You get the offer. The salary looks decent. The role is exciting. The team seems sharp. Then you hit the equity section and the confidence drops fast.

You see terms like stock options, RSUs, strike price, vesting, cliff, exercise window. The recruiter says the package has “real upside,” but the offer letter doesn't tell you what that upside is worth to you. That's the part most candidates struggle with.

If you're asking what is equity compensation, the practical answer is simple. It's ownership-based pay that can become valuable later, but only if several things go right. The company has to grow. Your grant has to vest. The instrument has to work in your favor. Taxes and liquidity have to line up. Until then, the headline number is only a possibility.

As a startup recruiter, I've seen strong candidates make two opposite mistakes. Some dismiss equity because it feels abstract. Others treat it like guaranteed money. Both approaches are costly. The right move is to evaluate equity the same way you'd evaluate any other part of compensation. Understand the mechanics, ask better questions, and translate the offer into realistic scenarios.

Startup offers gain clarity under these circumstances. Not because equity becomes simple, but because the trade-offs stop hiding behind jargon.

A lot of candidates reach the final round feeling confident about the job itself and uncertain about the offer.

That's normal. Cash compensation is easy to compare. Equity usually isn't. A company might offer a lower salary and say the upside makes up for it, but that only helps if you can judge whether the upside is credible, how long it may take, and what you'd need to do to receive it.

The practical issue isn't defining equity in one sentence. The issue is figuring out whether the equity in front of you is meaningful compensation or just a nice-looking line item.

Equity only matters if you can explain it back to yourself in plain English.

When candidates ask me about an offer, I usually start with three questions:

If you don't know those answers, you don't know the offer yet.

A smart equity evaluation also means accepting a less comfortable truth. Equity isn't extra. It often replaces cash you could have taken elsewhere. So when a company offers ownership, you're making an investment decision with your labor.

That's why candidates need more than a glossary. They need a way to judge the actual financial future attached to the grant.

Equity compensation means a company pays part of your compensation in ownership instead of only salary or bonus. In practice, that ownership usually shows up as stock options, RSUs, ESPPs, or related awards. One startup benchmark is that companies reserve 13% to 20% of equity for employee compensation, with typical grant ranges of 0.8% to 5% for C-suite executives, 0.3% to 2% for VPs, and 0% to 0.2% for junior hires, according to Rho's explanation of equity compensation.

The cleanest analogy is a pie.

The company gives you a slice today, not because the slice is immediately edible, but because everyone hopes the whole pie becomes much larger over time. If that happens, your slice may become valuable. If it doesn't, your ownership may end up worth little or nothing.

That's why equity is both alignment and risk-sharing.

The company preserves cash. You accept more uncertainty in exchange for possible future upside. That trade can make sense, especially at startups where cash is tighter and talent is expensive. It can also be a bad trade if the salary discount is too steep or the equity terms are weak.

Startups usually can't match the cash compensation of larger employers. Equity helps close that gap.

It also changes behavior in a useful way. If the company grows, employees with equity participate in that value creation. That doesn't magically make everyone think like an owner, but it does connect compensation to long-term company performance instead of only near-term payroll.

If you want a solid primer on the job-seeker side, Underdog's guide to startup equity basics for job seekers is a useful companion.

Practical rule: Treat equity as part of your compensation architecture, not as a lottery ticket and not as guaranteed income.

What works is using equity to balance a thoughtful offer. The company is honest about the trade-off. The salary is still livable. The grant is explained clearly. The candidate understands the vesting schedule and downside.

What doesn't work is when a company uses “upside” to dodge basic compensation clarity. If a recruiter can't explain the grant in plain language, that's not sophistication. It's a warning sign.

The best candidates I've worked with don't ask whether equity is good or bad in general. They ask whether this specific equity offer is worth taking relative to cash, role quality, and risk.

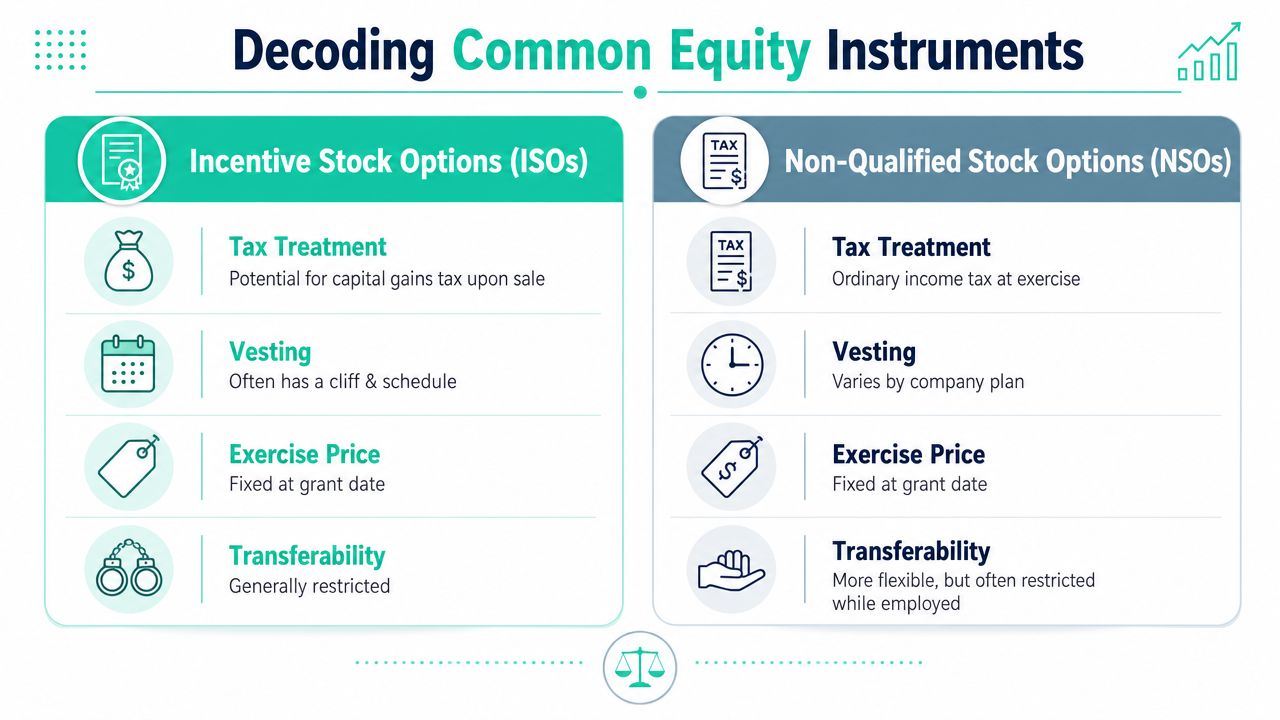

The instrument matters because it determines how value is created, when you receive ownership, and where the tax complexity shows up. As Falcon Wealth Planning explains, RSUs are valued as units multiplied by the current share price, while stock options are valued as the market price minus the exercise price. Options only have intrinsic value when the share price is above the strike price. Falcon also notes that common vesting structures run three to five years with a one-year cliff.

Options give you the right to buy shares later at a set exercise price.

That means options are only attractive if the company's share value eventually rises above that exercise price. If it doesn't, the options may never be worth using. This is why candidates shouldn't confuse the number of option shares with guaranteed value.

There are two option labels candidates hear most often.

A candidate doesn't need to become a tax lawyer to assess options. But you do need to know that two option grants with the same share count can feel very different in real life once exercise cost, taxes, and timing enter the picture.

RSUs are usually easier to understand.

They represent a promise to deliver shares when vesting conditions are met. You don't typically need to make an exercise decision the way you would with options. That simplicity is one reason more mature private companies and public companies often lean on them.

RSUs still aren't “free money.” Their value depends on the share price when they vest, and in private companies there may still be liquidity limits. But for many employees, RSUs are easier to model than options because the mechanics are cleaner.

| Instrument | How value is created | Main practical question |

|---|---|---|

| ISOs | Share value rises above strike price | Can you afford and justify exercise? |

| NSOs | Share value rises above strike price | What happens at exercise from a tax and cash standpoint? |

| RSUs | Shares are delivered as vesting occurs | When do they vest, and when can you sell? |

If your offer letter gives you an equity number but not the instrument type, ask for clarification before comparing offers.

When reviewing a grant, I'd ask these first:

If the written plan and your verbal explanation don't match, slow down. In disputes over offer terms or obligations, general contract concepts matter more than candidates expect. A plain-English resource like LA Law Group's breach of contract guide can help you understand why getting the grant terms in writing matters.

Vesting is the schedule that determines when your grant becomes yours.

You may be promised a certain number of shares or options on day one, but that doesn't mean you own all of them on day one. For restricted awards, ownership is typically delayed by vesting over multi-year schedules, which creates a retention effect because employees need to remain employed to receive the full value, as explained by J.P. Morgan Workplace Solutions.

A one-year cliff is the moment many candidates misunderstand.

During that first stretch, you're working but usually not earning partial ownership month by month in the way people assume. If you leave before the cliff, you may walk away with nothing from the grant. Once you hit the cliff, the first chunk vests, and then the remaining amount typically continues vesting over time.

That structure protects the company from giving equity to people who exit quickly. It also gives employees a reason to stay long enough to contribute meaningfully.

A normal journey goes something like this.

You join with excitement and barely think about vesting in the first few months because you're focused on the product, team, and onboarding. Around month ten or eleven, the cliff suddenly feels very real. After the first vesting event, the grant starts to feel more tangible because some of it is finally earned.

That's why people call vesting golden handcuffs. Not because it traps everyone, but because it changes the economics of leaving.

Staying for equity only makes sense if you still believe in the role, the team, and the company's path. Unvested equity is a factor, not a life plan.

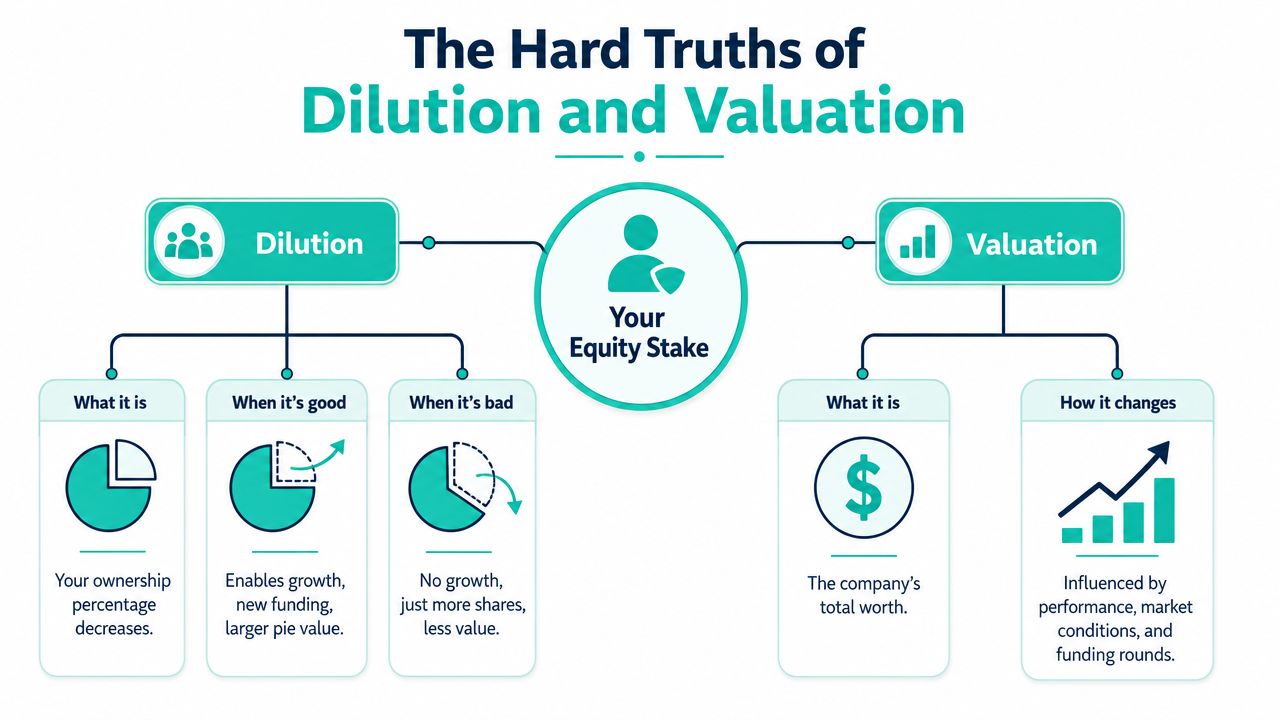

Most candidates hear “dilution” and assume something bad happened.

Sometimes something bad did happen. Sometimes it didn't. Dilution means your ownership percentage can shrink as more shares are created. That often happens when a company raises capital or expands the employee equity pool. Startup equity pools commonly fall in the 13% to 20% range, and grant sizes vary sharply by seniority, while companies now use a mix of options, RSUs, ESPPs, and performance shares for different retention and administrative reasons, according to NASPP's market data discussion.

The pie analogy matters here too.

If the company issues more shares, your slice can get smaller. But if the financing helps the company hire, build, sell, and survive, the entire pie may grow enough that your smaller slice is worth more than your earlier larger slice.

That's the version of dilution founders and employees should be willing to accept.

The bad version is when more shares are created without corresponding progress in company value. Then your percentage falls and the pie doesn't grow enough to offset it.

Candidates often fixate on ownership percentage because it feels concrete. In practice, the better question is what your grant could be worth under reasonable company outcomes.

To think clearly about that, it helps to understand the relationship between enterprise value, capitalization, and total equity. If you want a plain-language finance refresher, Finzer's guide on how to determine a company's net worth is a useful reference point.

You should also learn the mechanics of dilution itself. Underdog's explanation of equity dilution breaks down the topic in candidate-friendly terms.

Ask yourself:

Dilution isn't the enemy. Blind dilution is.

Equity ceases to be a story and becomes a model.

Carta makes the core issue clear in its discussion of equity compensation: the headline grant can be worth far less once dilution, vesting, taxes, and liquidity constraints are accounted for, which is why candidates need a practical way to estimate after-tax, after-dilution, and after-liquidity value before accepting an offer. You can read that framing in Carta's guide to practical equity valuation.

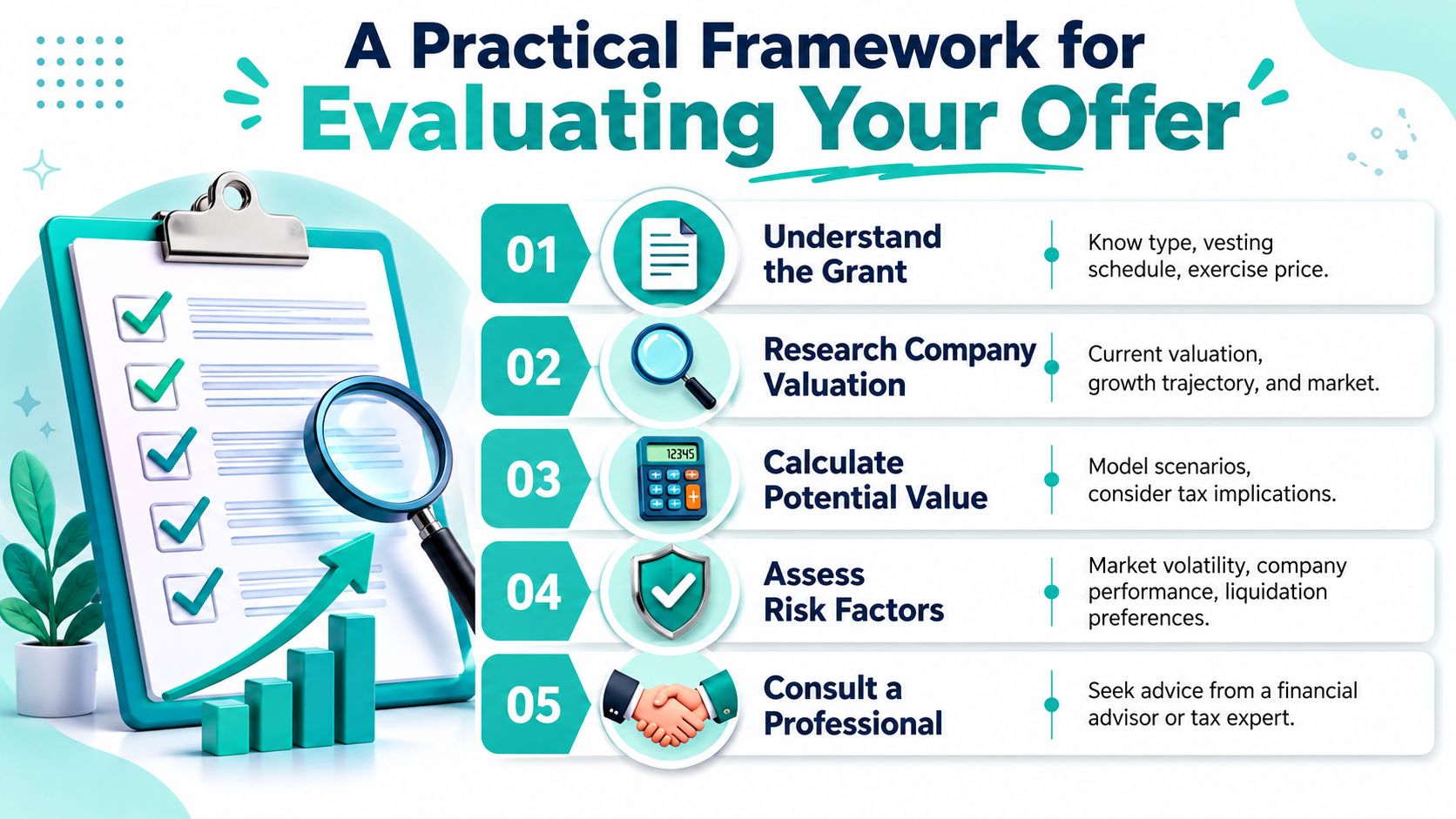

Before you evaluate upside, get the basic facts straight.

If a company can't answer those clearly, you're not ready to compare offers yet.

The most useful candidate questions are usually the least glamorous ones.

Ask for the fully diluted share count. Ask what valuation framework the company uses internally when discussing the grant. Ask what the latest common-share valuation is if they're willing to share it. Ask whether there has been a recent financing round and how the company talks about preferred versus common share economics.

You may not get every answer. Early-stage companies vary widely in what they disclose. But the quality of the response still tells you a lot. Clear answers signal operational maturity. Evasive answers usually mean more uncertainty, not hidden treasure.

Don't reduce equity to one “expected value” number in your head.

Use a few simple scenarios instead:

| Scenario | What to test |

|---|---|

| Conservative | You leave before full vesting, liquidity takes time, taxes reduce proceeds |

| Base case | You stay through meaningful vesting and the company progresses steadily |

| Upside case | The company performs strongly and liquidity arrives on favorable terms |

This exercise matters because equity is a probabilistic future payout, not present cash.

Candidates usually underestimate the drag from real-world constraints.

That's why a smaller amount of cash can sometimes beat a larger-looking equity grant in practical terms.

Candidate checkpoint: If you can't explain your after-tax and after-liquidity downside, you're still looking at marketing, not compensation.

Not every company will increase salary. Not every company will increase equity. But many will clarify terms, adjust one component, or explain refresh expectations if you ask directly.

A useful conversation sounds like this: I understand the headline grant, but I want to evaluate the actual economics. Can you walk me through the share count, vesting, exercise details, and how current employees think about liquidity?

If you want a tool built specifically for startup job seekers, Underdog's startup equity calculator guide can help you structure those inputs and compare scenarios more rationally.

It depends on the plan documents and your grant agreement.

In many cases, vested options don't last forever after departure. You may have a limited post-termination exercise window, and if you miss it, those vested options can expire. That's why you should ask about this before you sign, not when you resign.

The practical question isn't just “Do I keep them?” It's “How long do I have, and can I realistically afford the decision I'll need to make?”

This is a tax election that can matter in certain equity situations, usually when you receive actual stock subject to vesting rather than a more standard option or RSU arrangement.

Whether you should file one depends on your exact grant type, timing, tax position, and risk tolerance. This is one of those areas where internet summaries become dangerous quickly. If your company mentions restricted stock and an 83(b), get professional tax advice immediately because timing is usually critical.

A liquidity event is the moment your equity can potentially turn into actual money. That might happen through an acquisition, an IPO, or sometimes a company-approved secondary sale.

Until then, private-company equity can remain illiquid for years. That's the mistake candidates make most often. They treat vesting as the finish line. It isn't. Vesting means you've earned the asset. Liquidity determines whether and when you can convert it into cash.

Sometimes yes. Often no.

The right answer depends on your cash needs, your confidence in the company, the instrument type, and the quality of the terms. If a lower-cash offer would strain your life, the equity has to clear a very high bar. Ownership upside is appealing, but rent, debt payments, and family obligations are real and immediate.

Look for clarity.

A serious company can explain the grant, define the vesting schedule, discuss the cap table at a high level, and answer reasonable candidate questions without acting annoyed. A vague company may still be promising, but vague equity should be discounted heavily.

If you're exploring startup roles and want more context on how salary, equity, and offer structure compare across early-stage companies, Underdog.io is one place to evaluate opportunities with vetted startups and get more transparency into how offers are put together.