You're probably on one side of the same awkward conversation.

If you're a founder, you're trying to answer questions about ownership without sounding evasive, while also keeping your financing math straight. If you're a senior engineer or product hire, you're staring at an offer that includes equity and wondering whether the percentage on paper means what you think it means.

Both of you are talking about the same document. The startup cap table.

A good startup cap table makes fundraising cleaner, hiring conversations more honest, and decision-making much less emotional. A bad one creates confusion fast. Founders overestimate how much they still own. Candidates overestimate what their grant is worth. Investors spot the mismatch immediately.

The cap table is where ownership stops being a story and becomes math.

For a founder, that means it answers practical questions like: who owns common stock, what's reserved for hiring, what converts later, and what happens to everyone's stake after the next round. For a candidate, it answers a different but equally important question: what does my equity buy me, and how might that change after financing?

Founders usually learn cap tables under pressure. They're setting up a Delaware C-corp, issuing founder shares, carving out an option pool, then taking SAFEs or a seed round while still trying to hire. The spreadsheet grows faster than their understanding.

Candidates hit the same document from the opposite direction. They hear phrases like “fully diluted,” “post-money,” and “option pool” in an offer discussion, but they're missing the context behind those terms. That's how a seemingly generous grant becomes hard to evaluate.

Practical rule: If a founder can't explain the cap table clearly to a key hire, the company probably doesn't understand its own dilution well enough yet.

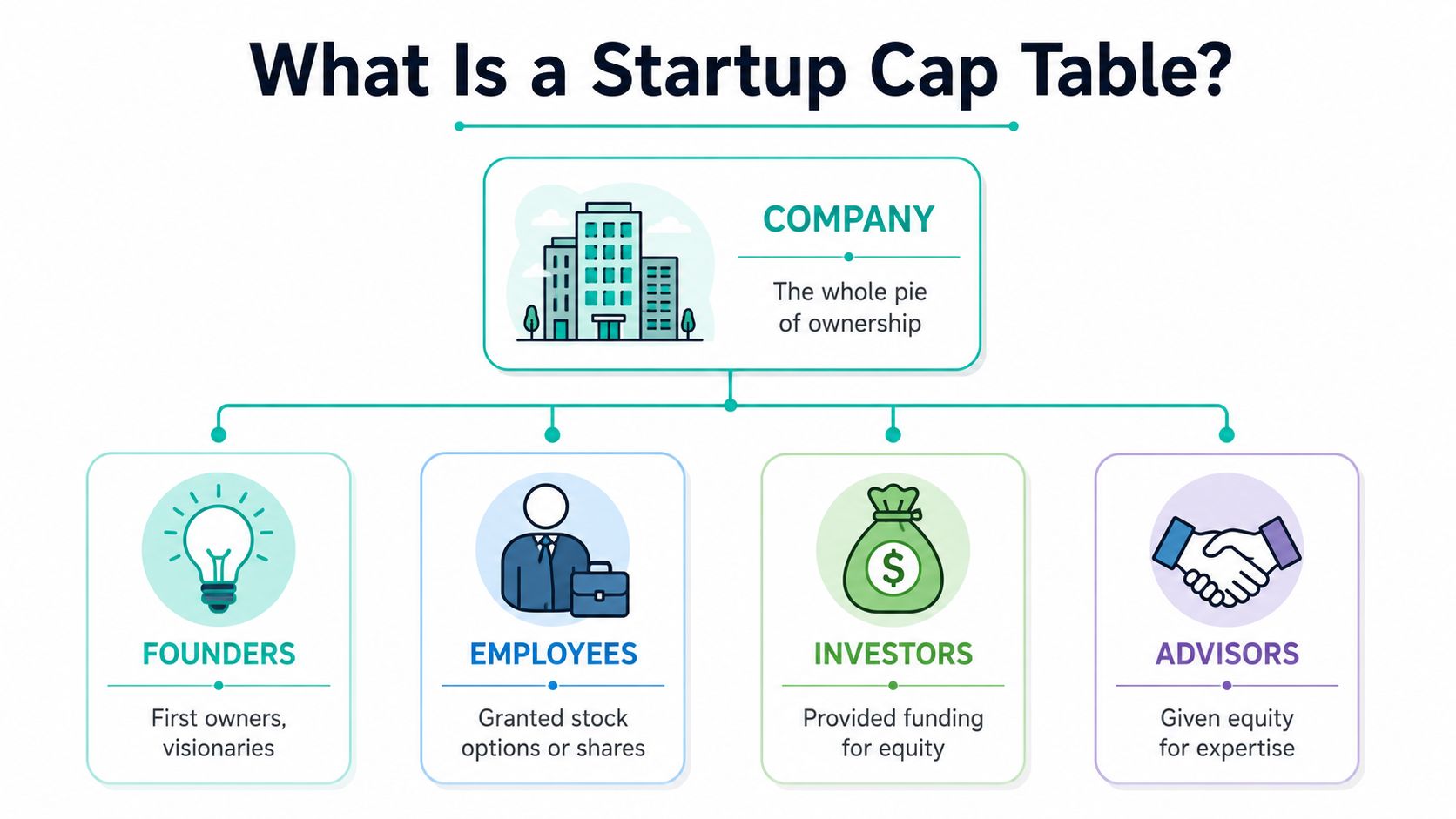

A useful startup cap table does more than list names. It has to work for three audiences at once:

When people say the cap table is the “single source of truth,” they mean it should be the working record everyone can rely on when a grant is made, a round closes, or a company exits.

That's why the details matter. Not because spreadsheets are exciting, but because equity is one of the biggest promises a startup makes.

A founder is hiring a senior engineer and says, "We can offer 0.5%." The engineer asks, "0.5% of what, exactly?" If the company cannot answer that from its cap table, the conversation is already off track.

A startup cap table is the company's ownership record. It shows who owns equity, what form that equity takes, and what the ownership looks like before and after new grants, SAFEs, notes, or priced rounds. For founders, it is an operating document. For candidates, it is the only way to translate an equity offer into something real.

This is the first place founders and hires often talk past each other.

Authorized shares are the maximum shares the company is allowed to issue under its charter. Issued shares are the shares granted to founders, employees, investors, or other holders. A company can authorize a large number and still have only a fraction of those shares outstanding.

That distinction matters because share count alone tells you very little. A grant of 100,000 shares can be large or small depending on the denominator. Candidates often focus on the numerator. Founders need to explain the denominator.

Early-stage companies usually start with a share count that leaves room for founder stock, an option pool, and future financings without constant charter changes. That makes administration easier and keeps equity math cleaner in board approvals, grant documents, and financing models.

It does not make the company more valuable.

What matters is the ownership percentage tied to those shares, and whether that percentage is being measured on an issued basis or a fully diluted basis. That is one of the biggest translation gaps between founder-side cap table management and candidate-side offer evaluation.

A cap table answers ownership questions. It does not answer valuation questions by itself.

A usable cap table should show, at minimum:

For founders, that is the baseline needed to approve grants, model fundraising, and avoid ugly surprises in diligence. For candidates, it is how you tell the difference between "you have 0.5%" and "you may have something closer to 0.3% once the pool expansion and SAFE conversion hit."

A clean cap table does not remove dilution or negotiation. It makes both visible.

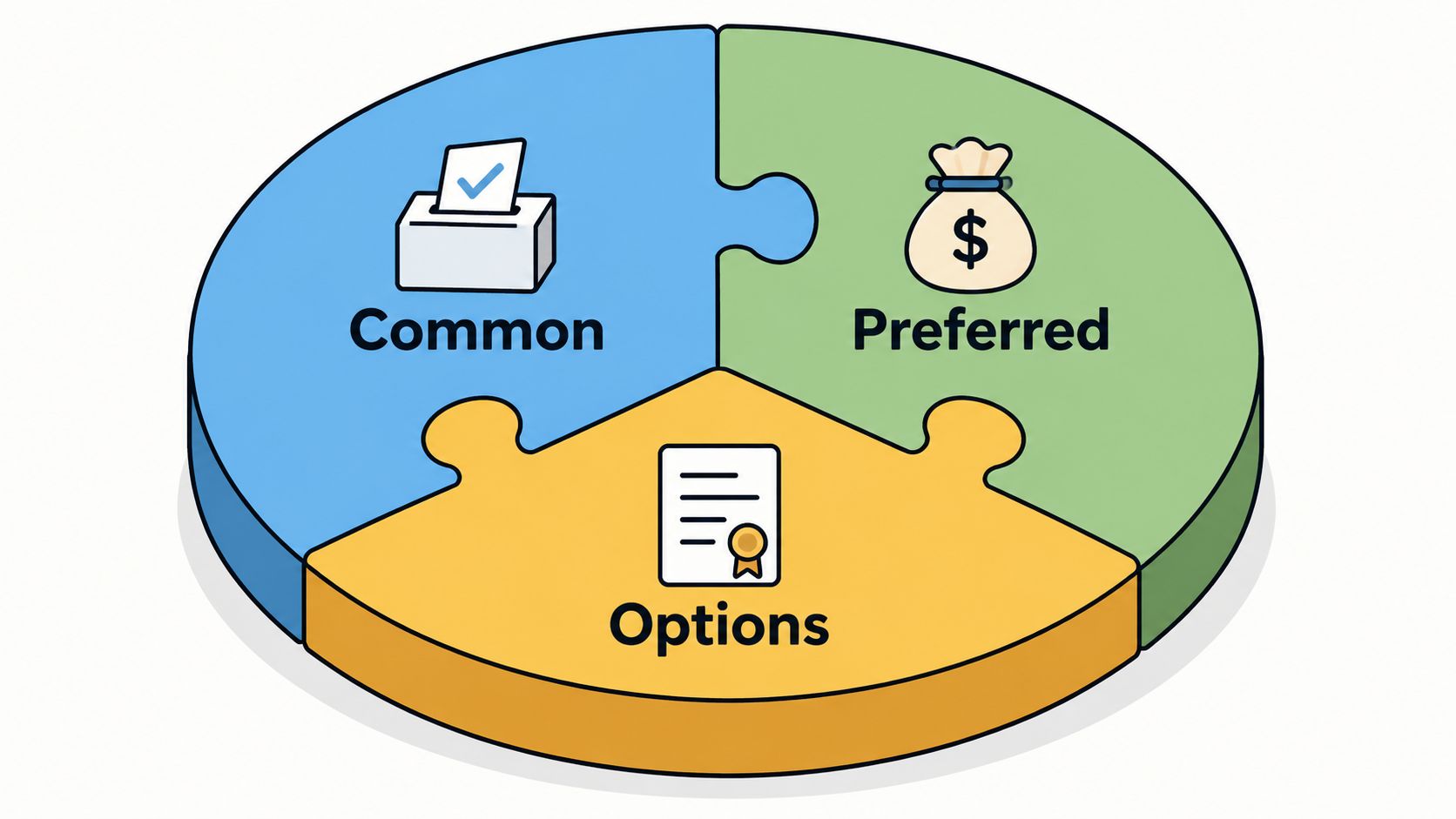

Once you open a real cap table, you'll see that not every line means the same thing. Some entries are actual shares issued today. Others are rights to receive shares later. Some belong to founders and employees. Others belong to investors with different economics.

Common stock is usually what founders receive at formation and what employees ultimately receive through stock options or direct grants. It's the standard ownership layer generally recognized when considering startup equity.

Preferred stock is usually what investors buy in priced rounds. It sits separately because investors often negotiate rights that common holders don't have. Even if you're not modeling every legal term in your working spreadsheet, you still need to track the class correctly.

For a candidate, the takeaway is simple: your equity may not sit in the same position as investor equity. That doesn't make it bad. It just means not all ownership is economically identical.

The option pool is the block of equity reserved for future hires. This is one of the most important founder-side planning tools because it determines how much room the company has to recruit without reworking ownership every time.

For employees and candidates, the option pool matters because your grant usually comes out of it. If the company has barely any unallocated options left, future hiring can create pressure to expand the pool and dilute existing holders.

Many startup cap tables go wrong at this point.

The company can't treat SAFEs and convertible notes as if they don't exist until the day they convert. As Stripe's guide to startup cap tables explains, the cap table must separately track convertible instruments like SAFEs and notes until they convert into equity, documenting the principal amount, discount rate, and valuation cap that determine how many shares the instrument will eventually convert into. It must also include the option pool, the number of share options ringfenced for future employee incentives.

That separate tracking matters for both sides of the table.

A strong cap table line item should answer these questions quickly:

| Item | What you should be able to tell |

|---|---|

| Founder shares | Who holds them, when they were issued, and whether vesting applies |

| Investor equity | Which class it belongs to and how many shares were issued |

| Employee grants | Granted amount, exercised status if applicable, and source from the option pool |

| SAFEs or notes | Conversion terms and how they may affect future ownership |

If a founder has to explain ownership from memory instead of from records, the startup cap table isn't doing its job.

A founder closes a round and feels relieved. A staff engineer reads their option grant and asks the harder question: what happens to my percentage after the next financing?

That gap shows up in almost every startup. Founders usually talk about valuation, runway, and who came into the round. Candidates care about what their equity could be worth, and how fast that percentage can shrink. The cap table puts both sides on the same math.

Dilution happens when the company issues more shares. Existing holders usually keep the same number of shares, but those shares represent a smaller percentage of the business because the total share count increased.

That distinction matters.

A founder can say, truthfully, that no one "lost" shares in the round. A candidate can say, also truthfully, that their ownership went down. Both statements describe the same event from different sides of the cap table.

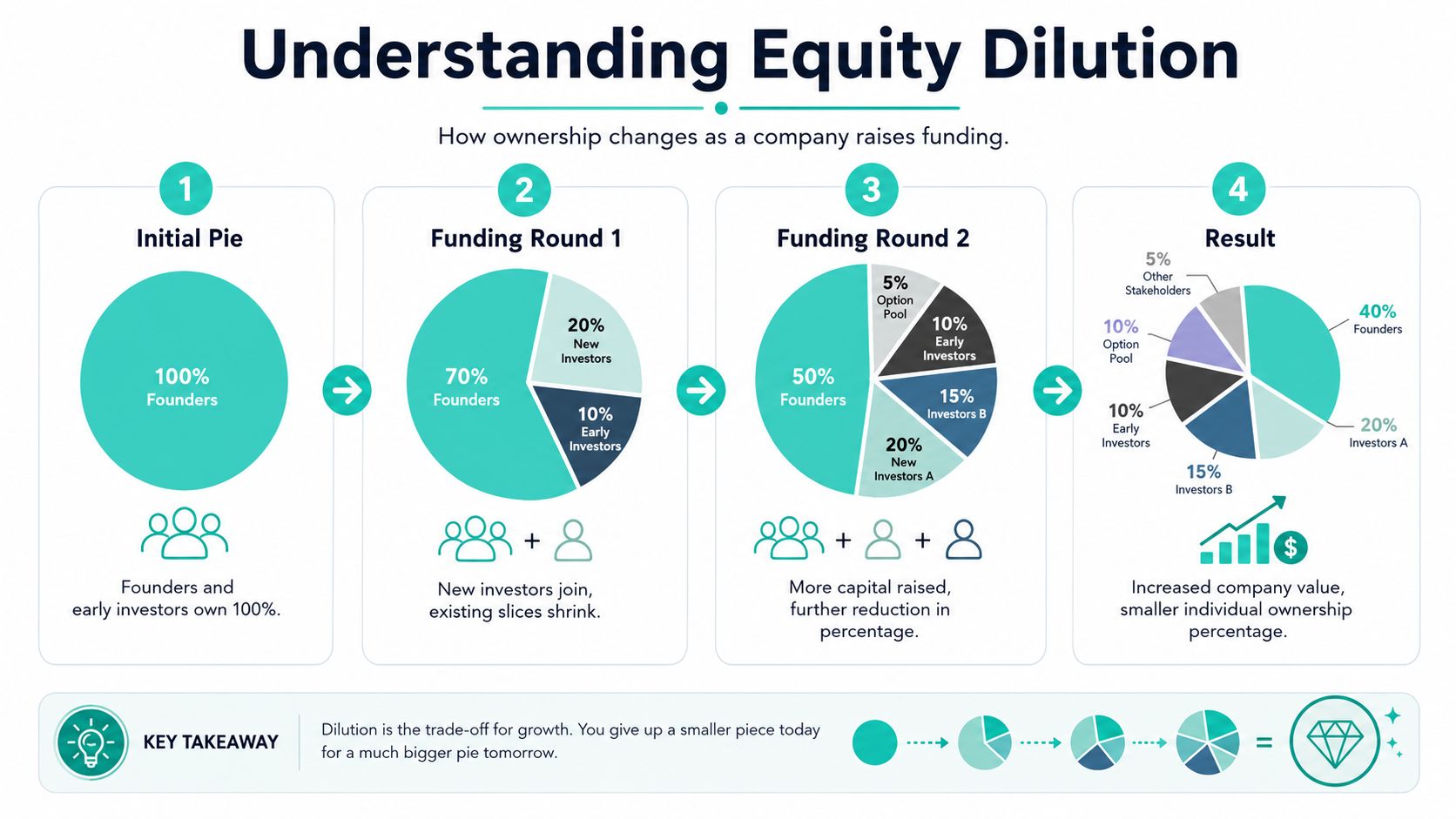

Start with a company that has 10,000,000 shares outstanding on a fully diluted basis. Suppose a founder owns 5,000,000 shares, the co-founder owns 3,000,000, and the remaining 2,000,000 sit with employees and the option pool.

Now the company raises a priced round and issues 2,500,000 new shares to investors.

After that financing, the old holders still own their original share counts. But the company now has 12,500,000 shares outstanding. The founder who owned 50% before the round now owns 40%. Someone with 1% before the round now owns 0.8%, assuming no other changes.

This is the part many offer conversations skip. Share count stayed flat. Ownership percentage did not.

For founders, dilution is the price of bringing in capital, and often the right trade if the money extends runway or helps the company grow faster than the ownership loss hurts.

For employees, dilution is part of the compensation math. A grant that sounds large in isolation may look very different after a financing, an option pool expansion, or the conversion of SAFEs and notes. That is why candidates should ask what percentage the grant represents today, whether that number is calculated on a fully diluted basis, and what assumptions management is using about the next round.

A good founder should be ready to answer those questions plainly.

Many first-time founders focus only on investor ownership. In practice, the option pool is often the bigger point of confusion in hiring conversations.

If investors ask the company to increase the option pool before closing a round, that expansion usually dilutes existing holders before the new money even goes in. From the founder side, this is a negotiation point in the term sheet. From the candidate side, it affects whether "we reserve equity for future hires" comes out of a pool that already exists or from a larger pool created right before financing.

That is one reason a headline valuation never tells the full story.

SAFEs and notes can delay dilution, but they do not remove it. They postpone the exact share count until the conversion mechanics are set by the next financing.

That is why founders should explain current ownership and likely future ownership separately. Candidates do not need every legal detail, but they do need to understand whether a stack of convertibles could materially change the denominator later. Founder Connects' guide to funding is useful background if you want to compare notes, SAFEs, and priced equity from the financing side.

The useful version of this conversation is specific. It sounds like: here is your grant size, here is what percent it represents on a fully diluted basis today, here are the major instruments that could change that, and here is the kind of dilution we would expect if we raise another round.

That helps both sides. Founders build credibility. Candidates can judge the offer on actual economics instead of optimistic shorthand.

If you are evaluating an offer, use an equity calculator for startup offers and pressure-test the assumptions. If you are making the offer, bring those assumptions to the table before the candidate asks.

Your first startup cap table doesn't need fancy software. It needs discipline.

A spreadsheet is enough at the beginning if the company is early, the ownership is still simple, and someone is updating it immediately after each board-approved event. The mistake isn't starting in a spreadsheet. The mistake is letting the spreadsheet drift away from the legal documents.

A simple operating version should include the basics:

That's your starting layer. It's not enough for diligence, but it's enough to prevent chaos.

A cap table that's easy to use internally can still fail in fundraising if it doesn't show the whole picture. According to Bulletpitch's guide to a VC-friendly cap table, a due-diligence-ready cap table should include five distinct sections: current ownership, fully diluted ownership summary, a separate convertibles schedule, detailed option pool status showing granted versus unallocated, and a pro forma model for the next financing round.

That structure matters because investors don't want to reverse-engineer your ownership.

Here's a stripped-down example of how a current ownership section might look.

| Shareholder | Share Class | Number of Shares | Ownership % |

|---|---|---|---|

| Founder A | Common | 4,000,000 | 40% |

| Founder B | Common | 4,000,000 | 40% |

| Employee Option Pool | Options | 1,000,000 | 10% |

| Seed Investors | Preferred | 1,000,000 | 10% |

This kind of summary is useful, but it's only one section. You still need a separate place for unconverted SAFEs and notes, and you need a forward-looking model before the next round starts.

What works:

What doesn't work:

Founders also need to tie equity grants to vesting terms consistently. If you're working through how those schedules are usually structured, this guide to an equity vesting schedule is a good companion to the cap table itself.

A founding team offers a senior engineer 0.5% and feels good about it. The candidate hears 0.5% and tries to translate that into upside, dilution risk, and how serious the company is about equity. If the founder cannot explain the denominator, the option pool, and what happens in the next round, the offer loses credibility fast.

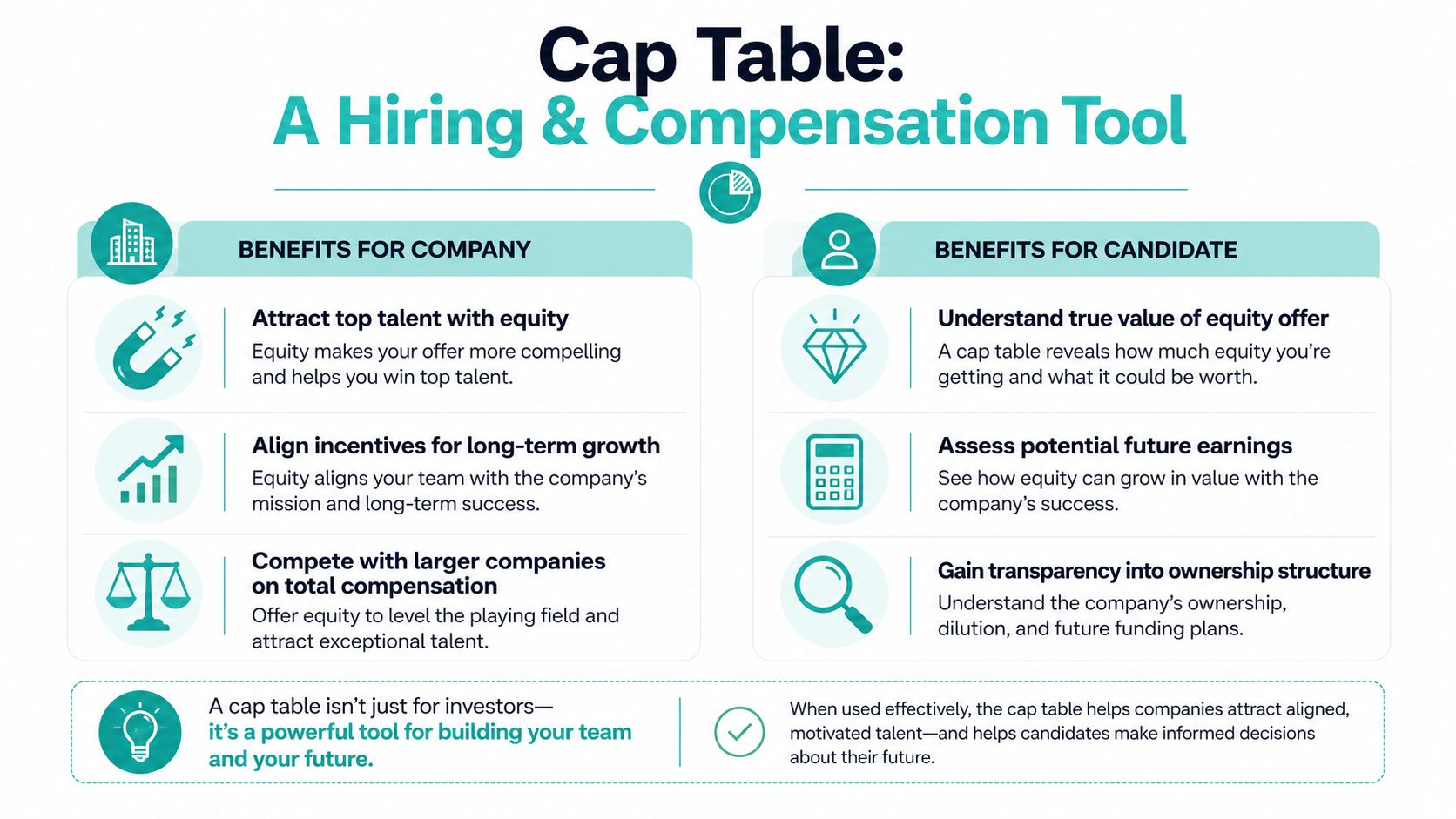

A cap table is not only a financing document. It is also the working document behind hiring, leveling, and equity compensation. Founders use it to decide what they can grant without creating hiring problems later. Candidates use it to judge whether an offer is meaningful or just loosely worded startup math.

That gap matters. Founders often speak in grant sizes. Good candidates evaluate ownership, dilution, vesting, and exercise risk.

Strong candidates do not expect guarantees. They expect a clean explanation.

The companies that handle equity well can answer basic questions in plain language. How many shares are outstanding on a fully diluted basis? Is the grant coming from the existing pool? Is a pool increase likely before or during the next financing? What other instruments could convert into shares later? Those answers tell a candidate whether the team manages equity or just delegates it and hopes for the best.

Clear communication helps on both sides:

Compensation design also has to fit the role. Equity is only one part of the package. Teams building quota, bonus, and incentive plans can compare their approach with this revenue operating system playbook.

Candidates usually hear a headline percentage. What they need is context behind it.

A statement like “we're offering 1%” can mean several different things. It might refer to current outstanding shares. It might refer to fully diluted shares. It might ignore SAFEs or notes that will convert later. It might also ignore a likely option pool increase tied to the next round. Each version produces a different economic outcome.

This is the founder-to-candidate translation problem. Founders often describe intent. Candidates need the cap table mechanics.

A better way to present an offer is simple: state the number of options, the current fully diluted share count, the implied percentage today, and the main events that could change that percentage. That does not remove uncertainty. It makes the uncertainty legible.

Ask whether the quoted ownership is based on today's fully diluted cap table or on a pro forma model after the next financing. Those are different numbers.

A candidate does not need to model a Series A from scratch. They do need enough detail to understand what they are signing.

Founders should welcome these questions. Candidates who ask them are usually the same people who understand risk, think like owners, and care about how the company is run.

Candidates who want the mechanics behind grant size, strike price, exercise timing, and tax trade-offs can review this guide to private company stock options.

A founder tells a senior engineer, "We're offering 0.4%." The engineer hears upside. The founder hears dilution, option pool math, and whether that 0.4% still means 0.4% after the next round. Advanced cap table questions usually start there. They are less about definitions and more about what survives contact with hiring, departures, and financing.

Dead equity is stock held by someone who is no longer adding value in proportion to the ownership they kept. Common examples are a co-founder who left early but kept a large stake, an advisor grant that was too generous, or founder shares issued without repurchase rights.

Every stale slice of the cap table reduces flexibility somewhere else. It can make it harder to hire a strong executive, force a larger option pool increase before a financing, or create tension in investor diligence. Candidates should care too. A messy cap table often signals that the company was casual about equity decisions, and that same habit can show up in how offers are explained.

The cleanest way to prevent dead equity is simple. Set founder vesting, keep repurchase rights in place, and review old grants before they become permanent mistakes.

A 409A valuation sets the fair market value of common stock for option pricing. For founders, it is a compliance process that affects how options are granted. For employees and candidates, it affects strike price, which directly changes how expensive it is to exercise.

If a company has not updated its 409A on time or has been granting options off an outdated valuation, that is not a technical foot fault. It can create tax problems, legal exposure, and awkward cleanup work later. Experienced candidates ask about the last 409A date because they understand that an option grant is only as sound as the process behind it.

This is one of the biggest founder-candidate translation gaps. Founders often talk about grant size. Candidates should also ask whether the company has the discipline to issue that grant correctly.

A spreadsheet works for a while. Then one financing closes, a few SAFEs convert, the option pool changes, someone leaves mid-vesting, and nobody is fully sure which version is current.

That is the point where the cap table stops being a record and starts becoming a risk. In practice, the breaking point usually comes before founders expect it. If the company is hiring actively, issuing grants regularly, tracking multiple security types, or preparing for diligence, manual version control becomes expensive.

Some teams also look at newer ownership infrastructure. Companies exploring alternative rails may want to see how teams develop equity tokenization platforms. That is separate from standard venture-backed cap table management, but it reflects a broader shift toward more structured ownership systems.

The standard for any system is straightforward. It should show who owns what today, what is vested versus unvested, what will convert later, and how the next financing changes everyone else's percentage. If it cannot answer those questions quickly and accurately, it is time to upgrade.