You've got the offer. The salary is clear. The title is flattering. Then you hit the equity paragraph and the confidence drops.

It says something like “10,000 stock options,” maybe names a vesting schedule, maybe mentions a strike price later, and suddenly you're doing mental math with variables you don't have. Most engineers can model a distributed system faster than they can translate an option grant into a real financial outcome.

That confusion is normal. Equity is one of the least intuitive parts of startup compensation because the number in the offer letter is not cash, not stock, and not value by itself. It's a contract with timing rules, purchase rules, and cap table context attached.

A useful An Engineer's Guide to Stock Options starts with one mindset shift. Don't ask, “How many options did I get?” Ask, “Under what conditions could these options become worth exercising, and what would I have to spend or risk to get there?”

That's the difference between reading an offer like an employee and reading it like an owner.

A common scenario goes like this. You get a startup offer with a solid base salary and a line that says you'll receive an equity grant after board approval. The recruiter says the upside could be meaningful. You believe them, but the actual document still leaves you with basic questions.

What does “10,000 options” mean if you don't know the total share count? What does a low strike price mean if the company never creates liquidity? What happens if you leave after a year and a half? What happens if the company gets acquired for less than everyone hoped?

Those are the right questions.

Practical rule: Treat equity like a future decision tree, not a bonus. You're evaluating rights, constraints, and possible outcomes.

The first pass is simple. Separate the offer into four buckets:

Most disappointment around startup equity comes from mixing those buckets together. A large grant can still be weak if the strike price is high, the cap table is crowded, or the exercise window is punishing. A smaller grant can still be attractive if the economics and terms are cleaner.

Engineers usually don't need motivational language here. They need a model. Equity gets easier once you stop treating it as a mysterious startup perk and start treating it like a system with inputs, states, and failure modes.

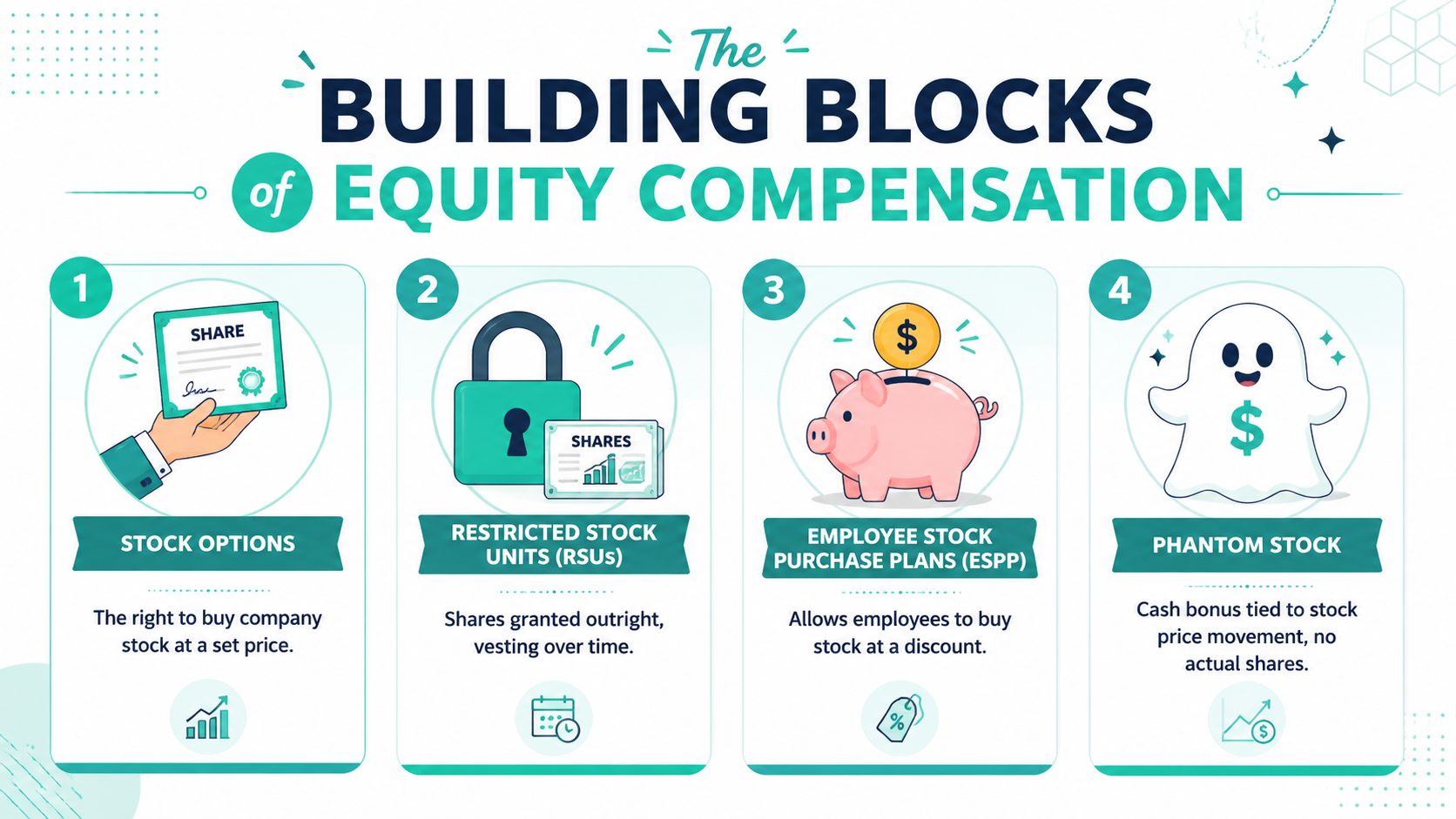

An equity grant is a bundle of rules, not a single number. Two offers can both say “10,000 options” and produce very different outcomes once you look at exercise cost, tax treatment, dilution, and what happens if the company sells before you ever get liquidity.

A stock option gives you the right to buy shares later at a preset exercise price, also called the strike price. Until you exercise, you do not own the shares. You hold a contract.

That distinction matters because engineers often anchor on share count and miss the real variables. An option only has economic value if the future share value exceeds the strike price and you can convert that paper gain into actual cash at some point. A large grant with a high strike price, tight exercise window, or weak exit prospects can be less attractive than a smaller grant with cleaner economics.

The practical question is not “How many options did I get?” It is “What would I need to pay, when would I need to decide, and what paths exist to a payout?”

The equity type changes both the math and the decision process.

| Equity type | What you get | Do you pay to own shares | Main practical trade-off |

|---|---|---|---|

| ISO | Right to buy shares | Yes | Better potential tax treatment if you follow the rules, but more constraints |

| NSO | Right to buy shares | Yes | Broader eligibility and simpler company administration, but exercise usually creates taxable income |

| RSU | Shares delivered when vested or settled | No purchase price | No strike price to fund, but taxes and liquidity timing still drive value |

ISOs are common for employees at U.S. startups. They can be attractive, especially when the strike price is low and you have the cash to exercise early. The trade-off is that the tax benefit depends on holding periods and other rules. Miss those rules and the expected advantage shrinks fast.

NSOs show up more often for contractors, advisers, and sometimes employees. They are easier for the company to issue broadly, but from your side they can create taxable spread at exercise. That makes cash-flow planning more important.

RSUs are more straightforward mechanically. You do not pay a strike price to receive the shares. That usually makes them easier to model at late-stage or public companies, where the stock has a clearer market value. They still raise timing questions around settlement, withholding, and whether you can sell when the shares arrive.

If you do not know which instrument you were granted, ask for the exact award type and the plan documents. “Equity” is too vague to evaluate.

A few terms drive the economics:

These are the fields that belong in your model. They determine how much cash you may need, how much risk you are taking on before liquidity, and how much flexibility you keep if your job or the market changes.

For a candidate-side checklist of what to ask about private equity grants, this private-company stock options guide is useful because it focuses on the missing implementation details, not just definitions.

Once you exercise and become a shareholder, legal rights start to matter as much as grant math. understanding shareholder agreements helps with the part many engineers skip, including transfer restrictions, company repurchase rights, voting provisions, and what can happen in an acquisition.

Equity value comes from instrument type, terms, and company outcome working together. If you only look at share count, you are missing the part that drives the decision.

You join a startup in March with 10,000 options, then get a strong offer elsewhere the following February. On paper, you still "have" 10,000 options. In practice, whether you leave before or after your cliff can be the difference between walking away with nothing and keeping a meaningful chunk of the grant.

Vesting is the mechanism that turns a grant into earned ownership over time. For engineers comparing offers, this is not background legal language. It directly affects retention economics, job-change timing, and whether the grant has any real value yet.

A common startup structure is four-year vesting with a one-year cliff. Carta's overview of vesting schedules and cliffs describes the pattern many private-company employees see: nothing vests during the first year, then a larger portion vests at the cliff date, with the rest vesting in smaller increments after that.

The cliff is the part people underestimate. It creates a sharp step function in value. Before it, the grant may look large but remain entirely unearned. After it, you have crossed the first threshold that places shares in your column.

Say the grant is 10,000 options under a four-year schedule with a one-year cliff. At month 12, 2,500 options vest. After that, the remaining 7,500 vest over the next 36 months, which works out to about 208 options per month.

If you leave at 11 months, you keep 0. If you leave at 18 months, you keep 3,750 vested options and lose the other 6,250.

That is why timing matters. A candidate in month six and an employee in month eighteen may quote the same grant size, but they are in very different economic positions.

| Time at company | Vested outcome |

|---|---|

| Before 12 months | 0 vested |

| At 12 months | 25% vested |

| After 12 months | Remaining amount vests gradually |

| At 4 years | Fully vested |

Companies use cliffs for two practical reasons. First, they want equity to reward people who stay long enough to contribute meaningfully. Second, they want to avoid a messy cap table full of tiny ownership stakes from short tenures.

From the employee side, the trade-off is straightforward. A cliff increases retention pressure early, especially in the first year, and it can distort job decisions near the vest date. I tell engineers to treat this as a cash-flow and risk question, not just a loyalty question. If leaving two weeks later means keeping a meaningful number of options, quantify that difference before deciding.

Keep your own vesting calendar. Use exact dates from the grant documents, not rough month counts from memory. If you want a quick way to model cliff timing and later vesting outcomes, a startup equity calculator for scenario planning helps turn the schedule into numbers you can compare against salary, risk, and expected tenure.

You get an offer with 40,000 options and a base salary that is slightly below market. The recruiter says the equity could be worth a lot. That may be true. The job is to turn "could" into a few concrete outcomes you can compare against cash, risk, and how long you expect to stay.

Engineers usually ask, "What is this grant worth?" The better question is, "Under what conditions does this grant become meaningful, and what would I have to spend or risk to realize that value?" That shift matters because options are not a bonus with a fixed dollar amount. They are a contingent claim on a future outcome.

Start with the core equation:

Potential pre-tax gain = (future share value - strike price) × vested shares

That is the right first model because it exposes the dependency that drives everything else. If the future share value never rises above your strike price, the options have no spread. If it rises a little, the grant may still be economically minor after taxes and exercise cost. If it rises a lot, the grant can dominate the compensation package.

Use three cases. Do not force a single forecast.

This is an engineering exercise, not a prediction market. The point is to test sensitivity. A grant that only looks good in the high case is very different from one that still looks respectable in the base case.

For a first-pass model, gather five inputs:

That last input is the one candidates skip. I see people model upside and ignore the check they may need to write to get it. If exercising vested options would require more cash than you are willing to tie up in a private company, the theoretical upside is less relevant than it looks in the offer letter.

If you want a quick way to organize those assumptions, a startup equity calculator for comparing offer scenarios is useful for turning grant size, strike price, and expected tenure into side-by-side outcomes.

Grant size matters less than many candidates think. Two offers can differ by a large option count and still be economically close if one has a much higher strike price or if you are unlikely to vest much before a probable departure.

Tenure matters a lot. A four-year grant is not a four-year value if you suspect this is a two-year role. Model the shares you are likely to vest, not the full grant, then ask whether that vested portion justifies the cash compensation trade-off.

Exercise constraints matter too. Many option plans have a finite life, and many companies require a decision soon after you leave. The exact rules depend on the plan documents, so read them rather than relying on startup folklore. From a practical standpoint, this means an option can have paper value and still force an awkward timing decision if you resign before a liquidity event.

What works is using the same framework across offers. Put every package through the same model: salary, bonus, option count, strike price, vesting likely to occur during your expected tenure, and cash needed to exercise. That makes trade-offs visible.

What fails is anchoring on the raw number of shares. I have seen candidates prefer the larger grant because it felt bigger, even when the smaller grant had better economics. Share count by itself is a unit, not a value.

Another common failure is treating all upside as equally reachable. It is not. Private-company equity is path-dependent. The company has to create value, your shares have to vest, you may need cash to exercise, taxes may affect timing, and there has to be some way to convert paper value into actual proceeds.

The practical standard is simple. If you cannot explain what has to happen in the low, base, and high cases, and what each case would cost you in time and cash, you do not know what the offer is worth yet.

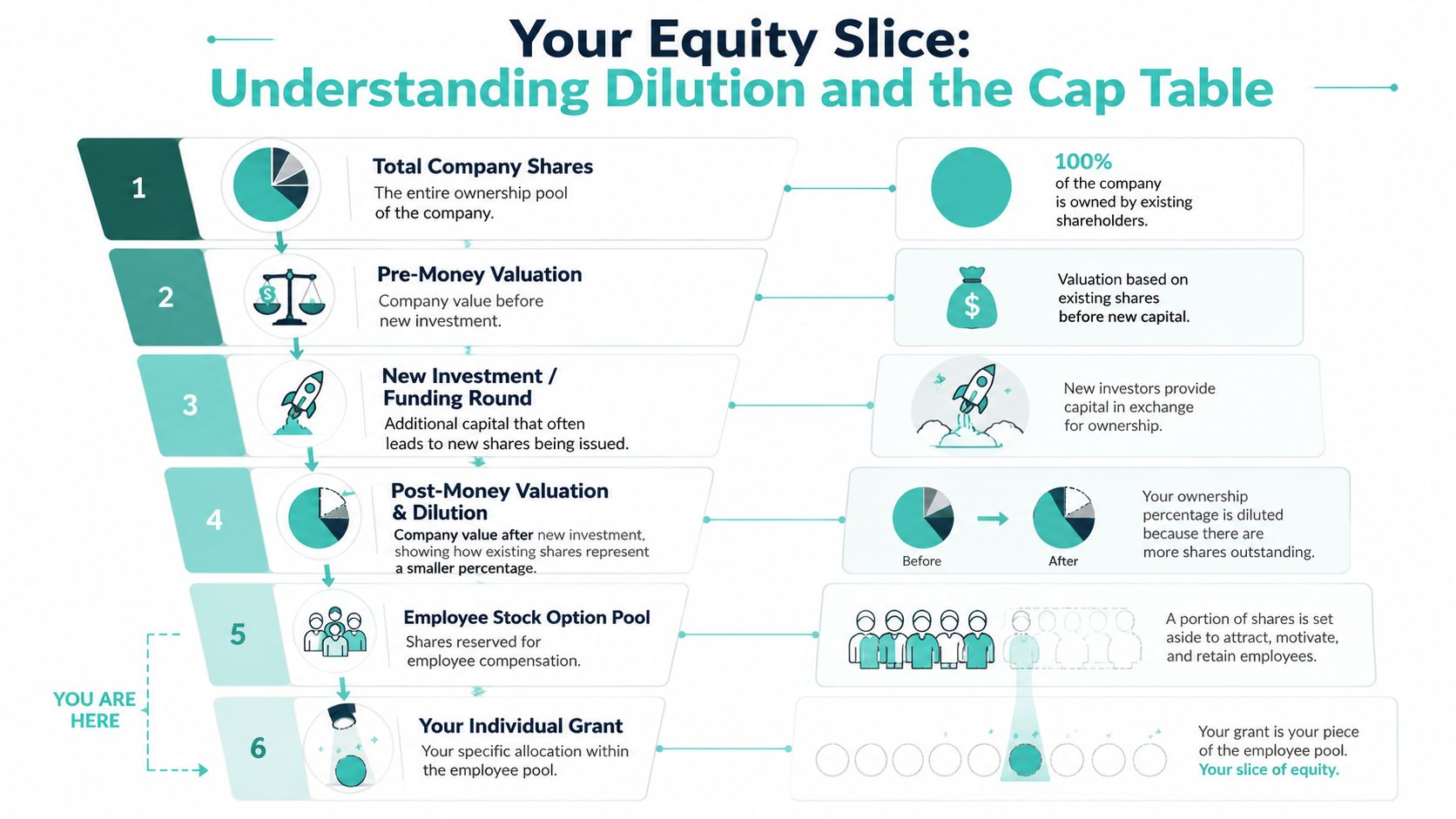

A grant can look generous in an offer letter and still produce a weak outcome for employees. The missing variables usually sit in the cap table: who owns what, who gets paid first, and how much your percentage is likely to shrink before any exit happens.

Engineers often ask whether 0.1% or 0.2% is good. It is a fair first question, but not a sufficient one. The better questions are how many shares exist on a fully diluted basis, how many are reserved for the option pool, what the current 409A says about common stock, and whether preferred investors sit ahead of common in an exit. Alex MacCaw makes the same point in An Engineer's Guide to Stock Options.

Those details matter because percentage alone hides the mechanics.

Dilution works like adding more slices to the pie while your slice count stays fixed. After new financing, a larger option pool, or more hiring, your ownership percentage usually falls. That is normal. It only becomes a problem if the company adds dilution faster than it adds enterprise value.

A smaller share of a much more valuable business can still be a great outcome. A larger share of a company with a heavy preference stack and limited exit paths may not be worth much at all.

The cap table answers a different question than ownership percentage. It tells you who gets paid, in what order, and under what conditions.

That matters because preferred stock often carries liquidation preferences. If the company sells for a modest amount, investors may recover their money first, sometimes with additional rights attached, before common stock participates. Employees hold common or options on common. So an acquisition headline can sound good while the payout to employees is mediocre.

I have seen candidates focus on dilution and miss the bigger risk. Senior preferences can matter more than a few extra basis points of ownership.

Analytical candidates separate themselves by asking questions such as:

Use this framework when you evaluate an offer:

| Question | Why it matters |

|---|---|

| What are total fully diluted shares? | Shows what your grant means in context |

| What is the latest 409A? | Helps you estimate common stock pricing relative to your strike |

| How much preferred capital is ahead of common? | Affects what employees may receive in an exit |

| Has the option pool been expanded recently? | Signals likely dilution pressure |

| What kind of exits fit this business? | Changes the realistic payout range |

One more practical point. A cap table is not just a finance artifact. It affects employee behavior. If a company has raised a lot of preferred capital and still talks about modest exit scenarios, common shareholders need to model outcomes carefully before treating the grant as meaningful compensation.

That is also why tax planning cannot be separated from cap table analysis. If you eventually exercise and hold shares, the after-tax result matters as much as the pre-tax headline. For country-specific planning ideas, it can help to review local accountant tips on reducing tax.

What does not work is accepting “you'll own roughly X percent” as a complete answer. Use the percentage as an input, then ask how dilution, liquidation preferences, and realistic exit values change the actual outcome. That is the shift from learning what options are to understanding how they pay off in real life.

You leave a startup on good terms, then open your grant portal and realize you have a short window to decide whether to wire several thousand dollars for stock you still cannot sell. That is the point where stock options stop being a compensation concept and become a personal balance-sheet decision.

Most guides explain the tax labels. Engineers usually need a decision model. What cash goes out now, what clocks start running, what could expire, and what outcome would justify the risk?

The detail that catches people off guard is the post-termination exercise period, or PTEP. Many companies have historically used a 90-day window. If you leave, you may need to decide quickly whether to exercise vested options or let them expire.

Run the math early. If your strike price is $1 and you have 5,000 vested shares, exercising costs $5,000 before taxes, legal review, or any other planning cost. If that amount would force you to raid emergency savings, the decision is already telling you something.

This is why I tell engineers to treat an option grant like a staged capital allocation problem. You are deciding whether to invest personal cash into a single illiquid asset, with limited information and no guaranteed exit date.

A useful framework is to evaluate exercise timing across four variables:

That framework shifts the question from “Should I exercise?” to “Under what assumptions does exercise produce a better expected outcome than waiting?”

For some employees, waiting is rational. They preserve cash, avoid putting more money into one company, and accept the risk that the options may expire if they leave.

For others, early exercise or prompt exercise after vesting can make sense. The usual reason is not optimism alone. It is timing. Exercise can start holding periods that affect how gains are taxed later, and those clocks do not start while the award is still just an option.

Tax strategy here is mostly about timing and structure, not clever loopholes.

With stock options, the sequence matters. Grant date, vest date, exercise date, sale date, and in some cases whether an election was filed on time can all change the after-tax result. A good pre-tax outcome can still produce a disappointing net result if you exercise at the wrong time or ignore the cash impact.

Section 1202 is one example engineers should at least know exists. In the right fact pattern, qualified small business stock can receive favorable treatment after a long holding period, which is one reason some employees care so much about when they exercise. It does not apply automatically, and it does not mean everyone should write the check early. It means timing can have real value, so the decision should be modeled, not guessed.

If you want a candidate-side reference on how exercise windows and option terms come up in offers, this guide to negotiating stock options is useful because it focuses on practical terms instead of compensation theory.

For broader planning discipline, local accountant tips on reducing tax is a useful reminder to plan before the sale event instead of after it.

A few habits consistently reduce regret:

The common failure mode is delay. People assume they will deal with exercise later, then later arrives during a job change, a financing, or tax season. By then, the range of good options is usually smaller.

You get the offer. Salary looks fine. The equity line is the part that can change the outcome, and it is usually the part with the least context.

Strong candidates separate headline value from actual value. A bigger number of shares can still be a weaker package if the strike price is high, the exercise window is short, or the company cannot explain what the grant means on a fully diluted basis. Engineers tend to do well here because the job is the same as any other system review. Ask for the inputs, understand the constraints, and model the edge cases.

Start with clarity before you ask for changes. A company that wants to hire and retain good people should be able to answer basic questions about the grant:

Those questions do more than signal that you understand equity. They tell you whether the company has its compensation process under control. If answers are vague, delayed, or inconsistent, treat that as useful information. Sloppy option administration creates real costs later.

If you want a candidate-side reference for framing the conversation, this guide to negotiating stock options is useful because it focuses on practical offer terms rather than abstract compensation theory.

After that, negotiate the levers that affect your downside and your flexibility. Share count matters, but it is only one variable. In many cases, a longer post-termination exercise window or an early exercise provision is worth more than a modest increase in the grant because it gives you more control over timing and cash flow. The rules around Section 1202 and exercise timing are a good reminder that tax treatment and holding periods can depend on decisions made long before any exit.

A practical negotiation list looks like this:

| Lever | Why it matters |

|---|---|

| More options | Improves upside if all else is equal |

| Better cash comp | Reduces dependence on uncertain equity outcomes |

| Early exercise provision | Can improve tax timing flexibility |

| Longer post-termination window | Reduces forced cash decisions after departure |

| Clear cap table context | Helps you evaluate real rather than headline value |

One more point matters in practice. Ask what would have to be true for the company to say yes. Sometimes the budget for base salary is fixed, but the equity band has room. Sometimes the reverse is true. Sometimes the company cannot change the grant size for leveling reasons, but it can change refresh cadence, sign-on cash, or exercise terms. You are not trying to win a rhetorical contest. You are trying to find which constraint is real.

Negotiate equity like an engineering decision under uncertainty. Define the variables, test the assumptions, and focus on the terms that change your actual outcomes.

The best package is the one you can explain to yourself in plain English, model with reasonable assumptions, and afford to hold if liquidity takes longer than anyone hopes.

If you're exploring startup roles and want a market where companies reach out with real opportunities, Underdog.io is one way to compare offers from vetted startups while bringing a sharper lens to salary, equity terms, and the trade-offs that matter.