Equity dilution is what happens when your ownership percentage in a company shrinks because new shares are created. It’s a totally normal, and frankly necessary, part of growing a startup. You're essentially trading tiny pieces of ownership for the fuel you need to grow—things like cash or top-tier talent.

This means your personal stake becomes a smaller slice of a much larger pie.

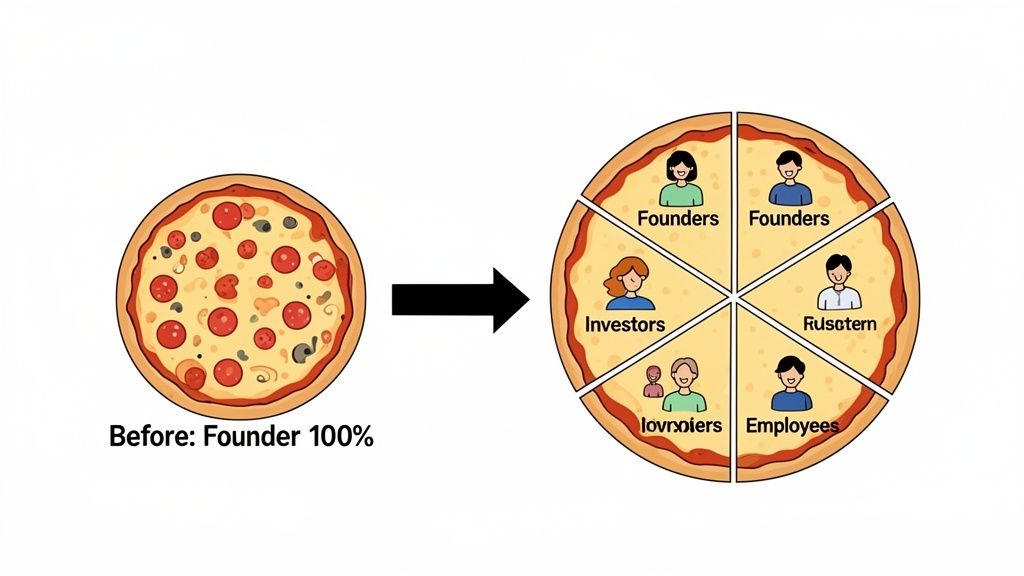

Imagine your startup is a pizza. In the very beginning, you, the founder, own the whole thing. It’s 100% yours. But one pizza, no matter how good, can only feed so many people. To turn it into a city-wide pizza empire, you're going to need a bigger oven, more ingredients, and a team of expert chefs.

This is where growth—and dilution—kicks in.

To get the cash for that bigger oven (i.e., scale your operations), you bring on an investor. In exchange for their money, you don't just cut a piece out of your existing pizza. Instead, you make the entire pizza bigger and give them a brand-new slice from it.

This is the central idea you have to grasp about equity dilution: your ownership percentage goes down, but the total value of the company (the whole pizza) goes up. Hopefully, way up.

Here’s a practical, real-world example:

Your percentage dropped, but the value of your stake has exploded. Your 70% is now worth $3,500,000. You swapped a piece of ownership for a massive leap in value. This is a foundational concept, and you can get a great primer by checking out these startup equity basics for job seekers.

To see this in action, let's look at how your ownership percentage changes even if your personal share count doesn't.

As you can see, even though you still hold your original one million shares, your claim on the company's total value shrinks proportionally as new shares are introduced for others.

The goal isn't to own 100% of a small company forever. It's to own a meaningful percentage of a very large, successful one. Dilution is the mechanism that makes this growth possible.

This isn't just about investors, either. You need to hire amazing people to help build the company. To attract them, you’ll create an employee stock option pool (ESOP), which is just another set of new slices reserved for key hires.

Every time you grant options to a critical new team member, the pizza gets a little bigger, and everyone's existing slice becomes a slightly smaller percentage of the whole.

But here’s the key: each of those talented people should be making the entire pizza more valuable. In the end, equity dilution isn't a loss; it's a strategic move. It's the price of ambition—the calculated choice to share ownership to build something far bigger than you ever could on your own.

Equity dilution doesn't just happen by accident. It’s the direct result of deliberate, strategic decisions made to grow the company. Understanding dilution means recognizing the key moments that trigger it—not as moments of loss, but as calculated moves to build a much bigger pie for everyone.

Fundamentally, there are three main events that force a company to issue new shares and, in turn, dilute the ownership percentage of everyone already on the cap table. Each one serves a distinct purpose on the startup journey, from getting that first check in the bank to landing world-class talent.

Let’s break them down.

By far the most common and significant cause of dilution is raising money from investors. When a startup needs cash to hire engineers, build the product, or enter a new market, it often turns to venture capital (VC) firms or angel investors. In exchange for that capital, the company issues them brand new shares of stock.

This process isn't a one-and-done deal; it happens in distinct stages, or rounds:

These rounds are where the toughest negotiations happen. Founders feel the sting of dilution the most in the earliest stages, often giving up 20% or more of their company in a single round. Why? Because the business is unproven, and investors demand a larger piece of the action to compensate for the risk. Data shows that a typical seed round involves 20% dilution, with a Series A often taking another 20%. For a deeper look at how this plays out, check out this founder's guide to equity dilution.

A brilliant idea is worthless without the people to build it. But early-stage startups can't compete with the salaries offered by big tech companies. Their secret weapon? Equity. This is managed through an Employee Stock Option Pool (ESOP).

An ESOP is simply a block of shares the company sets aside for future hires. To create this pool, the company has to mint new shares, which dilutes every single existing shareholder—from the founders to the earliest investors.

Think of the ESOP as a talent acquisition fund paid for with equity. It’s a strategic dilution that invests in the human capital you need to actually build the company and make everyone’s shares worth more.

For instance, a startup might create an initial option pool of 10% to 15% of its total equity. While this lowers every current shareholder's ownership percentage on paper, the goal is that the incredible people you hire with those options will create far more value than the dilution they cause.

In the very early days, before a company has a formal valuation, founders often use simpler fundraising tools to get started. The two most common are SAFEs (Simple Agreement for Future Equity) and convertible notes.

With these, an investor gives the company cash now in exchange for the promise of getting shares later, during a future funding round. These instruments "convert" into stock once the company raises its first priced round (like a Series A).

Here’s how they cause dilution:

This means that when the Series A financing finally happens, it's a double dilution event. Not only are you issuing shares to the new VCs, but all the early SAFE and note holders get their shares, too. It’s a necessary mechanism that bridges the critical gap between having an idea and getting your first official valuation.

Abstract concepts and percentages only get you so far. To really get a feel for how equity dilution works, you need to see the numbers in motion.

Let's walk through a practical example with a hypothetical startup, "Innovate Inc." We’ll follow two founders as they build their company from the ground up, watching their capitalization table (cap table) evolve through three critical growth stages. This journey will show exactly how ownership percentages shift while the value of their stake can actually grow.

Innovate Inc. starts with two co-founders, Alex and Ben. They decide to authorize and issue 10,000,000 shares of common stock for their new venture, splitting it right down the middle. Each founder gets 5,000,000 shares.

At this point, the company has no outside investors and no employees, so the cap table is as simple as it gets.

Innovate Inc. - Founding Cap Table

Each founder owns half the company. It’s clean and straightforward. But to build their product, they need a brilliant lead engineer—someone they can’t yet afford to pay a top-market salary. This is where equity becomes a powerful recruiting tool.

To attract that first crucial hire, Alex and Ben decide to create an Employee Stock Option Pool (ESOP). This is a block of new shares set aside specifically for granting equity to employees. They agree to create a 15% option pool, a pretty standard size for an early-stage company.

Creating this pool requires issuing new shares, which triggers the first dilution event for the founders. The math works by figuring out the total shares needed so the original 10,000,000 shares represent 85% of the new total (100% - 15%). The new total number of shares will be 11,764,706 (10,000,000 / 0.85).

This means they need to issue 1,764,706 new shares for the ESOP.

Innovate Inc. - Post-ESOP Cap Table

Suddenly, Alex and Ben no longer own 50% each. Their ownership has been diluted to 42.5%. They haven't lost a single share, but their slice of the pie just got smaller to make room for future team members.

With a founding team in place, Innovate Inc. needs cash to build its first product and find customers. They catch the eye of an angel investor who agrees to invest $500,000 at a $2,500,000 pre-money valuation.

The "pre-money" valuation is what the company is worth before the new cash comes in. The "post-money" valuation is simply the pre-money value plus the investment.

The investor’s ownership will be 16.67% ($500,000 investment / $3,000,000 post-money valuation). To give the investor this stake, the company has to issue even more shares. The current 11,764,706 shares now represent 83.33% (100% - 16.67%) of the company. The new total share count will be 14,117,647 (11,764,706 / 0.8333), which means issuing 2,352,941 new shares to the angel investor.

The Big Picture: While the founders' ownership percentage drops again, the value of their shares has jumped. The company is now worth $3 million. Alex’s 35.4% stake is now valued at over $1 million—a huge leap from where it started.

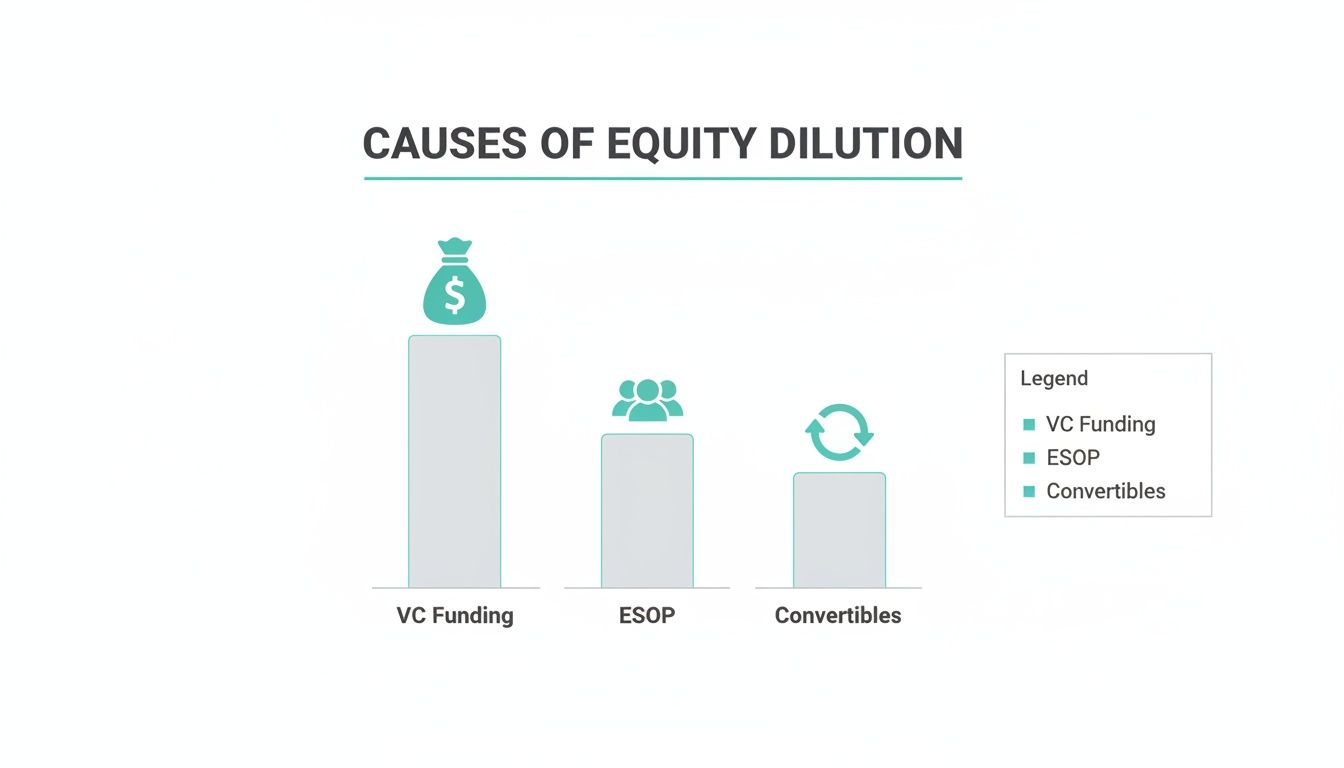

The infographic below shows the most common events that trigger these dilution scenarios in startups.

This visual breaks it down nicely: issuing shares for venture capital, employee option pools, and convertible instruments are the fundamental drivers of equity dilution.

Innovate Inc. - Post-Seed Round Cap Table

Notice that everyone’s percentage, including the unallocated ESOP, was diluted by the seed investment. This is the nature of growth.

Fast forward 18 months. Innovate Inc. has launched its product and is generating real revenue. A venture capital firm sees the potential and leads a Series A round, investing $5 million at a $20 million pre-money valuation.

The math is the same, just with bigger numbers.

The new VC investor will own 20% of the company ($5M / $25M). The existing 14,117,647 shares will now represent 80% of the new total. This means the new total share count is 17,647,059 (14,117,647 / 0.80), and 3,529,412 new shares are issued to the VC firm.

Here we can pull all the data together to see the full journey.

This table tracks the ownership changes for each stakeholder at Innovate Inc. as the company raises capital and issues new stock, providing a clear illustration of dilution in action.

After two rounds of financing and creating an option pool, Alex’s ownership has dropped from 50% to 28.3%. It sounds like a big loss, but the company is now valued at $25 million. His stake is worth over $7 million.

This is the power of "good" dilution—trading percentage points for a massive increase in the overall value of the company. You own a smaller piece of a much, much larger pie.

Equity dilution isn't just an abstract concept; it feels fundamentally different depending on where you sit at the table. For founders, employees, and investors, it represents a unique set of trade-offs, risks, and potential rewards. Here are actionable takeaways for each group.

For founders, dilution is a constant balancing act. On one hand, every funding round and hire chips away at your ownership. On the other, that same dilution is the fuel for growth.

The core challenge for a founder is to give up just enough equity to maximize the company's chance of success without losing too much control or future upside. It's a strategic sacrifice made in pursuit of a much larger victory.

Actionable Insight: Model out your fundraising scenarios on a spreadsheet. Create columns for Pre-Money Valuation, New Investment, Post-Money Valuation, and the resulting ownership percentages for each stakeholder. By plugging in different numbers, you can see exactly how a 20% vs. a 25% dilution impacts your stake. This turns a gut-feel decision into a data-driven one.

If you’re an employee, understanding dilution is absolutely critical to figuring out what a job offer with equity is actually worth. A classic mistake is to focus only on the number of stock options you're granted.

Actionable Insight: An offer of 10,000 options means nothing on its own. The two numbers you must ask for are total outstanding shares and the preferred price per share from the last funding round. With these, you can calculate your ownership percentage and the current "paper value" of your grant. This is crucial context when you are figuring out how to exercise stock options in the future.

Ultimately, the goal is for your smaller slice to be part of a pie that grows exponentially. Owning 0.1% of a company that exits for $1 billion is life-changing; owning 1% of a company that goes bust is worthless.

Investors are the primary drivers of dilution, but they are not immune to its effects. When a company they’ve already backed raises its next round, their own stake gets diluted.

Actionable Insight: This is why investors negotiate for protections. The two most important are:

These mechanisms help align incentives, ensuring everyone stays focused on the main goal: making the whole pie bigger.

Investors might be the ones causing dilution when they fund a company, but they aren't immune to its effects. When a startup they’ve backed raises its next round, their stake gets diluted just like everyone else's. To deal with this reality, savvy investors negotiate specific protections right into the term sheets. These clauses are all about safeguarding their ownership percentage and protecting their investment from getting washed out in the future.

For founders and employees, getting a handle on these terms is absolutely critical. They tell you a lot about an investor's expectations and act as a safety net that can dramatically change the cap table, especially if the company hits a rough patch. Two of the most important protections you'll see are pro-rata rights and anti-dilution clauses.

Pro-rata rights give an investor the right—but not the obligation—to buy more shares in future funding rounds to keep their ownership percentage the same. Think of it as a VIP pass to the next investment opportunity. It ensures the folks who believed in the company early on don't get squeezed out as it grows and brings in more cash.

Here’s how it works in the real world:

This right is also a powerful signal. When an investor exercises their pro-rata, it shows they still have strong conviction in the company's future. If they decide to pass, it can sometimes be read as a red flag by new investors coming in.

While pro-rata rights protect an investor's percentage of ownership, anti-dilution provisions protect the value of their investment. These clauses only kick in during a "down round"—that’s when a company has to sell shares at a lower price than it did in a previous round. This usually happens when a startup has missed its targets or is facing tough market conditions, causing its valuation to drop.

An anti-dilution clause adjusts the conversion price for the earlier investor, effectively giving them more shares to make up for the lower valuation. It’s a rebalancing act to keep their investment from being unfairly devalued by the company’s stumble.

Anti-dilution clauses are essentially a price protection guarantee for early investors. They ensure that if the company hits a rough patch and raises money at a lower price, the initial backers aren't disproportionately penalized.

There are two main flavors of anti-dilution, and they have wildly different impacts on the cap table.

Understanding the difference between these two mechanisms is vital. One is standard practice, while the other is considered aggressive and can be incredibly painful for founders and employees.

For everyone at the table—founders, employees, and investors—these terms lay out the rules of engagement for future growth and potential setbacks. They are a core part of what equity dilution means in practice.

An equity offer isn't just a number on a piece of paper. It’s a complex part of your compensation, and you need to look past the share count to figure out what it's truly worth. This is where your knowledge of dilution moves from a vague concept to a practical tool for making a big career decision.

When you're armed with the right questions, you can have a smart, confident conversation about your future at the company. The goal here is to get a crystal-clear picture of your potential ownership and what it might realistically be worth one day.

When a startup offers you an equity grant, the number of options is just one piece of a much larger puzzle. To solve for its actual value, you need more information. A great first step is learning how to accept a job offer, which often means having these exact kinds of detailed financial discussions.

Here’s a practical checklist of what you need to ask:

The way a company answers these questions tells you a lot. A transparent, confident company will have this information ready for you. If they hesitate, give vague answers, or act like you shouldn't be asking, that’s a major red flag. A lack of transparency here often points to bigger issues.

Understanding the context behind your equity offer is non-negotiable. An offer of 50,000 options means nothing without knowing the total share count and company valuation. It’s the difference between owning a significant stake and holding a lottery ticket.

Pay attention to how all the numbers fit together. A sky-high valuation with a relatively small number of total shares could mean your options are valuable on paper today, but it also signals that serious dilution is almost certainly coming. On the flip side, a lower valuation might mean your grant offers more upside if the company takes off.

By asking these questions, you’re doing more than just evaluating an offer—you're assessing your potential role as a future owner.

When you're navigating the world of startup equity, a few questions always seem to pop up. Let's clear up some of the most common points of confusion so you can feel confident evaluating what dilution means for you.

Nope, not at all. Your salary has no direct connection to equity dilution.

Dilution only happens when the company issues brand-new shares—usually during a fundraising round or when adding more stock to the employee option pool. This process reduces the ownership percentage for all shareholders equally, no matter what their cash compensation looks like.

Getting this distinction right is key to understanding how much dilution could potentially happen down the road.

You will never lose the shares you've already been granted. That's a common misconception.

Dilution doesn't take your shares away; it just reduces your percentage of ownership because the total number of shares in the company has increased. You'll always own the same number of shares, but they'll represent a smaller slice of what is hopefully a much bigger, more valuable company pie.

The core idea is that you own the same number of shares, but the total pie gets bigger. Your slice becomes a smaller percentage, but its value should increase significantly if the company is growing successfully.

When you're looking at an offer, it’s always a good idea to understand the terms laid out in the initial partnership and founders' agreements, as these documents often define how equity changes are handled. As you prep for those conversations, make sure you're ready with these essential questions to ask before accepting a job.

Equity dilution is what happens when a company issues new shares, which reduces the ownership percentage of existing shareholders. Imagine owning 1 slice of a pizza cut into 10 slices (10%). If the pizza is cut into 20 slices, you still have 1 slice, but now you own only 5%. Your share of the whole has been "diluted."

Dilution most commonly occurs when a startup raises money from investors (a funding round). To raise capital, the company sells new shares to these investors, increasing the total number of shares in existence. This process is necessary for growth but dilutes the ownership of earlier shareholders, including founders and employees.

Not necessarily. While dilution reduces your percentage ownership, the goal is for the company's overall value (its valuation) to increase significantly more because of the new investment. You own a smaller piece of a much larger, more valuable pie. If the value increases enough, the actual dollar value of your shares can grow even though your percentage shrinks.

Percentage ownership is your slice of the company. Share value is tied to the company's total valuation divided by the total shares. Dilution reduces your percentage, but if the new investment increases the company's valuation enough, the price per share (and thus the value of your shares) can still go up.

Anti-dilution provisions are protective clauses often granted to investors, not employees, in certain financing terms. They adjust the investor's share price if the company later raises money at a lower valuation (a "down round") to minimize their dilution. Standard employee stock options do not have anti-dilution protection.

It's difficult to predict precisely, but you should ask about the company's capitalization structure ("cap table"). Key questions include: "How much has been raised to date?", "What is the current total number of shares (fully diluted)?" and "How much is set aside for the employee option pool?" This context helps you understand your grant's potential.

As an employee with standard stock options, you cannot prevent dilution from future funding rounds, which are essential for the company's growth. Your focus should be on the company's potential for increased valuation. You can negotiate for a larger initial grant or "refresh" grants at later stages to offset the effects of dilution over time.

At Underdog.io, we connect top tech talent with innovative startups where your equity can make a real impact. Ditch the endless applications and let curated opportunities find you. Get started here.