You're looking at an offer letter that says your base salary is lower than what a bigger company would pay, but there's a grant attached. Maybe it's stock options. Maybe it's RSUs. Maybe it's just a big share number that feels impressive and vague at the same time.

On the other side of the table, a founder is trying to hire someone who already has a good paycheck, solid benefits, and maybe unvested equity they'd have to walk away from. Cash alone usually won't close that gap. Equity is the tool startups use to bridge it.

That's why equity compensation for startups matters. It isn't a bonus. It's a trade. The company asks you to accept uncertainty now in exchange for a claim on upside later. The problem is that many stop at “what percent am I getting?” when the question that matters is simpler and sharper: when does this turn into money you can use?

A talented engineer gets an offer from an early-stage startup. The salary is decent, but not enough to clearly beat a public-company package. Then the recruiter points to the equity grant and says, “That's where the upside is.”

That answer is incomplete.

If the grant is hard to value, impossible to exercise affordably, or unlikely to become liquid, the upside may be more theoretical than real. If the company structures it well, though, equity can change the economics of an offer and the long-term wealth outcome for the employee.

Founders face the mirror image of the same problem. They need equity to recruit people who could work almost anywhere. But they also can't afford to hand out ownership carelessly. Startups typically reserve 10% to 20% of fully diluted equity for employee compensation through an option pool, and early employees at the seed or Series A stage often receive 0.5% to 2% depending on role and seniority, according to Brex's overview of startup equity compensation.

Equity buys alignment, but only if both sides understand the bargain.

For employees, that bargain is:

For founders, the bargain is different:

Equity works when it reflects shared risk. It fails when it's treated like decorative compensation.

A good equity package isn't the one with the biggest share count. It's the one that creates a believable path from offer letter to actual cash.

The pizza analogy helps.

A company is the whole pizza. Equity is your claim on a slice. Different equity types change what kind of claim you have, when you get it, and what you owe along the way.

An option doesn't hand you the slice today. It gives you the right to buy the slice later at a preset price.

That's the key mental model. If the company grows, buying at that old price may be attractive. If the company stalls, the option may never be worth exercising.

There are two common forms.

| Type | Who usually gets it | What matters most |

|---|---|---|

| ISOs | Employees | Potentially more favorable tax treatment, but more rules |

| NSOs | Employees, contractors, advisors, broader recipients | More flexible, usually simpler for the company |

Incentive Stock Options, or ISOs, are typically for employees. They can be tax-advantaged if handled correctly, which is why candidates often prefer them when they have a choice.

Non-Qualified Stock Options, or NSOs, can be granted more broadly. Companies use them for contractors, advisors, and situations where ISO rules don't fit.

The practical difference isn't the acronym. It's the tax trigger and flexibility. If you're an employee, ask which type you're receiving and why. If the company can't answer that cleanly, slow down and get clarity.

Restricted Stock Units, or RSUs, work differently. An RSU is not the right to buy a slice later. It's a promise that the company will hand you the slice when vesting conditions are met. No purchase is required.

That sounds simpler, and in some ways it is. But private-company RSUs can create awkward timing because you may owe tax when they vest even though you can't yet sell the shares. If you work across borders, the mechanics get even more layered. For a useful country-specific breakdown, Fintrack has a practical guide on managing RSUs for Canadian employees.

Stock Appreciation Rights, or SARs, tie your payout to the increase in share value. You benefit from appreciation without necessarily receiving actual shares.

Some companies use SARs when they want incentive alignment without full cap table complexity. For employees, the main question is whether the instrument creates a clear, realistic payout path.

Practical rule: If you can't explain your grant in one sentence using plain English, you shouldn't accept it yet.

Here's the plain-English version:

That's the level of clarity both candidates and founders should demand.

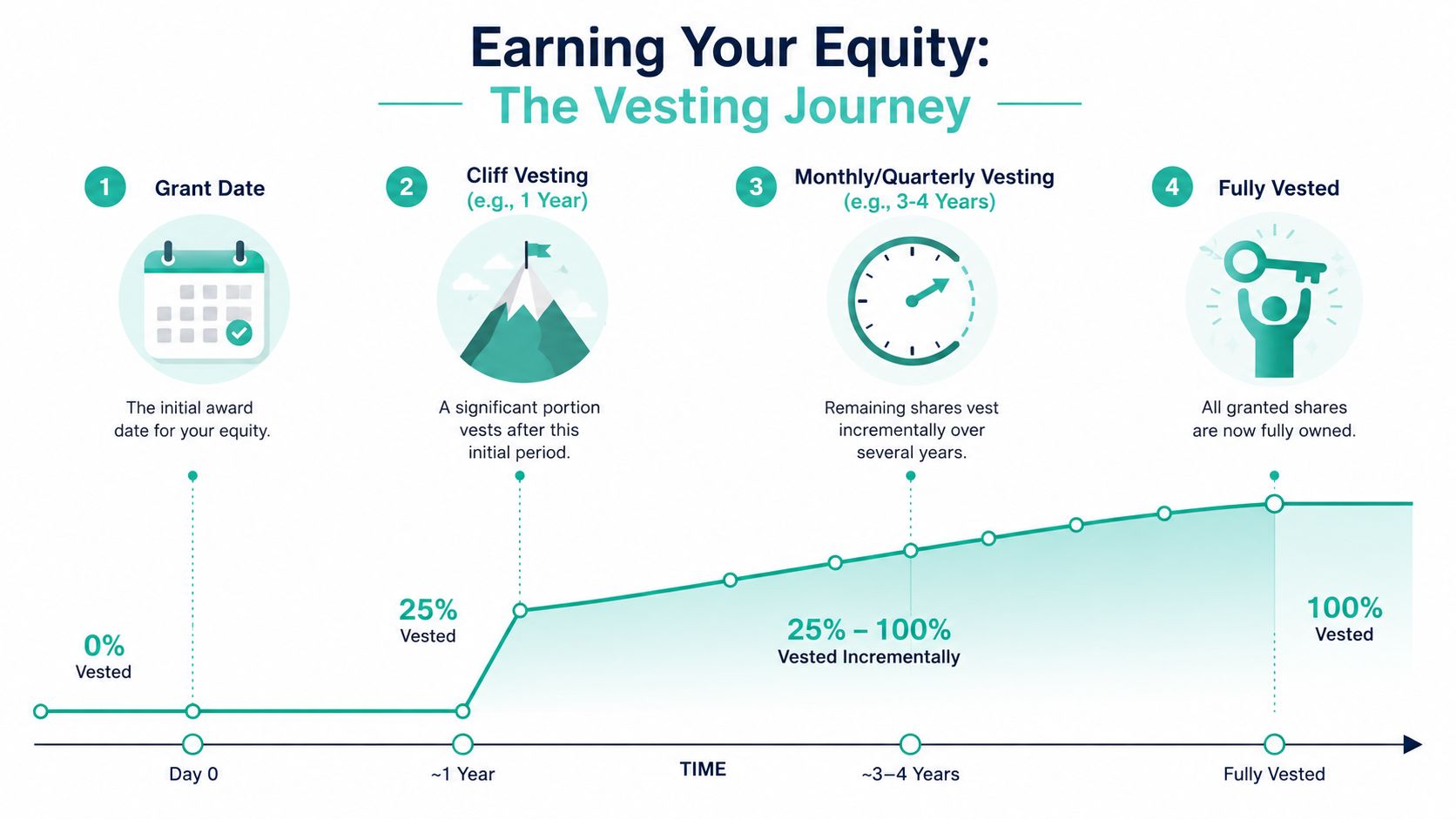

A grant letter is only the start. You don't own most startup equity outright on day one. You earn it over time through vesting.

The visual version helps.

Think of vesting as an engagement period. The company is saying, “We want you to share in the upside, but only if you stay and help build the thing.” You're saying, “I'm willing to tie part of my compensation to a longer-term outcome.”

A common startup structure is a four-year vesting schedule with a one-year cliff. The cliff is the first major milestone. If you leave before it, you usually get nothing. After that, the rest typically vests in smaller increments over time.

If you want a more detailed walkthrough of common timelines and why they matter, Underdog has a useful piece on the equity vesting schedule.

The share count gets attention. The fine print determines whether the grant is usable.

Here are the terms people underweight:

An acquisition isn't always great for employees. Sometimes the buyer wants the team, not every legacy compensation promise.

That's why acceleration matters.

There are two patterns you'll hear discussed:

| Clause | What it generally means | Why you care |

|---|---|---|

| Single-trigger acceleration | Vesting speeds up upon a change in control | More employee-friendly, less common for broad grants |

| Double-trigger acceleration | Vesting speeds up only if there's both a change in control and a qualifying termination event | More common and often more negotiable |

A candidate who negotiates acceleration, or a longer post-termination exercise window, may improve the practical value of the package without changing the number of shares at all.

The best equity term is often the one that keeps your upside alive if your employment ends at the worst possible moment.

Founders should pay attention here too. Clear vesting mechanics make the company more fundable and the compensation plan more defensible. Sloppy terms create confusion, and confusion becomes resentment fast.

Most candidates anchor on the share count because it's the easiest number to see. That's a mistake.

10,000 options can be life-changing or nearly worthless. Without context, it's just a number. Real analysis starts when you convert the grant into ownership, then into potential value, then into realistic cash scenarios.

Ask for the fully diluted share count. That's the share total assuming all options and similar instruments are counted. Then ask what percentage your grant represents on that basis.

Startups don't hire with raw share numbers. They hire with slices of the company. A small slice of a small pie and a small slice of a larger, more mature pie are very different offers.

Recent compensation data shows how much stage changes the math. Base salaries moved only modestly, with 1% to 2% increases, while equity grants fell sharply. H1 2025 data showed a 36% decrease in equity compensation grants compared with prior years, and a mid-level software engineer might see 0.3% to 0.7% at seed versus 0.2% to 0.4% at Series B, according to CandorIQ's startup compensation equity guide.

For options, ask for the company's latest 409A valuation and your strike price.

The back-of-the-napkin framework is simple:

That gives you a rough current paper gain if you exercised today.

A practical way to sanity-check multiple offers is to use a framework like Underdog's startup equity calculator, then pressure-test the assumptions yourself.

Suppose you have an option grant. You know:

That's enough to build three scenarios:

| Scenario | What to assume | What you're looking for |

|---|---|---|

| Base case | The company grows, raises more money, and exits modestly | Whether the grant still beats the salary gap |

| Strong case | The company executes well and liquidity arrives on a favorable timeline | Whether the upside is meaningful after dilution |

| Flat case | The company survives but equity stays illiquid or the spread stays narrow | Whether you can live with the cash comp alone |

At this point, individuals finally ask the right question. Not “What's my percentage?” but “What kind of exit would need to happen for this to matter after dilution and taxes?”

Your percentage will usually shrink as the company raises capital and expands the option pool. That doesn't automatically mean you're losing. If the total company value grows enough, a smaller percentage of a much more valuable company can still be a better outcome.

But you do need to model it accurately.

The logic for founders is similar. Generic grant tables often create problems because they ignore candidate-specific risk and future dilution. A more grounded approach is the risk-anchored equity view. Rather than assigning arbitrary benchmark grants, it calibrates equity to the value gap between what the candidate is leaving and what they're risking. That matters, as 90% of startups fail and financing rounds dilute everyone at different stages. The same framework notes that seed rounds can involve 15% to 25% dilution and Series A rounds 20% to 30%, which is why static grants often age badly, as discussed in Ravio's guide to equity compensation for startups.

Ask these five questions, in this order:

If the company gives crisp answers, the offer is probably being handled by adults.

If you get hand-waving, the issue usually isn't only the equity. It's the operating discipline behind it.

Startup equity can create wealth. It can also create a tax bill before you've seen a dollar of cash.

That's the part people learn too late.

The cleanest way to think about taxes is by asking what event creates them.

That last one is the trap. AMT, or the Alternative Minimum Tax, is the reason an employee can exercise options in a private company and still face a meaningful tax obligation without selling anything.

The biggest mistake in equity conversations is obsessing over grant size while ignoring the path to cash. The most critical employee question is still, “how and when does this become cash?” Realistic liquidity windows are often 2 to 5 years, and with more secondary activity in the market, candidates should pay close attention to early exercise rights and acceleration clauses rather than fixating only on headline percentage, as noted in Titan's discussion of startup equity compensation.

That issue is especially important if you're leaving unvested equity somewhere else or stretching financially to join a startup. If you need a tax professional to walk through private-company equity tradeoffs, a firm that offers financial clarity for NYC clients can help frame the questions before you sign.

Don't treat exercise as an administrative step. Treat it like an investment decision.

Ask:

A private-company share can make you taxable before it makes you liquid.

Candidates often want certainty where none exists. That's fine. The goal isn't certainty. It's avoiding preventable mistakes.

For founders, the tax lesson is simpler. If your team can't understand the tax trigger, they'll either undervalue the grant or resent it later. Neither outcome helps recruiting or retention.

Most equity negotiations focus on the wrong variable.

Candidates push on the number of shares. Founders defend the cap table. Both sides would do better by negotiating the package as a risk-and-liquidity instrument, not just an ownership percentage.

If you're evaluating equity compensation for startups, the best negotiation points often reduce risk rather than inflate optics.

Start with questions like these:

For a practical framework on how to raise those issues without sounding adversarial, Underdog has a concise guide on how to negotiate stock options.

A lot of startup equity policy still sounds like this: “first engineer gets around X,” “second PM gets slightly less,” “everyone after that gets some discount.”

That approach creates inconsistency fast. It also ignores the actual risk the person is taking.

A better system starts with internal leveling and then adjusts for context. One useful rule of thumb is that if a junior hire gets 1x, a mid-level hire should get 2x, and a senior hire should get 4x. The standard discount per subsequent hire has also tightened from 20% to 10%, reflecting stronger demand for early-stage talent, according to Pear VC's guidance on structuring equity for early hires.

Founders don't need a perfect spreadsheet religion. They need a policy they can explain and defend.

A practical system usually includes:

| Decision area | What works | What fails |

|---|---|---|

| Leveling | Tie grants to scope and seniority | Let every manager invent their own ranges |

| Risk adjustment | Increase grants for candidates giving up more certainty | Ignore foregone compensation and unvested equity |

| Liquidity terms | Be clear on exercise windows and acceleration | Treat legal terms as afterthoughts |

| Candidate communication | Explain percentage, dilution, and path to cash | Lead with raw share count |

Founders who hire through startup-focused channels often get pushed toward greater compensation clarity because candidates ask better questions. Platforms like Underdog.io, which connect startup candidates and employers in a curated hiring marketplace, tend to surface these conversations earlier in the process because equity is often central to the role.

Negotiation lens: Don't ask only, “Can I get more?” Ask, “Can this package fail in a less painful way?”

Employees don't expect zero risk. They expect coherence.

If two similar hires get wildly different grants because one negotiated harder, your equity plan becomes political. If every hire gets the same benchmark despite radically different tradeoffs, your plan becomes unfair in another direction.

The strongest approach combines a clear ladder with candid discussion of risk, liquidity, and what the company can realistically support. That's what keeps the package competitive without poisoning the cap table.

Startup equity is a bet. Salary is money you can spend now. Equity is a chance to build wealth later.

The right decision depends on four things: whether you understand the instrument, whether you can estimate its realistic value, whether you're prepared for the tax timing, and whether the path to liquidity is believable. For founders, the same logic applies in reverse. A strong package is one candidates can understand and trust.

If you believe in the company, can absorb the risk, and the terms hold up under scrutiny, equity can be a powerful part of compensation. If not, a bigger share count won't save a weak offer.

If you're exploring startup roles and want to compare offers with better context around salary, stage, and equity, Underdog.io helps candidates get introduced to vetted startups through a single application, with a hiring process built around early-stage tech roles rather than broad job-board noise.

{kind=link}