You get a startup offer. The mission is strong, the team seems sharp, and the equity grant looks like the kind of line item that could change your financial future.

Then you read the paperwork and hit a phrase that sounds like it belongs in a venture lawyer's binder: liquidation preference.

A lot of candidates skip past it. Founders sometimes do too, especially when everyone is focused on closing a round or signing an offer. That's a mistake. If you're deciding whether stock options are meaningful compensation or mostly aspirational, this term matters. It helps determine who gets paid first when a company is sold, merged, or otherwise turned into cash.

For a software engineer, product manager, designer, or early employee, that isn't abstract finance. It's directly tied to whether your equity has real value in a decent outcome, not just a spectacular one.

Say you're a senior engineer choosing between two jobs.

The first is a large public company. Compensation is straightforward. Salary, bonus, RSUs, done. The second is a startup with a lower cash package, but a meaningful option grant. The recruiter talks about upside, ownership, and being early. You believe them. You should want upside.

But equity at a startup isn't just about how many shares or options you get. It's also about where your shares sit in line when money gets distributed. Investors usually hold preferred shares. Employees and founders usually hold common stock or options that convert into common stock. That difference can completely change the outcome at an acquisition.

A candidate often compares offers by multiplying option count by a headline valuation. That shortcut can mislead you.

If the company has raised several rounds with investor-friendly terms, a sale that sounds good on paper may still produce very little for common shareholders. That doesn't mean the company is a bad bet. It means you need a better mental model.

One useful starting point is understanding company share capital distinctions. Before you can judge the value of an option grant, it helps to know what kind of shares exist, how many are issued, and why not all equity sits on equal footing.

Career lens: If equity is a big part of your compensation, you're not just evaluating product-market fit. You're evaluating payout mechanics.

When people ask what is liquidation preference, they're usually asking a practical version of the same thing:

Who gets paid first if this company exits for less than everyone hoped?

That question belongs in your job search, your founder fundraising process, and any conversation where someone uses the word “upside” casually.

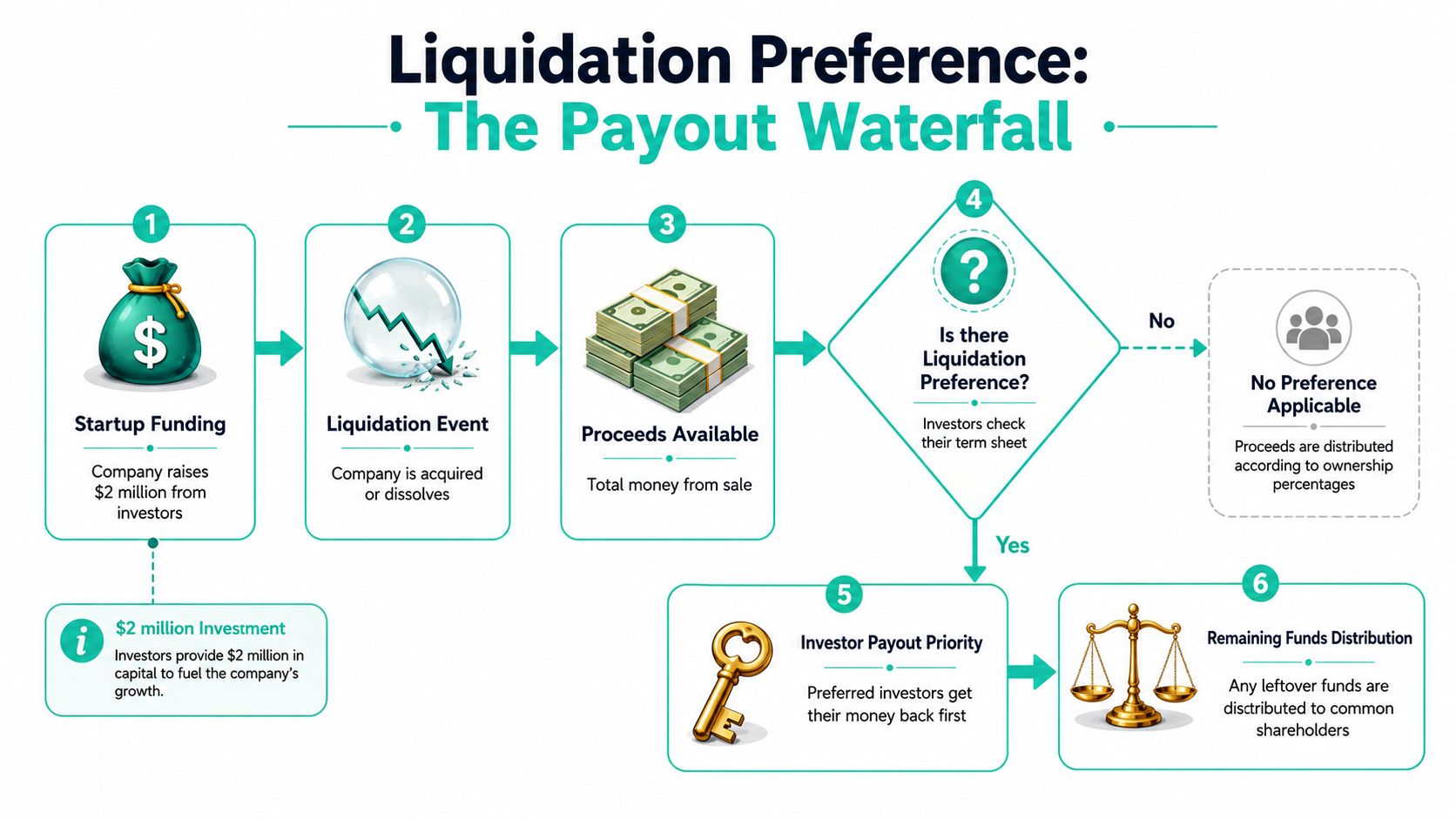

At its core, liquidation preference is an investor's money-back priority.

A verified definition from HSBC Innovation Banking's explanation of liquidation preference puts it this way: liquidation preference is a foundational economic term in venture finance that gives preferred shareholders a fixed multiple of their initial investment, typically 1x, before common shareholders receive any payout in a liquidity event such as a sale, merger, or IPO. The same source notes that this gives investors downside protection because they can take that fixed return rather than rely on their ownership percentage if the exit value is low.

Think of a concert with a VIP entry line.

Everyone bought a ticket to the show. But one group paid for priority access. When the doors open, that group goes first. Liquidation preference works the same way in a company exit. Investors with preferred stock don't own “better” companies than employees do. They hold shares with a priority payment right.

That's the whole concept.

A few terms make the mechanics easier to follow:

If you want a grounding in how startup equity works before getting into preference terms, this primer on startup equity basics for job seekers is a helpful companion.

Startups are risky. Investors know many companies won't exit at huge valuations.

So liquidation preference gives them a floor. If things go badly or just less brilliantly than planned, they may still recover their capital before common shareholders receive anything. That's why people sometimes describe it as downside protection.

Here's the practical takeaway for employees: your option grant can look generous and still sit behind a large investor claim.

A startup exit doesn't begin with “what does everyone own?” It begins with “who gets paid first?”

That's why understanding what is liquidation preference matters so much. It's less about legal jargon and more about payout order.

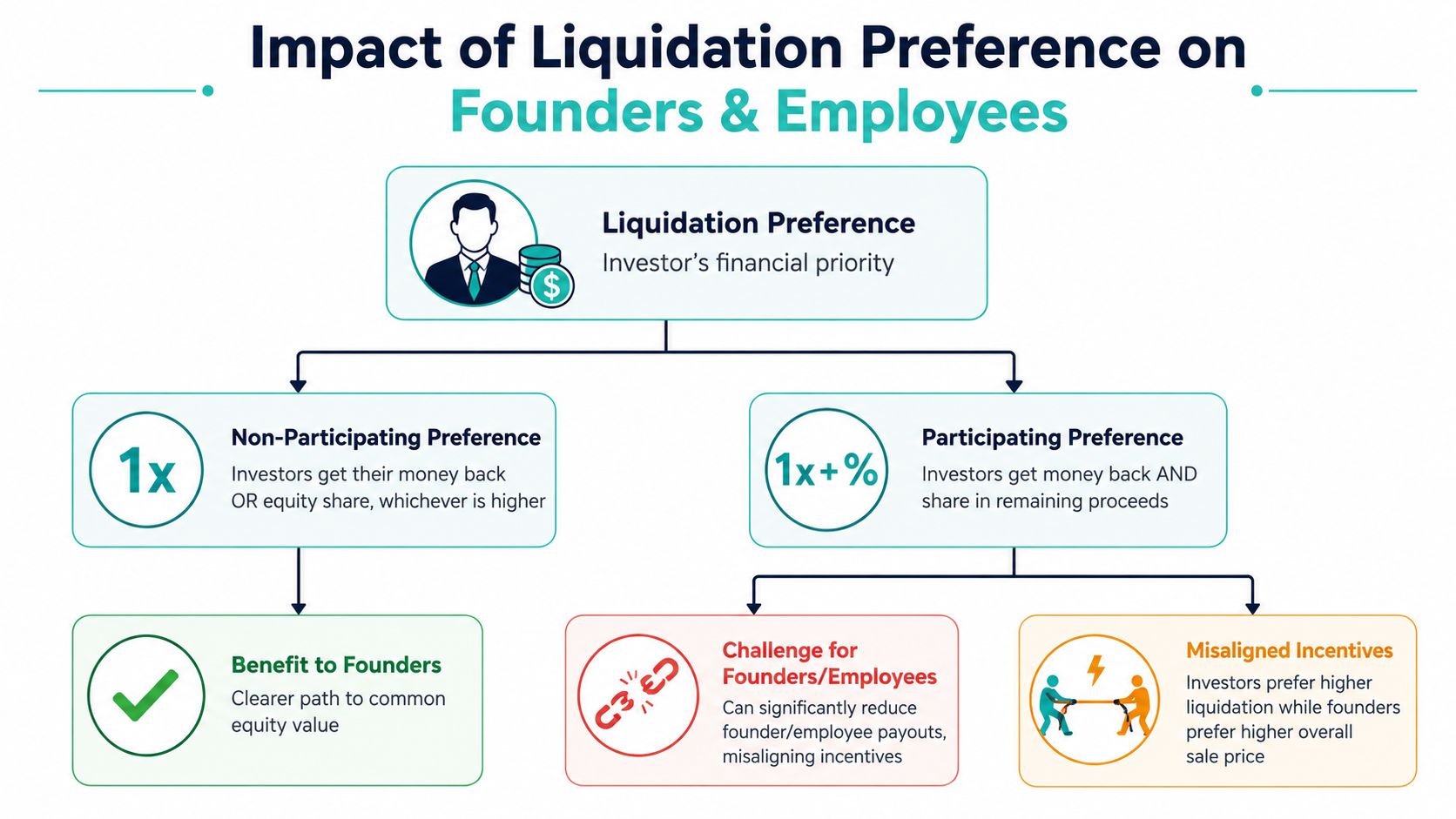

Not all liquidation preferences work the same way. Two mechanics matter most: the multiple and whether the preference is participating or non-participating. As LTSE explains in its founder guide to liquidation preferences, those mechanics determine whether investors take their money back and then share remaining proceeds, or instead choose the better of their preference amount or pro rata ownership share.

This is the version most founders and employees hope to see.

With 1x non-participating, investors get a choice. They can either:

They pick whichever gives them more money. They don't get both.

That “either-or” structure is why this is often seen as cleaner and more founder-friendly. It protects investors on the downside without letting them double dip when the outcome is good.

This one is more aggressive.

With a participating preference, investors first take their preference amount back. Then they also share in the remaining proceeds as if they were common shareholders. In plain language, they get paid twice in the waterfall.

That can significantly reduce what's left for founders and employees in exits that are solid but not massive. It changes the economics most in the middle, where common holders might otherwise have seen meaningful value.

Negotiation lens: When you hear “participating,” translate it to “investors recover capital first and still keep sharing.”

This is the middle ground.

It works like participating preference up to a limit. After investors hit the cap, the extra participation stops. The exact cap depends on the term sheet, so you need to read the clause rather than assume it's harmless.

For candidates, the main point isn't memorizing every legal variation. It's recognizing that capped participating still shifts value away from common holders compared with a standard non-participating structure.

| Preference Type | How It Works | Founder Friendliness |

|---|---|---|

| Non-participating | Investor chooses either the preference payout or conversion to common, whichever is higher | Most founder-friendly of the three |

| Participating | Investor gets the preference payout first and also shares in the remaining proceeds | Least founder-friendly |

| Capped participating | Investor participates after taking preference, but only until a stated cap | Middle ground |

If you're a founder negotiating financing, the headline valuation can distract from the actual economics.

If you're a candidate, you probably won't renegotiate the company's financing terms yourself. But you can still use them as a filter:

Let's make this concrete.

Assume a startup raises $2 million from investors. Those investors hold a 1x liquidation preference. We'll look at three exits: $5M, $20M, and $100M. To keep the math simple, assume the investors own 25% of the company on an as-converted basis and founders plus employees own the other 75%.

One more concept matters before the examples. Wall Street Prep's liquidation preference overview notes a critical breakpoint in the exit waterfall: if the company exits below the aggregate liquidation preference, founders and employees holding common stock can receive zero, because the entire sale price goes to preferred shareholders first.

Under 1x non-participating, the investor compares two options:

The investor chooses $2M because it's higher.

That leaves $3M for common shareholders. Founders and employees split that remainder.

Under 1x participating, the investor first takes $2M. Then the remaining proceeds are $3M. The investor also gets 25% of that $3M, which is $0.75M.

So the investor receives $2.75M total, and common shareholders split the remaining $2.25M.

Under 1x non-participating, the investor compares:

Now conversion is better, so the investor takes $5M as a common shareholder. Founders and employees receive $15M.

Under 1x participating, the investor first takes $2M. That leaves $18M. Then the investor takes 25% of $18M, which is $4.5M.

Total investor payout becomes $6.5M, leaving $13.5M for common shareholders.

That's where the “double dip” shows up clearly. The company had a respectable exit, yet common holders still gave up meaningful value compared with the non-participating structure.

For anyone trying to understand how sale value translates into shareholder payouts, this explainer on business valuation for sellers' payouts is useful context because payout math often starts with what value is available to equity holders.

Under 1x non-participating, the investor compares:

The investor converts and takes $25M. Founders and employees receive $75M.

Under 1x participating, the investor first takes $2M. That leaves $98M. Then the investor takes 25% of $98M, which is $24.5M.

Total investor payout is $26.5M, leaving $73.5M for common shareholders.

The difference between structures is small at the top only if you're looking casually. It's large when you're the person whose options sit in common.

Don't ask only whether the startup can exit. Ask what kind of exit must happen before common stock really pays.

For founders and employees, liquidation preference isn't just cap table trivia. It shapes the value of common equity.

If a company raises multiple rounds, each round can add to the preference stack. And seniority matters. Later rounds often sit ahead of earlier ones, so the payout order can run from the newest investors backward before any value reaches common. That stack can make a moderate acquisition feel much less exciting for the people who built the company.

Employees often hear a story like this: “You own a small piece of a company that could be worth a lot.”

That may be true. But common stock doesn't participate equally in every outcome. If investors have a large claim ahead of common, your equity may need a much stronger exit before it turns into meaningful proceeds.

That's why two startups with similar valuations can offer very different practical upside.

Aggressive preference terms can also create misalignment.

According to Twobirds' discussion of liquidation preference economics, in a $50M exit with a $10M investment at 1x participating, the investor gets $10M first and then also shares in the remaining $40M. The same source notes this can reduce a founder's effective ownership by 10-20% in a mid-range exit compared with a non-participating structure.

That matters because many startups don't end in failure or breakout success. They land in the middle. And the middle is exactly where preference terms bite hardest.

A term sheet can preserve alignment, or it can make founders and employees feel like they're climbing for an outcome that mostly pays someone else first.

If you're considering a startup role, ask questions that reveal structure, not just optimism:

For a broader view of how stock options fit into total pay, this guide to what equity compensation means in practice helps place liquidation preference in the larger compensation picture.

The point isn't to reject every company with investor protections. It's to understand when your upside is real, and when it's mostly a recruiting story.

If you're a founder, liquidation preference is one of the terms worth fighting for early. A slightly lower valuation with clean terms can be better than a flashy valuation paired with harsh economics.

If you're an employee or candidate, you usually won't negotiate investor rights directly. You can still use them to judge the opportunity and negotiate your own package with sharper questions.

A term sheet often signals the key issue in a compact phrase:

You don't need to become a venture lawyer. You do need to know which words affect payout order and whether investors are choosing one path or taking both.

A practical script for candidates is simple:

“Can you help me understand the company's total liquidation preference overhang and whether recent rounds are senior to common?”

That question tells a recruiter or founder you know how startup economics work.

Fiscallion's overview of liquidation preference seniority notes that the most recent rounds are typically senior to earlier ones, so Series B investors are paid before Series A, and Series A before Seed, creating a waterfall distribution order.

That means even if a company's total raised capital seems manageable, the layering can still matter a lot. The newest money may get paid first, then earlier investors, then common if anything remains.

For founders:

For candidates, this guide on how to negotiate stock options can help you turn that understanding into better questions and, sometimes, a stronger equity package.

Usually, no in the practical sense that matters most to employees. In many public listing scenarios, preferred shares convert into common, and the special payout preference no longer functions the same way it does in a private-company sale. If you're evaluating a job offer, liquidation preference matters most for acquisition and downside exit scenarios.

Usually not. Those terms are negotiated between the company and its investors.

But you can absolutely use the information. If a company has a heavy preference stack or investor-friendly participation terms, you may decide to ask for more cash, more equity, or a different strike on the risk-reward tradeoff.

Ask: What is the company's total liquidation preference overhang?

That gets you much closer to the actual economics of your option grant than headline valuation alone.

You should worry less about the number of rounds by itself and more about the structure of those rounds. Senior preferred stacks can push common shareholders further down the payout order. The result is that your options may need a stronger exit than you expected before they produce meaningful value.

No. Some investor protection is normal. Venture financing works because investors take serious risk, and standard terms often reflect that balance.

The issue is whether the terms are clean and understandable, or whether they pull too much value away from common shareholders in realistic exit scenarios.

If you're deciding whether to join a startup, don't stop at option count, strike price, or the latest valuation. Ask how the waterfall works. Ask who gets paid first. Ask how much room is left for common in a decent, not legendary, outcome.

Underdog.io helps tech professionals explore startup roles with more context around what they're joining. If you want opportunities at vetted startups where equity is part of the conversation, you can start with Underdog.io.