You're probably in one of two spots right now.

You're either a founder with an MVP, a few customer conversations, and one painful realization: the next person you bring in will change the company more than any feature you ship this month. Or you're a candidate looking at an early-stage role and trying to decode whether “co-founder” means actual ownership and influence, or just a flattering title wrapped around an employee package.

That's why co-founders vs founding team members isn't a branding question. It's a decision about risk, reward, and power. It affects who owns what, who decides what, who stays through the ugly parts, and who feels misled later.

Get it right, and you build trust early. Get it wrong, and the damage shows up in cap table tension, awkward investor conversations, broken expectations, and departures that hurt far more than a normal employee exit.

A common founder mistake happens before the company even has enough history to call it a pattern.

One person starts the company. They create the initial vision, talk to users, maybe build a rough product, and then hit the wall. They need help. Usually it's technical help, go-to-market help, or operational help. The person they meet feels indispensable. So the founder reaches for the biggest signal of importance they know: “Come join me as co-founder.”

Sometimes that's right. Often it isn't.

The title sounds generous in the moment, but it creates long-term expectations around ownership, authority, sacrifice, and permanence. If the person is really joining to help execute a defined direction, even very early, that may be a founding team role rather than a co-founder role. The difference matters because the role shapes the company's legal and cultural foundation from day one.

A U.S. Census Bureau working paper on startup team loss found that losing a key founding team member, such as a founder, has an especially large adverse effect on startup performance. The same line of research also notes that losing a non-key founding team member still hurts. Early roles aren't interchangeable. Some departures shake the whole venture.

That's the practical reason this decision deserves rigor. If you call someone a co-founder, you're not just recognizing effort. You're identifying them as part of the core group whose commitment and continued presence materially shape the company's trajectory.

A co-founder title should answer a hard question: if this person leaves, does the company lose part of its original spine, or just a very strong early operator?

Founders often get themselves in trouble. They use “co-founder” to recruit when what they really mean is “first critical hire.” Then later they try to manage that person like an employee, compensate them like an employee, and govern the company without them like an employee. That mismatch rarely stays quiet.

For technical teams, this confusion shows up constantly around the first engineering leader. A founding engineer role can be enormously important without being the same as co-founder. One shapes company inception. The other helps make the company operationally real.

If you're the founder, the safest move is to define the bundle, not the title. What risk is this person taking? What authority will they hold? What equity instrument are you offering? What do you expect when things get hard?

If you're the candidate, ask the same questions before you let the title flatter you into a bad deal.

Most confusion starts because people use these labels socially instead of structurally.

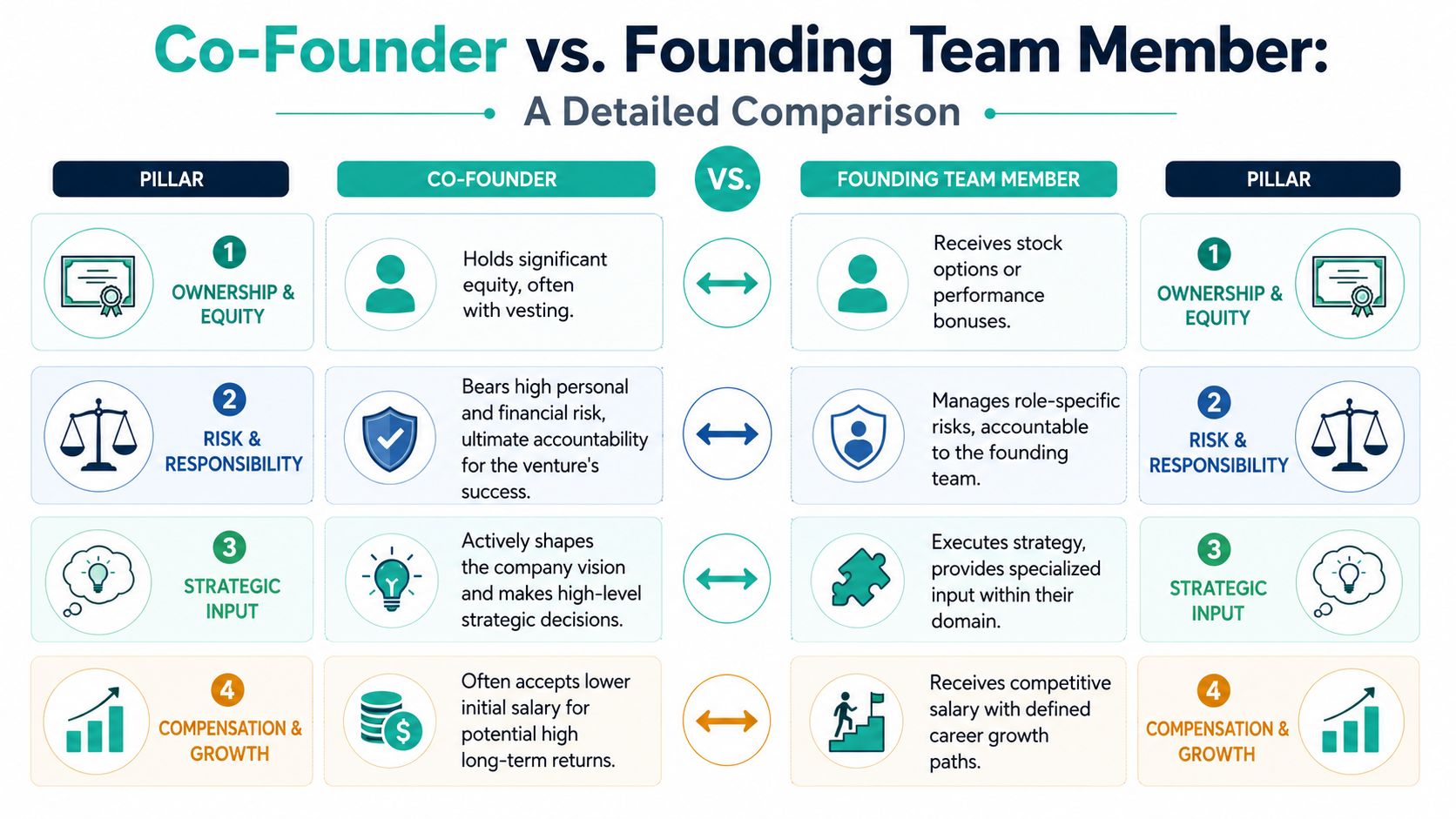

A co-founder is part of the company's originating group. They aren't just early. They share responsibility for creating the company in the first place. That usually means they help define the problem, shape the initial product or business model, absorb meaningful uncertainty before anything is proven, and commit at a level that justifies founder-scale ownership.

This is less about chronology than people think. Joining early doesn't automatically make someone a co-founder. Joining before product-market clarity, before systems exist, and before the business has much structure can matter. But the deeper test is whether the person is sharing in the company's existential risk and helping define its core direction.

A founding team member is an early, high-impact employee. They join when the company is still fragile and undefined in many ways, but they are not necessarily part of the original founding compact. Their job is often to turn intention into execution.

That can mean building the first product team, creating the first sales motion, setting up finance, or owning infrastructure no one else can handle yet. They may have broad scope and unusually high trust. They may influence strategy heavily. But influence is not the same thing as founder status.

Think of it this way:

The distinction also shows up in compensation structure. If you need a primer on how startup ownership works in practice, this overview of equity compensation is useful because it separates the mechanics from the mythology.

Early importance and founder status are not the same thing. Startups fail when they treat them as interchangeable.

A lot of founders avoid saying this plainly because they don't want to discourage candidates. That hesitation creates bigger problems later. A strong founding team member usually doesn't need a fake founder label. They need an honest deal, real scope, and a reason to believe the upside matches the risk.

The fastest way to understand co-founders vs founding team members is to compare the bundle attached to each role.

| Dimension | Co-founder | Founding team member |

|---|---|---|

| Equity instrument | Founder-level common stock | Usually stock options from the employee pool |

| Governance | May have voting rights, board involvement, or direct say in major company decisions | Usually no formal governance role |

| Strategic scope | Helps shape company direction, financing posture, and major leadership decisions | Owns execution inside a function, with varying strategic influence |

| Commitment profile | Expected to carry long-term, company-level responsibility | Expected to perform at a high level in a defined role |

| Risk exposure | Often accepts lower early cash and greater uncertainty in exchange for larger ownership | Takes startup career risk, but typically with more bounded downside and less control |

This is the clearest line.

Carta's 2025 Founder Ownership Report says that in 2024, 45.9% of two-person founder teams split equity equally, up from 31.5% in 2015. The same report says that after a seed round the median founding team collectively owned 56.2%, which fell to 36.1% at Series A and 23% at Series B in its dataset, as shown in Carta's founder ownership data.

That matters because founders start from a position of meaningful ownership that then dilutes over time. Founding team members usually don't start there. As CRV explains in its founder and co-founder guidance, co-founders typically receive founder-level common stock and governance rights, while founding members generally receive options from the employee pool and no board representation.

If you're going to share ownership at the founder level, the legal terms need to be drafted like founder ownership, not improvised in a text thread. A practical primer on that is this shareholder contract explained by Kons Law, which is useful for understanding what should be spelled out before memories and assumptions drift.

A surprising number of people fixate on the title and ignore authority.

A real co-founder often has some combination of voting power, board participation, fundraising input, and a voice in executive hiring. A founding team member may have enormous trust and still have none of those things formally.

Practical rule: If the person has founder language but employee-level governance, treat the offer as an early employee offer until the documents prove otherwise.

This is why “we'll figure it out later” is dangerous. Companies don't become more comfortable discussing power once there's money, pressure, and status involved.

Co-founders are accountable for the whole company, even when their functional specialty is narrow. A technical co-founder might write code, but they also help decide whether to raise, when to pivot, who to hire, and how to allocate scarce resources.

A founding team member can still be broad. The first product designer may define user experience standards. The first engineer may architect the product foundation. The first finance hire may build the company's operating discipline from scratch. But those people usually own a lane inside the company, not the company itself.

If you need a market reference point when shaping these early offers, startup compensation benchmarks can help calibrate salary and equity discussions without collapsing everything into “founder or not.”

This is the least discussed part and often the most important.

Founders absorb identity risk, financial risk, and time risk all at once. They don't just take a job at a fragile company. They become tied to whether the company exists at all. Founding team members take real career risk too, especially early on, but the role is still different if they aren't carrying the same control and downside.

That's why the same person can be indispensable and still not be a co-founder. Importance does not erase structural differences.

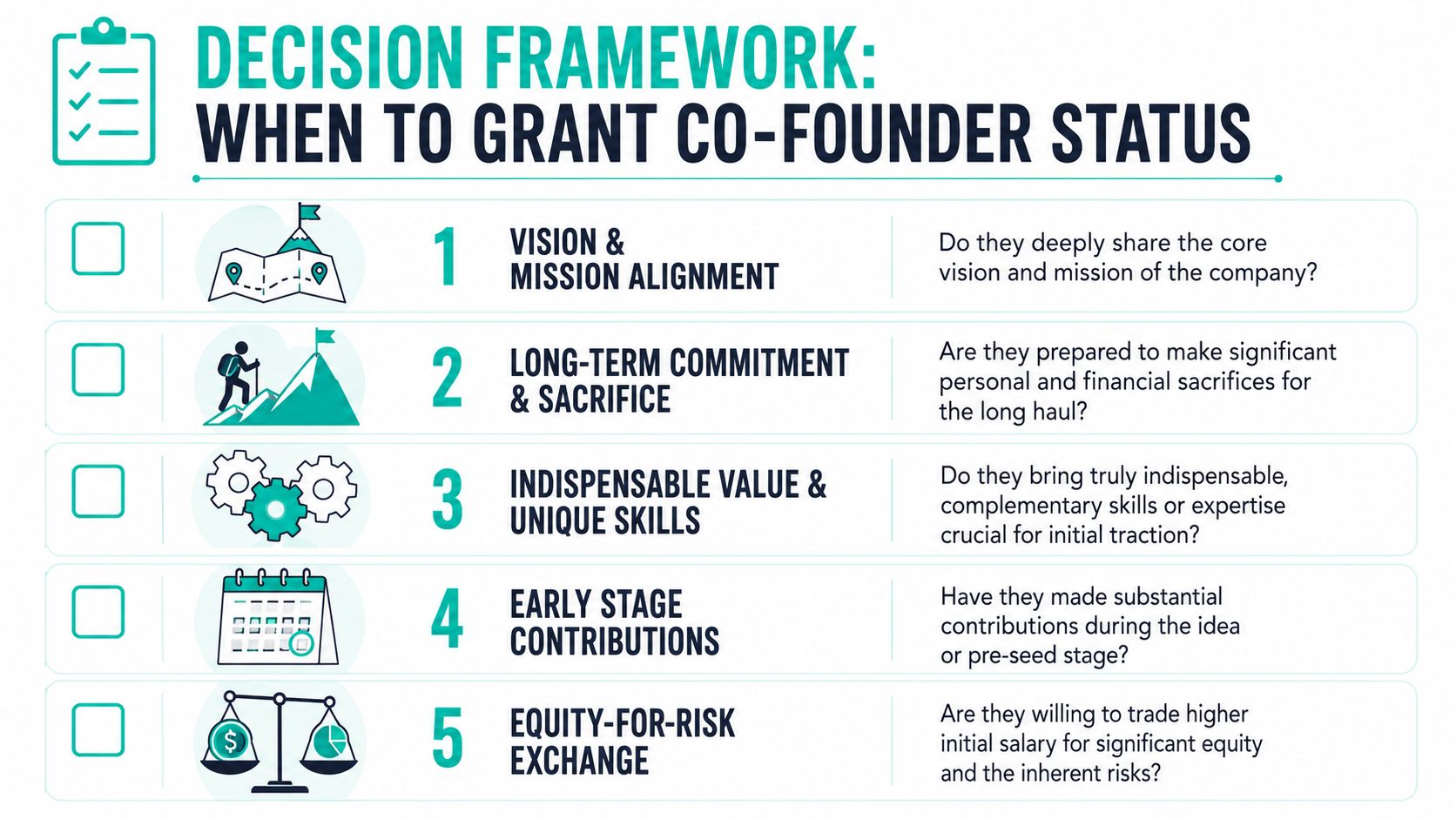

Founders should make this decision with much stricter criteria than most do.

Gust's guidance makes the key point clearly: founders are expected to work full-time for years, which justifies materially larger ownership. Part-time or lower-commitment contributors, however valuable, should receive equity calibrated to their actual time and risk exposure, which aligns more with a founding team member role, as discussed in Gust's piece on co-founders vs founding team members.

That means you should reserve co-founder status for people who clear several tests at once.

Use these questions before you offer the title:

Founders often grant co-founder status because someone joined early, worked hard, or has a close personal relationship with the founder. None of those are enough on their own.

Early arrival is timing. Hard work is expected. Friendship is not a governance model.

If someone's contribution is essential but their commitment is conditional, compensate that contribution fairly without pretending it's a founder relationship.

If the person is extremely valuable but doesn't meet the threshold, you still have strong options:

This is one place where discipline helps both sides. A candidate who deserves co-founder status should want it documented properly. A candidate who doesn't should still want a clean, respectful package that reflects what they're signing up for.

A common early mistake looks like this: the founder cannot afford a true senior hire, does not want to share founder-level power, and still needs someone to build a major part of the company. So the pitch gets fuzzy. Big title, vague equity, unclear authority. Strong candidates usually see through that, and the ones who accept under those terms often become resentful later.

Founders attract better first hires when the offer is honest about three things: risk, reward, and power. That means spelling out what the company has, what it does not have, and what this person will control if they join. Early candidates are not only evaluating compensation. They are deciding whether the trade they are making with their career is rational.

Start with the role itself. The strongest founding team candidates want to build something meaningful, but they also want to know where the walls are. Write the job around outcomes, not startup theater. Explain the problem the company is trying to solve, why it matters now, what is already working, and what is still messy. If the business is pre-product, say that. If customer churn is a problem, say that. If the hire will inherit a blank page with very little support, say that too.

Good early operators are drawn to scope and honesty.

The interview process should test for behavior under uncertainty, not only pedigree. A polished background helps, but first hires earn their keep by creating structure where none exists. Ask for examples of projects they initiated on their own, processes they built before anyone requested them, and decisions they made without full information. The point is to learn how they work when the title is smaller than the responsibility.

This is also where founders need discipline about power. If the role is a founding team position, define the decision rights clearly. Can this person hire? Own budget? Set roadmap within their function? Speak for the company with customers or investors in their area? Serious candidates pay attention to that level of detail because it tells them whether they are being hired to build or to execute someone else's plan.

The offer has to stand on its own. Fair salary matters. So does meaningful equity from the employee pool, clean vesting terms, and a role with visible impact on company outcomes. If you need part-time financial leadership before a full executive hire, practical resources like no-BS part-time CFO advice can help founders think through what to outsource, what to hire, and which decisions should remain with the founder.

Sourcing also matters, but channel quality matters less than message quality. A strong candidate will tolerate risk if the structure is credible. A weak structure does not become convincing because it is wrapped in co-founder language.

The practical rule is simple: do not use a founder-adjacent title to cover for limited cash, limited equity, or limited authority. Strong first hires are usually open to risk. What they reject is confusion.

Early-stage offers often sound bigger than they are. That doesn't make them bad. It just means you need to inspect the structure, not the excitement.

CRV makes the most useful distinction here: true co-founders are typically granted founder-level common stock and may hold board seats or other voting authority, while founding team members usually receive options from the employee pool and no formal governance role, as explained in CRV's guide to the founder and co-founder distinction.

That should be your first filter. Ask what you're being granted. If the answer is vague, slow the conversation down.

Bring these up before you accept:

Some signals should make you cautious fast:

| Red flag | Why it matters |

|---|---|

| “Co-founder” title with employee-level options and no governance | The company may be using the title as a recruiting tool rather than a real structural role |

| Unclear answer on equity class | If they can't explain it, they probably haven't thought it through or don't want you to |

| “We'll sort out the paperwork later” | Later is when leverage changes |

| Founder expects founder-level commitment without founder-level upside | That usually becomes resentment |

| Constant title inflation across the early team | It creates hierarchy confusion and future compensation problems |

If the title is generous but the documents are thin, believe the documents you haven't seen yet, not the enthusiasm you're hearing now.

A good early employee offer doesn't need to cosplay as a co-founder package.

It should be honest about your place in the company, specific about scope, and fair about upside. You should know what success looks like, who you report to, what you own, and how the company thinks about your future. Plenty of outstanding startup careers begin as founding team roles. In many cases, that path is better than a shaky co-founder arrangement because the expectations are cleaner from the start.

If you do want a founder path, ask for founder structure. If the company won't provide it, evaluate the role as a founding team opportunity and decide accordingly.

The healthiest startups don't obsess over titles. They obsess over alignment.

A co-founder role means one thing. A founding team role means another. Both can be highly impactful, meaningful, and financially rewarding. Problems start when a company mixes the language of one with the economics and control of the other.

For founders, the discipline is simple. Don't hand out co-founder status as a recruiting shortcut. Match title to commitment, equity, governance, and actual company-building responsibility.

For candidates, the rule is just as simple. Don't evaluate early-stage offers based on prestige words. Evaluate the package, the authority, the vesting, and the day-to-day reality of the role.

Write it down early. Document ownership, vesting, scope, decision rights, and what happens if circumstances change. That conversation may feel awkward in the first weeks of a company. It feels much worse after money is raised, responsibilities drift, and people start remembering the original deal differently.

The strongest teams aren't built on flattering ambiguity. They're built on explicit agreements that everyone can live with when the company gets harder, not just when it feels full of promise.

If you're exploring startup roles or trying to make your first critical hires, Underdog.io helps connect tech candidates and startups in a format built for early-stage teams, where clarity on role, scope, and growth matters far more than inflated titles.