You finally got the startup offer. The salary is easy to read. The title makes sense. Then you hit the equity paragraph and the confidence drops.

It says something like: you'll receive stock options, they vest over time, there's a cliff, and the details will be in a separate grant document. That's usually the part with the most upside and the most confusion. Candidates often spend hours negotiating base pay, then sign the equity section without understanding what they've agreed to.

That's a mistake.

An equity vesting schedule tells you when you earn the grant, what you lose if you leave, and how your compensation changes if the company gets acquired. It also affects later decisions that have nothing to do with your day-to-day job, including whether you need cash to exercise options and whether taxes show up before any liquidity does. If you want a useful primer before diving into the legal docs, Underdog's guide to private company stock options is a good starting point.

A candidate once showed me an offer and asked the wrong first question. They asked, “Could this be worth a lot someday?” The better question was, “What exactly do I earn, and when?”

That's the practical lens you need. Equity is not a lottery ticket you either hit or miss. In a startup job offer, it's a compensation component with rules attached. Those rules decide whether you walk away with nothing if the role isn't a fit, whether you keep a meaningful stake after two years, and whether a company sale helps you or leaves you with less than you expected.

Most offers translate into a few immediate realities:

A strong startup offer isn't just about how much equity appears on paper. It's about when it vests, what happens if you leave, and whether you can actually use it later.

Candidates who understand vesting negotiate differently. They ask better questions. They stop treating equity as a vague upside story and start treating it like part of their total comp.

That shift matters most when the market is noisy. If you're joining early, switching from a public company, or weighing multiple startup offers, the vesting terms often tell you more about the company's philosophy than the recruiting pitch does.

Think of equity as compensation you earn in installments by staying and contributing, not as something fully handed to you when you sign. The company grants you a fixed amount upfront, but ownership rights build over time according to the equity vesting schedule.

That schedule usually has three basic parts.

The grant is the total amount of equity the company says you're eligible to earn. If your offer says you received stock options, that number is your starting promise.

Vesting is the earning process. It determines when pieces of that grant become yours.

The cliff is the waiting period before the first chunk vests. If you leave before the cliff, you usually get none of that grant.

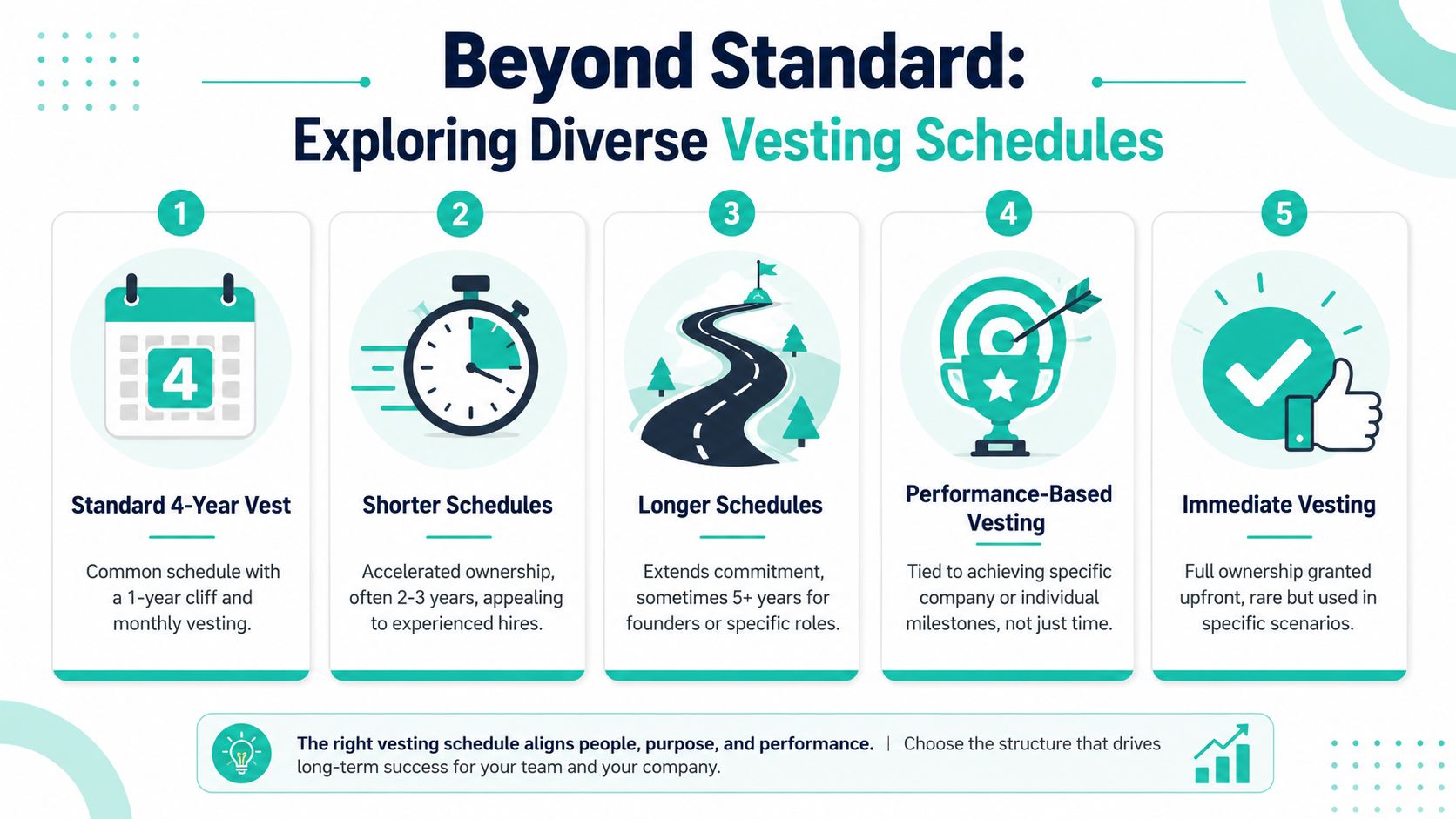

The most common setup in startup and VC-backed companies is a 4-year vesting schedule with a 1-year cliff. Under that structure, you vest 0% in the first year, then 25% vests at the 12-month mark, and the remaining 75% typically vests in equal monthly installments over the next 36 months, often calculated as 1/48th of the grant per month after the cliff, as described by Wise's explanation of the standard vesting schedule.

That sounds technical, but the practical meaning is simple. Stay less than a year, and you usually leave with nothing from that grant. Stay past the cliff, and your ownership starts accumulating on a regular basis.

Here's why companies like this model:

The standard schedule is common for a reason, but “standard” doesn't mean “safe to skim.”

Look for these points in the grant paperwork:

Practical rule: Never assume the summary in the offer letter controls. The grant agreement is where vesting actually lives.

The default model gets most of the attention, but companies don't all use the same structure for every person. Vesting can be monthly, quarterly, annual, or lump-sum, and custom schedules are often used for executives or advisors, as noted in UpCounsel's discussion of vesting schedule variations.

That matters because the right question isn't only “what is vesting?” It's “why did they choose this schedule for this role?”

Most startup employees get time-based vesting. You remain employed, time passes, and more of the grant vests. It's straightforward and easy to administer.

Milestone-based vesting works differently. Equity vests when someone or the company reaches a defined event, such as launching a product, completing a technical deliverable, or hitting a regulatory milestone. This can make sense when a role is tightly tied to a specific result.

Performance-based vesting ties equity to measured outcomes. The trigger might be individual performance, team targets, or company-level goals. This is more common in senior compensation design than in broad employee grants because it creates judgment calls and documentation issues.

Here's the simplest way to compare them:

| Schedule Type | Trigger for Vesting | Best For |

|---|---|---|

| Time-based | Continued service over time | Most employees at startups |

| Milestone-based | Completion of a defined event or project | Roles tied to a narrow strategic objective |

| Performance-based | Hitting specified metrics or targets | Senior leaders or highly customized grants |

| Hybrid | Time plus milestone or performance conditions | Situations where retention and outcomes both matter |

| Lump-sum or immediate | Vesting occurs all at once or upfront | Rare cases, often special hires or unusual arrangements |

Time-based vesting works because it's predictable. Candidates can understand it, finance teams can track it, and the board can approve it without endless interpretation.

Milestone and performance structures can work, but only when the trigger is drafted with precision. If the milestone is vague, you get arguments later. If the performance metric depends on factors outside the employee's control, the schedule stops feeling like compensation and starts feeling like a moving target.

What usually doesn't work is borrowing an executive-style structure for a mid-level hire without a clear reason. It creates complexity without solving a real problem.

Companies often reserve custom schedules for roles where the market pressure is different or the contribution profile is unusual.

The lesson for candidates is straightforward. If your terms differ from the broad company norm, ask why. Sometimes that indicates negotiating strength. Sometimes it's a sign the company is improvising.

Vesting acceleration becomes relevant when the company is sold or undergoes another major change in control. This is the clause that determines whether some or all of your unvested equity vests faster than originally planned.

A single-trigger acceleration clause means vesting speeds up after one event, usually the sale of the company. If the trigger happens, the unvested portion covered by that clause accelerates.

A double-trigger clause requires two events. First, the company changes control. Second, your employment ends under specified conditions, often termination without cause.

For candidates, the practical difference is sharp:

An acquisition can sound like the ideal outcome, but it doesn't automatically mean your unvested equity becomes yours. If the buyer wants to retain staff, they may keep the existing vesting schedule in place. If they don't keep you, the acceleration clause decides whether you leave with more than your vested amount.

If you're a senior hire, acceleration is not a niche legal footnote. It's part of your economic package.

Junior and mid-level candidates often won't get much movement here. Senior leaders sometimes will, especially if they're taking on meaningful execution risk or joining at a fragile stage.

When you review the grant documents, don't just ask whether acceleration exists. Ask what event triggers it, how much accelerates, and whether the definitions are narrow or broad.

Vesting becomes clearer once one runs the numbers on a real grant. The math isn't difficult. The consequences are.

If you want a complementary walkthrough of startup equity basics from the employee side, Underdog's engineer's guide to stock options is useful alongside the calculations below.

Say your grant is 48,000 options on the common four-year structure described earlier.

Under that structure, nothing vests during the first year. At the one-year mark, 25% of the grant vests. For a 48,000 option grant, that means 12,000 options vest at the cliff. After that, the remaining 75% vests in equal monthly installments over the next 36 months, often as 1/48th of the original grant each month, based on the standard schedule described by Wise earlier in this article.

Now assume you leave after 30 months.

Your vested amount would generally be:

The remaining 18,000 options would usually be unvested and forfeited when you leave.

That's why the departure date matters so much. Leaving shortly before a vesting date can mean walking away from equity you were days away from earning.

Now take the same 48,000 option grant and assume the company is acquired at 18 months.

By that point, absent any acceleration:

That leaves 30,000 unvested options.

Outcomes then depend on your acceleration clause:

The same grant can lead to very different outcomes depending on one clause many candidates never ask about.

This is why offer evaluation isn't just about grant size. Schedule plus timing plus trigger language determines the actual economics.

Candidates often think vesting answers the whole equity question. It doesn't. Vesting tells you when you earn rights under the grant. It does not, by itself, tell you when you can sell, when you owe taxes, or how much cash you may need to come up with.

Carta draws a critical distinction between grant, vesting, and taxable events, and notes that vested options may still be subject to exercise limits and tax implications. The practical candidate question is therefore not just how much vests, but when taxes may be due and when equity can realistically be monetized.

If you have stock options, vesting usually means you've earned the right to exercise some portion of the grant. It doesn't mean cash appears in your account. It doesn't mean the shares are liquid. And it doesn't mean there's a buyer.

Candidates often encounter a surprise. They see a vested number in a dashboard and assume they've captured value. In reality, they may still need to decide whether to exercise, whether they can afford to do it, and whether doing so creates tax consequences before any exit event.

When you get the grant paperwork, work through these issues carefully:

NASPP's guidance is especially useful here because it frames vesting as a precision-sensitive legal and cap-table mechanism. Vesting happens in discrete tranches, and rounding rules, day-count conventions, tolling mechanics, and trigger definitions can materially change outcomes.

That sounds abstract until it isn't. A different definition of termination, a different treatment of partial periods, or a different trigger wording can shift ownership timing and tax timing in ways that matter.

If you want a legal lens on the broader compliance environment around private securities, FINRA rules for private investments provide useful context on how private transactions are regulated and why documentation deserves careful review.

Your equity documents are not administrative clutter. They are the instructions for how your compensation behaves when things go well, and when they don't.

Most candidates won't negotiate the entire structure from scratch. Companies usually standardize broad equity terms across employees. But that doesn't mean you're powerless.

What's often negotiable is the economic package around the structure. Grant size may move. Refresh expectations may be clarified. Senior hires may get a conversation on acceleration, cliffs, or post-termination treatment. And sometimes the most valuable negotiation point is getting precise answers in writing.

Use a direct checklist:

If you're working in a state with a lot of startup hiring, it also helps to understand the wider employment contract environment. For example, these California employment contract factors are a practical reminder that equity terms sit inside a larger legal relationship, not a standalone perk.

A vesting schedule can look familiar while hiding important differences. NASPP notes that vesting mechanics depend on drafting details such as rounding rules, day-count conventions, and trigger definitions, which can materially affect ownership and tax timing. That's exactly why careful review matters in negotiation, not just after signature.

A few candidate red flags:

For candidates exploring startup offers through curated channels, Underdog's guide on how to negotiate stock options is a practical companion to the questions above.

If you're comparing startup offers and want access to companies where equity is part of a serious compensation conversation, Underdog.io lets tech candidates submit one application and be considered by vetted startups and high-growth teams across the US.