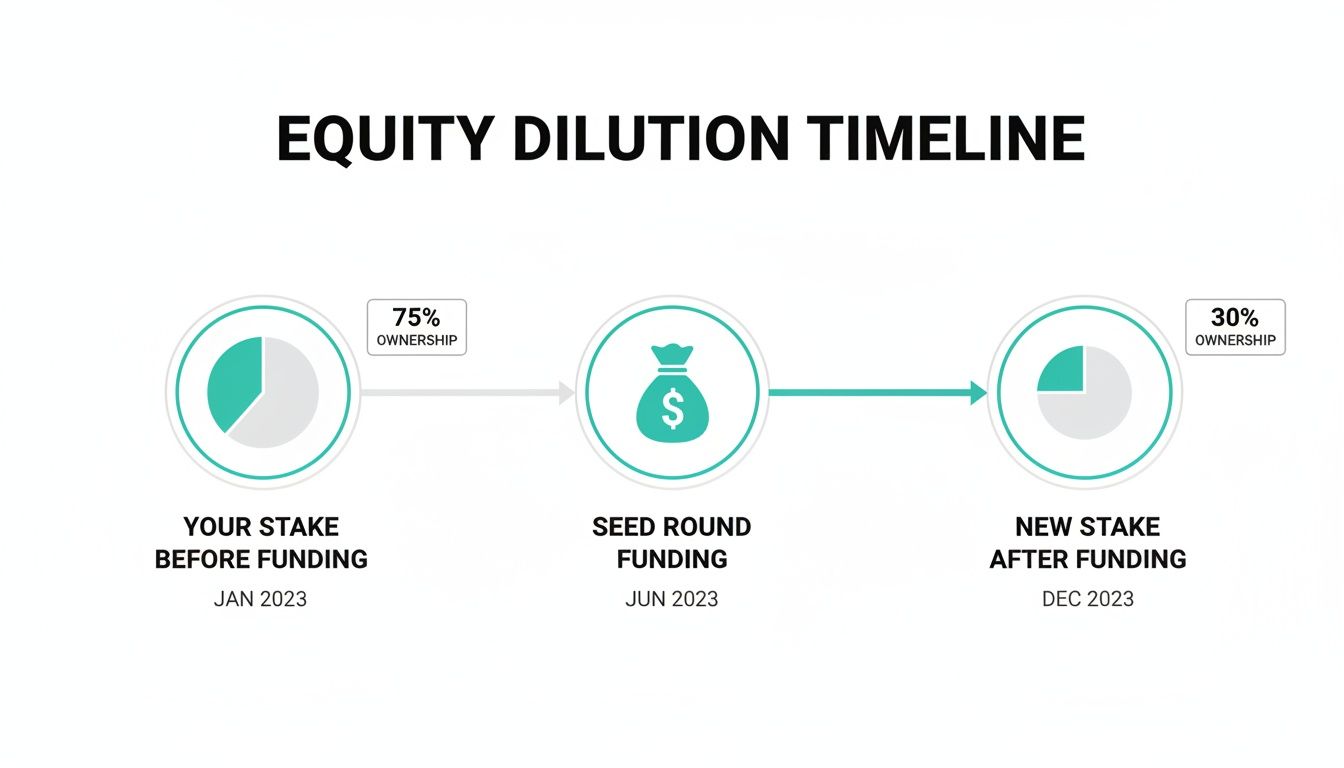

The word dilution can sound pretty alarming, especially when you’re looking at a startup equity offer. It feels like you’re losing a piece of something valuable. But in a growing startup, dilution is not only normal—it's often a great sign. It means the company is successfully attracting new investment to fuel its growth.

The trick is to stop focusing on your ownership percentage and start thinking about the total value of your stake.

Let me put it this way. Imagine you own a slice of a small pizza. Someone comes along and offers to make that pizza ten times bigger, but your slice will be a smaller percentage of the new, giant pizza. Would you take that deal? Absolutely. Your new, smaller-percentage slice is now way bigger than your original one.

This is exactly how dilution works in a startup. When the company raises a new funding round (like a Series A or B), it creates and sells new shares to investors. This increases the total share count, meaning your grant now represents a smaller piece of the pie. But that new investment also boosts the company’s valuation, making the entire pie much, much larger.

Dilution isn't about losing value; it's about trading a percentage of ownership for the capital needed to grow the company's total value. A smaller slice of a much bigger pie is often worth far more than a large slice of a small one.

A startup equity calculator is the perfect tool for running these numbers yourself. It lets you model how your potential payout changes as the company valuation grows, even while your ownership percentage shrinks with each funding round.

Let's walk through a clear example to see how this plays out in the real world. Say you join a seed-stage startup and get options representing 0.1% of the company, which is currently valued at $10 million.

A year goes by. The company crushes its goals and is now ready to raise a Series A round to scale up.

The company raises $8 million from a venture capital firm. In a typical Series A, investors might acquire around 20% of the company. To do this, new shares are issued and sold to them.

See what happened? Your ownership percentage went down, but the actual value of your equity more than tripled. That's because the company put the new funding to good use.

Another 18 months pass. The company is now a leader in its market and raises a huge $50 million Series B round. This time, new investors take another 15-20% stake.

Your ownership percentage has shrunk by nearly 40% since you started, but the value of your equity has grown 16x. This is the classic startup trade-off: growth is almost always more important than the percentage you own. If you want to dive deeper into the mechanics, you can learn more about what equity dilution means for employees in our detailed guide. This is the dynamic that can lead to the life-changing outcomes startup equity is known for.

Theory is one thing, but nothing makes startup equity click like seeing the numbers in action. Let’s move beyond the abstract terms and into a real-world scenario to see how an equity calculator can turn an offer letter into a tangible look at your financial future.

We’ll follow a senior product manager named Maria who just got an exciting offer from a promising Series A startup. By plugging her numbers into a calculator, we can model a few potential outcomes and see just how dramatically her equity could play out.

Maria's offer comes with a significant equity grant. Here are the key details we'll be working with, pulled straight from her offer letter:

First things first, what percentage of the company is she actually being offered? We can figure this out by dividing her grant (25,000) by the total shares (15,000,000). This gives her an initial stake of roughly 0.167%.

Next, let's find the current 'paper value' of her grant. The company's latest share price is its valuation ($40M) divided by the total shares (15M), which comes out to $2.67 per share. The paper value is that price minus her strike price, multiplied by her options: ($2.67 - $2.00) * 25,000 = $16,750. It's a nice starting point, but the real magic of a calculator comes from modeling what happens next.

The true value of startup equity isn't realized until an "exit"—usually an acquisition or an IPO. This is where a calculator becomes your crystal ball. For Maria's situation, we'll assume the company raises one more funding round (Series B) before an exit, which will cause 20% dilution to her stake.

Dilution sounds scary, but it's a normal part of the startup journey. As new investors come in, the company issues more shares, which shrinks everyone's percentage of the pie. The goal, of course, is that this new funding will make the whole pie massively bigger.

As you can see, your slice of the ownership pie gets smaller with each funding round, but the new capital is what fuels the growth that makes the entire pie more valuable.

Let's start with a solid, respectable outcome. The company grows steadily and gets acquired for $200 million. Here's how the math breaks down.

That’s a life-changing amount of money from a single equity grant. But what happens if the company hits it big?

Now for the dream scenario. The company becomes a dominant force in its market and goes public with a $1 billion valuation. The inputs are all the same, we're just swapping in a much bigger exit number.

By running these two scenarios, Maria gets a clear, data-backed range of possibilities. Her equity could be worth anywhere from $218,000 to nearly $1.3 million, depending entirely on the company's future success.

This exercise shows exactly what a startup equity calculator is for. It takes the abstract details in an offer letter and transforms them into a spectrum of real financial outcomes. It empowers candidates like Maria to go beyond just the salary, assess the risks, and make a huge career decision with their eyes wide open.

A startup equity calculator gives you a great starting point, but it only tells half the story. The real-world cash you walk away with after an exit depends on a few critical details that most calculators don’t account for.

Understanding these concepts is what separates a hopeful employee from a truly informed stakeholder. It shows you’re serious about your financial future and helps you protect what you’ve earned. Two of the most important factors are liquidation preferences and the company's capitalization table.

Let's say a startup sells for $50 million. You might think that money gets split up among everyone based on their ownership percentage. That’s almost never how it works. Investors who fund the company get something called a liquidation preference—think of it as a VIP line to get their money back first.

Investors put their cash on the line, and this preference ensures they recoup their investment (and sometimes more) before employees holding common stock see a dime.

Liquidation preferences are a contractual right for preferred shareholders (investors) to be paid out a specific amount from exit proceeds before common shareholders (employees and founders) receive anything.

There are two main flavors you’ll run into:

Knowing which type a company has is crucial because it directly dictates how much money is left for you.

The second document you need to know about is the capitalization table, or cap table for short. This is the company’s official master spreadsheet that tracks who owns what—every share held by founders, investors, and employees. It’s the single source of truth for the company's entire ownership structure.

A detailed cap table shows you more than just the total number of shares. It reveals the different classes of stock (preferred vs. common) and can offer big clues about the liquidation preferences attached to each investor's shares.

Asking smart questions about the cap table shows you’re a sophisticated candidate. It can tell you a lot about the company's financial health and how it views employee equity. You can learn more about how to navigate these conversations in our guide on how to negotiate stock options.

Let's see how this works in a simple scenario. Imagine a company raises $10 million from investors who have a 1x non-participating liquidation preference. A few years later, the company gets acquired for $30 million.

Before anyone else gets paid, the investors get their $10 million back. The remaining $20 million is then split among all shareholders, including employees with stock options. If those investors had participating preferred stock, they would take their $10 million and their ownership percentage of the remaining $20 million, leaving far less for the rest of the team.

Finally, remember that the actual cash you receive will also be hit by taxes. Getting a basic handle on how your equity payout is taxed—specifically the rules around capital gains tax—is key to forecasting your actual take-home amount. These are the details that separate a paper fortune from real money in your bank account.

Alright, you’ve got the theory down. Now it's time to stop crunching numbers in your head and start using the right tools to see what your equity offer actually looks like. There are a handful of solid calculators out there that can help you model different scenarios and get a real feel for your potential stake.

Choosing the right one really just depends on what you need—some are incredibly user-friendly, while others offer more firepower for complex modeling. These tools have become the standard for a reason. In fact, an estimated 70% of new ventures now rely on ownership distribution tools to map out fair equity splits. This marks a huge shift in how startups handle compensation, a trend you can dig into deeper to master the step-by-step approach to equity calculation.

Here are a few of the most trusted tools that will help you run the numbers on your offer. Each one has its own vibe and strengths.

Here’s a look at the straightforward interface from Captable.io, where you can plug in your grant details and see what the future might hold.

As you can see, the tool keeps inputs like share price and your number of options separate from the projected exit value, giving you a clear, no-nonsense picture of your potential earnings.

Even after you've run the numbers, a startup offer can leave you with some nagging questions. It's completely normal. Let's tackle a few of the most common ones I hear from candidates, so you can walk into any negotiation with total confidence.

Everyone wants to know the magic number for a "good" equity percentage, but the honest answer is: it doesn't exist. The right amount of equity is all about context—the company's stage, your specific role, and how much experience you bring to the table.

Think about it this way: at a Series A company, a senior engineer might see an offer between 0.05% and 0.25%. A director, on the other hand, could command something closer to 0.5% to 1.5%. Instead of getting fixated on the percentage itself, use an equity calculator to model what that stake could actually be worth. A smaller slice of a rocket ship is almost always better than a huge chunk of a company that's going nowhere.

This is the classic startup dilemma, and it really boils down to your personal appetite for risk. A higher salary is cash in the bank, offering stability and immediate financial security. Equity is the lottery ticket—a bet on a potentially massive, but completely uncertain, future payday.

If you have deep conviction in the founders, the product, and the market, pushing for more equity could have a life-changing upside. But if you need financial certainty right now, or you aren't completely sold on the startup's chances, taking the higher salary is the smarter, safer move. A calculator helps you put a number to that upside, making the trade-off crystal clear.

A higher salary pays your bills today, while a significant equity stake is a bet on a life-changing payout tomorrow. Your choice reflects your belief in the company's journey and your own financial goals.

When your employment ends, the clock starts ticking on what’s called a Post-Termination Exercise (PTE) window. You typically have just 90 days to decide whether you want to buy (or "exercise") the options you've already vested.

If you don't act within that window, those options vanish and go back into the company’s option pool. It’s a huge financial decision, since exercising means paying cash for both the stock's strike price and the potential taxes that come with it. Always make a point to clarify the PTE window during your offer negotiation—some more progressive companies are now offering employee-friendly extended periods.

Absolutely. Just like your salary, your equity grant is almost always on the table for discussion. The trick is to come prepared with more than just a vague request for "more."

This is where your homework pays off. Use a startup equity calculator and market data to see how your offer stacks up against similar roles at companies of the same stage. Build a strong case around the specific value and experience you bring to the table and your long-term commitment to the mission. A data-driven ask isn't just more professional—it’s far more likely to succeed.

A startup equity calculator is a tool that takes the key variables from your equity offer — your number of options or shares, your strike price, the total fully diluted shares outstanding, the company's current valuation, and your vesting schedule — and models what your stake could be worth at different future exit valuations. You plug in the numbers from your offer letter, set one or more hypothetical exit scenarios, and the calculator projects a pre-tax payout range for each. More advanced tools also factor in expected dilution from future funding rounds, showing how your ownership percentage changes while your stake's dollar value can still grow significantly.

The four essential inputs are your stock option grant (the number of shares you have the right to purchase), your strike price (the fixed price per share you pay when you exercise), the total number of fully diluted shares outstanding (found by dividing your grant by this number to get your ownership percentage), and the company's current valuation (which establishes today's paper value of your grant). For forward-looking scenario modeling you also need an assumed exit valuation and an estimate of how much dilution you will experience from future funding rounds — typically 15 to 25 percent per round. Your strike price and grant size will be in your offer letter; you may need to ask the company directly for the total share count and any outstanding convertible instruments like SAFEs or convertible notes.

How does dilution affect my startup equity?Dilution occurs when a company issues new shares — most commonly during a funding round — which increases the total share count and reduces everyone's ownership percentage proportionally. For example, if you own 0.1 percent before a Series A where investors receive 20 percent of the company, your stake shrinks to approximately 0.08 percent. However, if that round raises the valuation from $10M to $40M, your 0.08 percent is now worth $32,000 — more than triple the original $10,000 paper value. Dilution is therefore not inherently harmful; it is the mechanism through which growth-stage companies fund the activities that make your remaining stake worth more. The critical question is whether the valuation increase justifies the dilution, which is exactly what a calculator helps you model.

Stock options give you the right to purchase company shares at a fixed strike price set at the time of your grant. Your profit at exit is the difference between the exit price per share and your strike price, meaning a low strike price is highly valuable. Options are most common at early-stage startups where the 409A valuation is low, maximizing potential upside. Restricted Stock Units (RSUs) are direct grants of shares that vest over time with no purchase required — when RSUs vest, you receive shares at full market value, taxed immediately as ordinary income. RSUs are most common at later-stage or public companies where the value is more predictable and employees prefer certainty over speculative upside. The key practical difference is that options require cash to exercise and carry more tax complexity, while RSUs are simpler but offer less financial leverage on early-stage growth.

A vesting schedule is the timeline over which you earn your equity grant. The industry standard is a four-year schedule with a one-year cliff: no equity is earned in the first twelve months, but on your one-year anniversary 25 percent of your total grant vests immediately — the "cliff" — and the remaining 75 percent vests in equal monthly installments over the following three years. The cliff protects the company from granting valuable equity to employees who leave quickly. For employees, it means leaving before the one-year mark has a significant financial cost — you walk away with zero equity regardless of how close you are to that anniversary. A startup equity calculator lets you model your stake's value at any point in the vesting schedule, which makes the real financial cost of leaving visible and concrete.

A liquidation preference is a contractual right giving investors priority access to exit proceeds before common shareholders — which includes employees holding stock options. In a non-participating preferred structure, investors choose at exit between receiving their original investment back or converting to common stock and sharing pro-rata with everyone else, whichever is more advantageous. In a participating preferred structure, investors receive their original investment back first and then also participate alongside common shareholders in dividing what remains — often called "double-dipping" — which can substantially reduce the pool available to employees, particularly in smaller exits. For any startup offer, asking whether the company has participating or non-participating preferred stock is one of the most important questions to ask before accepting.

There is no universal benchmark because the right percentage depends entirely on the company's funding stage, your seniority, and the role. At a Series A company, a senior engineer might receive 0.05 to 0.25 percent, while a director-level hire might see 0.5 to 1.5 percent. At seed-stage companies, percentages are typically higher because the risk is greater and the valuation is lower. Rather than fixating on the percentage, use a startup equity calculator to model what that specific stake would be worth at realistic exit valuations — a smaller percentage of a fast-growing company is often worth far more than a larger percentage of a company with limited growth prospects. Context is everything.

Several tools are widely used and trusted in the industry. Carta is the gold standard for cap table management and offers detailed scenario modeling, primarily designed for companies but with strong resources for employees wanting to understand their grants. Captable.io by LTSE is particularly useful for modeling how dilution plays out across multiple funding rounds in a visual, intuitive way. Holloway's Guide to Equity Compensation is not a calculator per se but is an exhaustive reference covering every nuance of startup equity, including frameworks and spreadsheet templates for building your own models. For most candidates, starting with Captable.io for visual dilution modeling and cross-referencing with Carta's educational resources provides a solid analytical foundation.

Yes, equity grants are almost always negotiable alongside base salary. The most effective negotiation approach is data-driven rather than vague — use a calculator to benchmark your offer against market data for similar roles at companies of the same stage and funding level, and present a specific counter grounded in that comparison. Connect your ask to the tangible value you bring: your experience, your relevance to the company's immediate challenges, and your long-term commitment. If the company cannot increase the grant size, there are other equity-related terms worth exploring: an extended post-termination exercise window (giving you more time to decide whether to buy vested options after leaving), accelerated vesting in an acquisition scenario, or a more favorable vesting start date.

Ready to find your next role at a high-growth startup? Underdog.io connects top tech talent with vetted companies where your skills and equity can truly make an impact. Apply in 60 seconds.