You got the good news. A term sheet landed in your inbox, or a startup offer finally looks serious. Then the spreadsheet shows up.

It has share counts, valuation, SAFEs, option pools, and ownership percentages that look precise enough to matter and opaque enough to derail the whole conversation. The common response is to scan for the one number they recognize, then hope the rest is fine.

That's risky from both sides of the table.

A founder can give away more ownership than intended because the headline valuation looked attractive. A senior engineer can accept an equity grant that sounds generous in shares but turns out to be a tiny slice once the full cap table is considered. In both cases, the hard part isn't arithmetic. It's translating the math into a decision.

An equity dilution calculator helps because it turns abstract financing language into something testable. Instead of asking, “Is this a good deal?” in the abstract, you can ask better questions. What happens to founder ownership if the option pool is expanded before the round closes? What happens to a candidate's option grant if there are more shares outstanding than the company first mentioned? What changes if a SAFE converts on more favorable terms for the investor?

That's where clarity starts. Not with a perfect forecast, because startup finance never gives you that, but with a model you can stress-test before you sign anything.

A first-time founder usually sees the same sequence. The investor says the valuation is strong. Counsel marks up the docs. Everyone moves fast. Then one line in the model changes, and suddenly the founder's ownership doesn't look like the number they had in mind.

A senior engineer has a parallel version of that moment. The company says the role includes meaningful equity. The offer letter lists a number of options. It sounds substantial until the candidate asks, “Out of how many total shares?” That's the point where excitement turns into fog.

The founder is trying to answer questions like these:

The candidate is usually asking a different set of questions:

Practical rule: If you can't explain the offer or the term sheet in plain English, you shouldn't sign it yet.

An equity dilution calculator gives both people the same advantage. It replaces vague reassurance with a model. You enter the cap table, round terms, option pool assumptions, and convertible instruments. Then you see the ownership outcome instead of guessing at it.

Founders often focus on valuation because it's the visible negotiating point. Candidates often focus on the number of options because it's the visible compensation point. But ownership economics usually hide in the mechanics around those numbers.

That's why a calculator is less like an accounting tool and more like a flashlight. It shows what's sitting in the corners of the deal. Once you can see it, the negotiation changes. You stop reacting to labels and start working from outcomes.

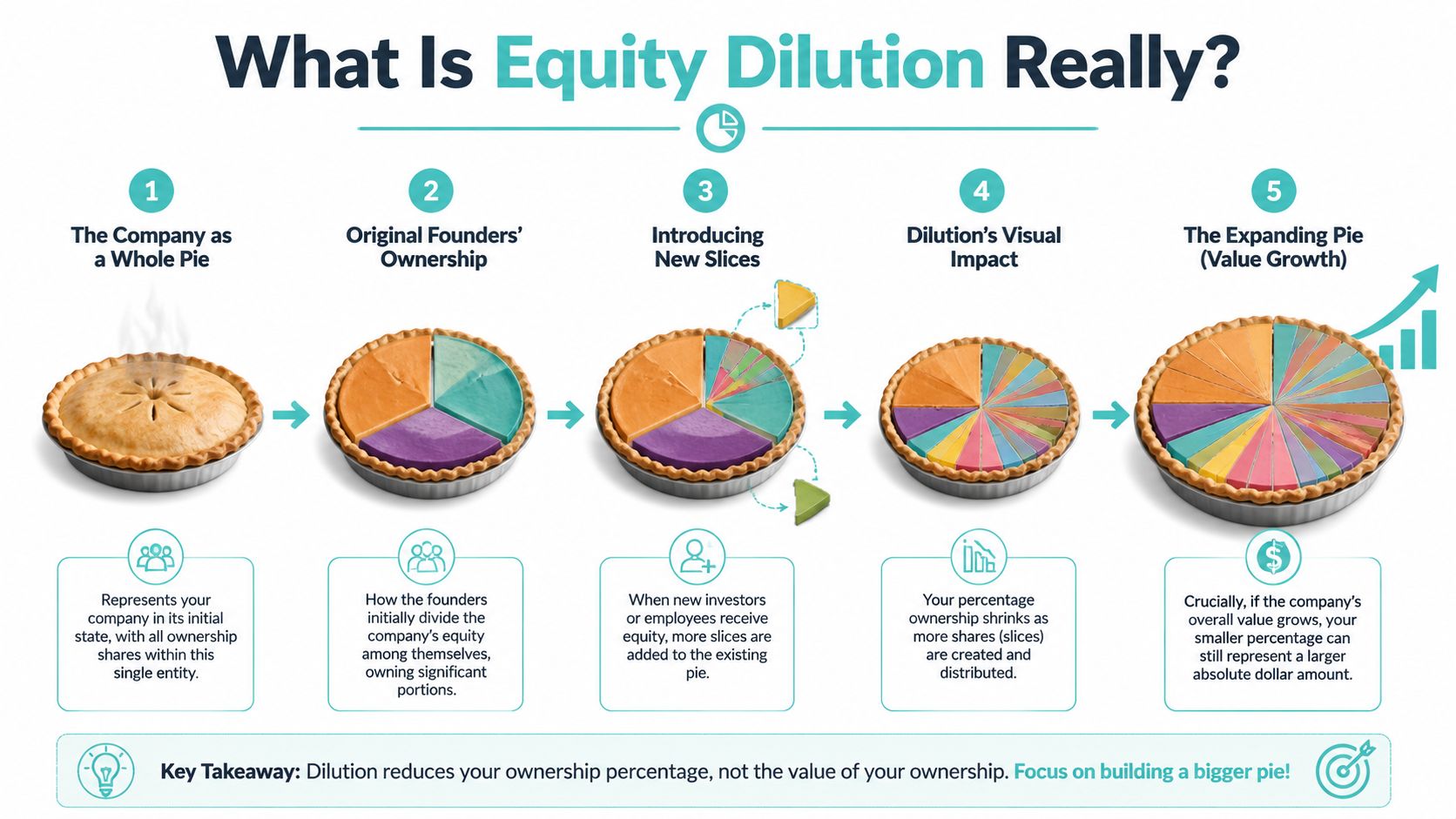

The easiest way to understand dilution is to stop thinking about legal documents and start thinking about pie.

At the beginning, the company is one whole pie. The founders divide it into slices. If they're the only owners, those slices add up to the entire pie. Then the company raises money, grants options, or converts SAFEs and notes. New slices get created. The pie now has more slices than before, so each original slice becomes a smaller percentage of the whole.

That sounds bad until you remember the point of the exercise. If the pie becomes much larger in value, a smaller percentage can still be worth more in absolute terms.

A lot of unnecessary fear comes from treating dilution as failure. It isn't. Startups issue equity because they need to hire people, reward early employees, and bring in capital to grow. If nobody ever got diluted, most venture-backed companies wouldn't get far.

What matters is whether the dilution is intentional, proportional, and well understood.

Here's the mental model I use with founders and candidates:

| Situation | What changes | What stays the same |

|---|---|---|

| New investor buys into the company | Total shares increase | Your existing share count usually stays the same |

| Option pool expands | Reserved shares increase | Your percentage falls if the denominator grows |

| SAFE or note converts | New shares are issued to convert the instrument | Ownership shifts before or during the priced round |

Equity dilution is “the reduction in an owner's percentage stake that occurs specifically when a company issues additional shares to investors during fundraising rounds, grants employee stock options, or converts convertible debt instruments like SAFEs and notes,” according to SVB's explanation of startup equity dilution.

That formal definition matters because it tells you what to watch. Dilution doesn't happen because your business changed direction or because revenue slowed. It happens when the cap table changes through new equity issuance.

The right question isn't whether dilution will happen. It's whether the value created by the new shares justifies the ownership you gave up.

Founders sometimes fixate on the percentage drop and miss the strategic upside. Candidates sometimes do the reverse and hear “you'll be diluted later” as if that automatically wipes out the opportunity. Neither view is useful on its own.

You need both lenses. Percentage tells you control and relative ownership. Value tells you what that ownership could represent if the company executes.

If you want a practical breakdown of how founder control can stay central even after major financing events, The Business Model Analyst Deepseek report is worth reading. It's a useful reminder that dilution and control aren't always the same conversation.

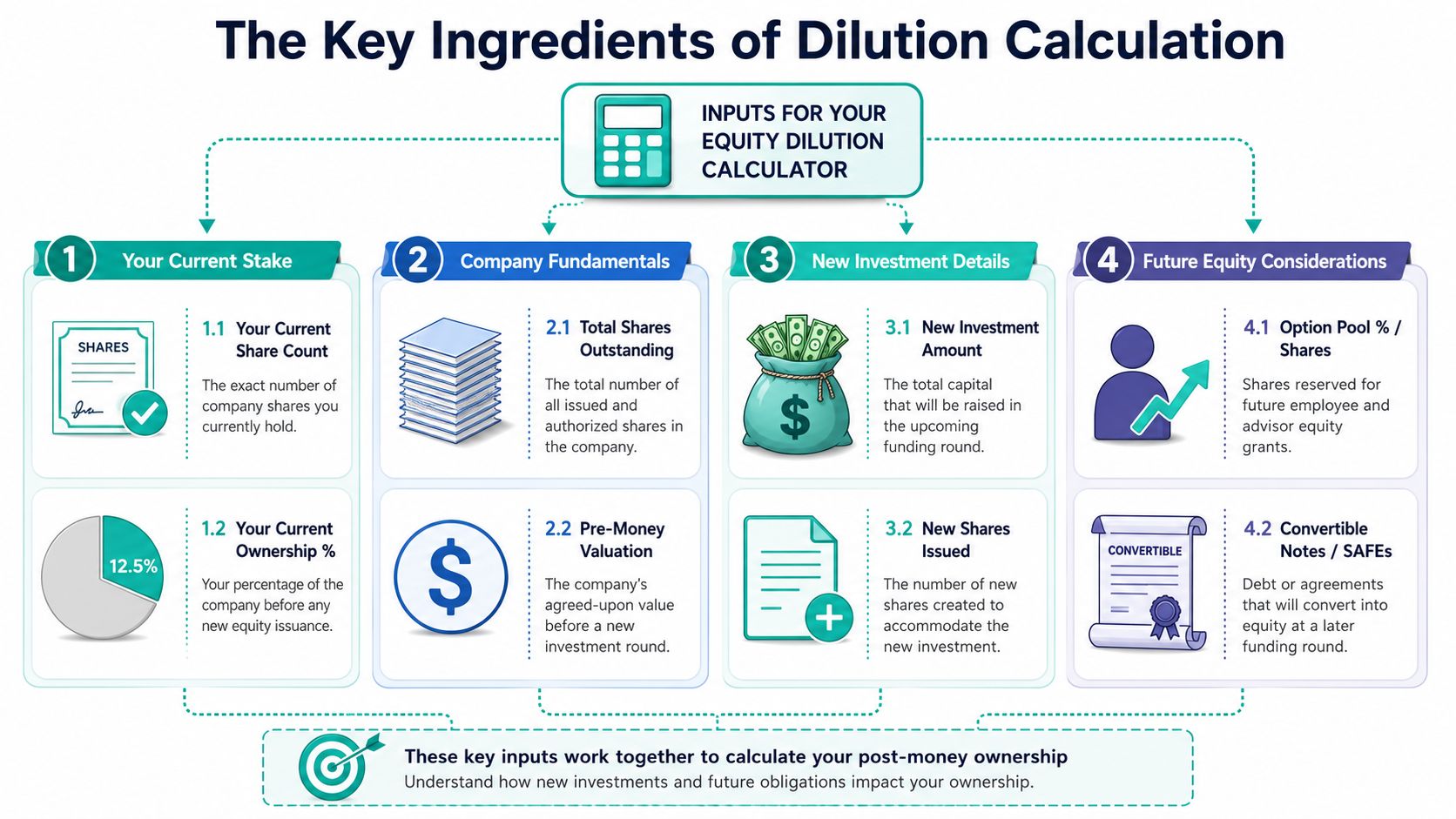

A dilution calculator only works if the cap table inputs reflect reality. I see the same mistake from both sides of the table. Founders model the round off a rough share count from memory, and candidates evaluate an offer off the headline option grant without asking what that grant sits on top of.

Pre-money valuation is the company's value before the new cash comes in. Post-money valuation is the pre-money valuation plus the new investment.

Simple definitions, but the confusion shows up fast in negotiations. A founder may hear a strong valuation and assume the dilution is modest. A candidate may hear the latest valuation and assume their grant is worth more than it is. Neither conclusion holds unless you also know the share count and how many new shares will be issued.

Use these inputs together:

For founders, this helps test whether a valuation headline protects ownership. For candidates, it helps separate company value from grant value, which are not the same thing.

Start with the fully diluted share count. That includes founder stock, issued employee equity, the available option pool, and securities that are likely to convert into equity. Using only outstanding common shares gives a cleaner-looking answer and the wrong one.

The basic math is straightforward. If an investor is buying a target ownership percentage, the company issues enough new shares so that the investor ends up with that percentage of the post-round total. Carta's dilution explainer walks through the mechanics and why the denominator matters so much.

That denominator is where negotiations often turn. Founders use it to compare term sheets that may look similar on valuation but differ once pool increases or convertibles are included. Candidates use it to translate a grant like "50,000 options" into an actual ownership percentage, which is the only number that lets you compare one offer against another.

The option pool is reserved equity for future hires and advisors. It changes dilution even before a single new employee joins.

This is one of the most common traps in an early round. If investors ask for a larger pool to be created before closing, existing holders usually absorb that dilution first. Founders should model the pool expansion separately from investor ownership so they can see who is bearing what. Candidates should ask two direct questions: how large is the current pool, and is the company expecting to increase it in the next financing?

Those questions matter because a grant can look generous in raw share terms but sit inside a cap table that is about to expand. If you are assessing the economics of your own offer, the vesting timeline matters too. This guide to startup vesting schedules is a useful companion to the dilution math.

SAFEs and convertible notes are where a simple model stops being enough. They are not common stock on day one, but they often turn into shares right before or as part of a priced round, which changes the fully diluted count and the ownership percentages everyone cares about.

The key conversion rule is practical. SAFE holders usually convert at the better of the valuation cap price or the discount price. Y Combinator's SAFE primer explains how those terms work in the standard documents. For founders, that means a SAFE round that felt founder-friendly when signed can produce more dilution than expected when the priced round finally happens. For candidates, it means the option grant you are evaluating may represent a smaller slice of the company than the current common share count suggests.

One direct rule of thumb helps here. If the company has raised meaningful SAFE or note financing, do not accept back-of-the-envelope dilution math from anyone. Model the conversion terms, then negotiate off the modeled cap table.

A dilution calculator earns its keep when it answers a real question.

A founder is about to raise a seed round and wants to know how much of the company will still be theirs after the investor comes in and the hiring pool gets topped up. A senior engineer has an offer with a promising option grant and wants to know what that grant is likely to be worth after the next financing. Same math. Different decisions.

Start with the plain version of the cap table. Founders own all the outstanding shares. The company is raising its first priced round. The investor wants a meaningful stake, and the board wants an option pool large enough to hire the next wave of employees.

That sounds simple. It rarely feels simple once the percentages move.

Before the round, the picture is straightforward:

| Holder | Before round |

|---|---|

| Founders | Entire company |

| Employees option pool | Small or not yet expanded |

| New investor | None |

After the round, the company has issued new shares to the investor, and it may also have increased the option pool:

| Holder | After round |

|---|---|

| Founders | Lower percentage ownership |

| Employees option pool | Larger reserved pool for future hires |

| New investor | Ownership from newly issued shares |

The practical mistake on the founder side is focusing only on the investor check. If the term sheet says the company must create or increase the option pool before the round closes, founders usually absorb that dilution first. Investor ownership then gets calculated on top of the larger share count. In plain English, the pool can cost founders almost as much attention as the financing itself.

Candidates should read the same scenario differently. An option grant is not just a share number. It is a claim on a percentage that can shrink as the cap table expands. If a company says, "we have plenty of room left in the pool," ask the next question: was that pool already sized for the next 12 to 18 months of hiring, or will it likely be increased again at the next round?

One useful way to model this scenario is to run two versions side by side:

Those are not academic differences. They change who bears the dilution.

For founders, that comparison becomes a negotiation tool. For candidates, it helps separate a solid offer from one that only looks generous because nobody has translated the future cap table.

Now add the parts that trip people up. The company raised on SAFEs earlier. Those SAFEs convert in the Series A. The board also wants to refresh the option pool. A new lead investor is pricing the round.

At that point, order matters more than optimism.

This Carta guide to dilution is useful because it frames dilution through cap table mechanics rather than headline valuation alone. That is the right lens for a Series A model. The negotiation usually turns on who gets diluted by the SAFE conversion, who gets diluted by the pool refresh, and whether the pre-money number is being discussed on a basis that already includes those shares.

The sequence should be explicit:

Founders should care about this sequence because each step changes the denominator used in the next one. A round can look founder-friendly at the valuation headline and still leave founders with less ownership than expected once the convertibles and pool increase are included.

Candidates should care because the same sequence tells you whether your grant sits behind hidden dilution. If earlier SAFEs have not yet converted, the current cap table may understate the actual fully diluted share count. If the pool is about to be refreshed, your percentage ownership can shrink soon after you join, even if your option count stays fixed.

That is why one question works so well in negotiations: "Can you show me the fully diluted cap table before and after the round, including convertibles and the option pool?" A founder who can answer it usually understands the trade-offs. A candidate who asks it usually gets a much clearer picture of the offer.

A good scenario model does more than output a percentage. It shows where dilution is coming from.

For founders, that means separating investor dilution from pool dilution and conversion dilution. Those are different economic concessions, and they should be negotiated that way.

For candidates, it means translating an option grant into context. The right question is not only how many shares you are getting. The right question is what financing events are likely to hit that percentage before you vest enough of the grant for it to matter.

Cap table mistakes usually start with skipped steps, not advanced math. The cleanest way to avoid them is to model each financing event in order, then use the result as a negotiation document instead of a rough estimate.

A founder gets a term sheet on Friday and wants to know what the round does to ownership before Monday's call. A senior engineer gets an offer letter with an option grant and wants to know whether the percentage in the recruiter's spreadsheet survives the next financing. Both need the same thing. A simple model they can trust.

Good dilution calculators are decision tools, not finance theater. The sheet should be simple enough to use in a live negotiation and detailed enough to catch the terms that change ownership.

If you want a reference point for structure, this startup equity calculator guide is a useful companion to a downloadable model.

The best version starts with a small number of inputs that map to real cap table decisions:

That is enough to answer the practical questions.

For founders, the calculator helps compare structures, not just valuations. A higher pre-money can still be a worse deal if the pool expansion lands entirely on the common holders. For candidates, the same sheet turns an option grant into something you can evaluate against likely financing events instead of a headline number in an offer email.

Keep the spreadsheet to three tabs:

| Tab | Purpose |

|---|---|

| Current cap table | Shows ownership before any new financing |

| Next round model | Calculates dilution from the term sheet you are discussing |

| Sensitivity cases | Tests a few realistic variations, such as pool expansion or convertible conversion |

That layout keeps the logic visible. It also makes version control easier, which matters more than people expect. Many cap table errors come from changing one assumption in place and forgetting what moved.

Start with the live deal in front of you. Then copy the tab and change one variable at a time.

Founders should test the terms that usually move dilution the most: valuation, pool size, and whether convertibles convert before the priced round. Candidates should ask for enough context to fill in the same model, even if only approximately. Number of fully diluted shares, size of the option pool, and whether the company expects to raise soon are often enough to make the grant legible.

One warning from practice: a calculator is only as useful as the assumptions inside it. If a company says your grant is 0.25% but cannot tell you whether that figure is based on issued shares or fully diluted shares, the spreadsheet is not the problem. The offer is still unclear.

Use the model as a negotiation document. Founders can use it to push for cleaner round structure. Candidates can use it to ask better questions and judge whether an offer still works after expected dilution.

A founder opens the spreadsheet and sees their ownership drop from 62% to 41%. A senior engineer looks at an offer that says 0.25% and wonders what that number will be worth after the next round. The calculator did its job. Now the hard part starts.

The right question is not whether dilution happened. It always does. The core question is whether the post-round cap table still supports the next two or three decisions the company needs to make: hire well, raise again, and keep the people building the company motivated.

Start by reading the output as a future cap table, not a closing-day snapshot. I tell founders to look at what the business will feel like after the round, after the pool increase, and after any SAFEs or notes convert. A round can look acceptable on paper and still leave the company too tight on hiring equity or too thin on founder ownership for the next financing.

A simple priced-round example shows why. If a company raises $5 million on a $10 million pre-money valuation, the new investor ends up with one-third of the company post-money. That dilution may be perfectly reasonable if the capital meaningfully extends runway and helps the company hit the milestones for the next round. It becomes expensive when the company raises more than it needs, expands the option pool fully before closing, and leaves conversion mechanics fuzzy.

That is where founders usually have room to negotiate.

Bring scenarios into the meeting. One base case, one investor-friendly case, one founder-protective case. That changes the discussion from abstract opinions to explicit trade-offs.

Negotiation cue: Ask, "Which structure gives us enough capital to execute without forcing a painful pool expansion or a weak Series B setup six months from now?"

Candidates should read the results differently. You are not trying to perfect the company model. You are trying to test whether the company is transparent and whether the grant still makes sense after expected dilution.

Start with percentage, then ask what sits underneath it. An option grant is a slice of a pie that will almost certainly be cut into more pieces later. The grant can still be attractive. But only if you know roughly how large the pie is today and how likely it is to expand soon.

Ask these questions directly:

The answers matter as much as the grant size. A company that explains the cap table clearly is giving you useful information about how it operates. A company that avoids basic ownership questions is also telling you something.

A few patterns deserve caution:

For the actual compensation conversation, this stock option negotiation guide for startup candidates is practical and specific.

The best calculator output gives both sides a clearer bargaining position.

Founders want enough capital, enough hiring room, and enough retained ownership to keep the company financeable. Candidates want enough upside, enough clarity, and enough evidence that the company treats equity as a real part of compensation rather than a vague promise.

Those are different goals, but the same model helps both sides test them. That is what makes dilution math useful. It is not just valuation arithmetic. It is a negotiation playbook.