You got the offer. The salary looks solid. The team seems sharp. Then you hit the equity section and the confidence drops fast.

You see a big option number, a vesting schedule, a strike price, maybe a mention of the last round, and none of it cleanly answers the only question that matters. What could this be worth to me?

That confusion is normal. Startup equity is often presented in a way that sounds precise but feels unusable. Candidates get a number of options, but not always the denominator. They hear “ownership” without a practical way to estimate it. They're told the upside could be meaningful, but the math behind that upside stays fuzzy.

The good news is that you don't need to become an options theorist to make a smart call. You need a simple framework, a few key data points, and a clear view of the hidden variables that subtly change the outcome, especially dilution, exercise cost, and taxes.

A startup option grant usually lands in front of you as a mix of legal language and optimism. You'll see terms like vesting, exercise price, and expiration, but none of those terms mean much until you translate them into ownership and possible payout.

Start with the practical mindset. Treat the grant like a financial asset with conditions, not like a lottery ticket and not like guaranteed cash. That framing alone improves negotiations because you stop reacting to the raw option count and start asking what those options buy you.

A stock option usually gives you the right to buy shares later at a set price. That set price is the strike price. If the company eventually becomes worth much more, buying at that earlier price can create meaningful upside. If it doesn't, the options may never be worth exercising.

The first mistake candidates make is anchoring on the size of the grant. A large number of options can still represent a tiny slice of the company. A smaller number can be much better if the denominator is smaller, the strike price is lower, or the company's trajectory is stronger.

When I explain startup equity to engineering candidates, I suggest a simple order of operations:

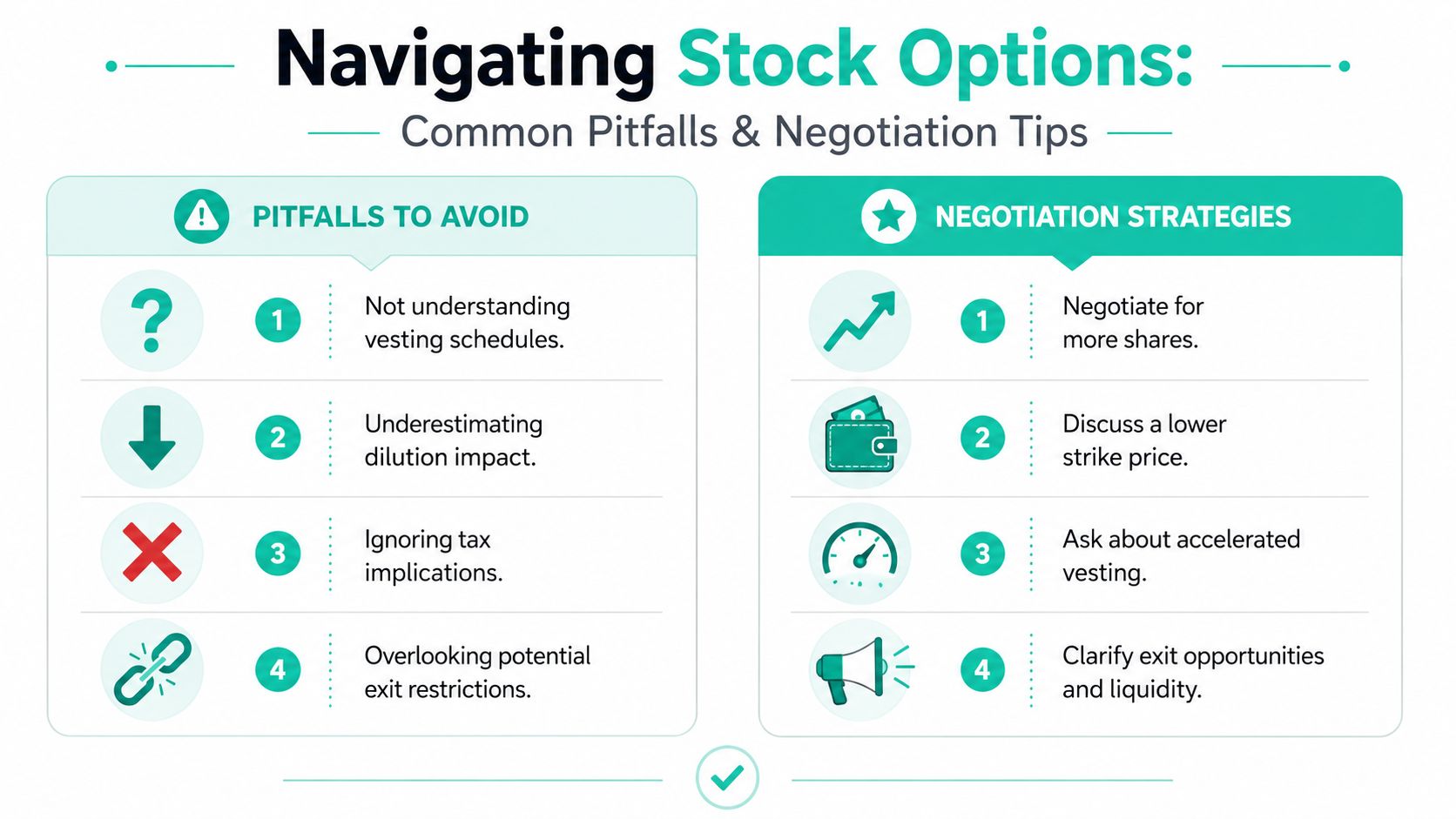

Practical rule: Don't negotiate equity from the option count alone. Negotiate from ownership, cost, and likely exit scenarios.

A strong startup offer can absolutely create wealth. But the real work starts after the offer arrives, when you convert the equity language into a model you can reason about.

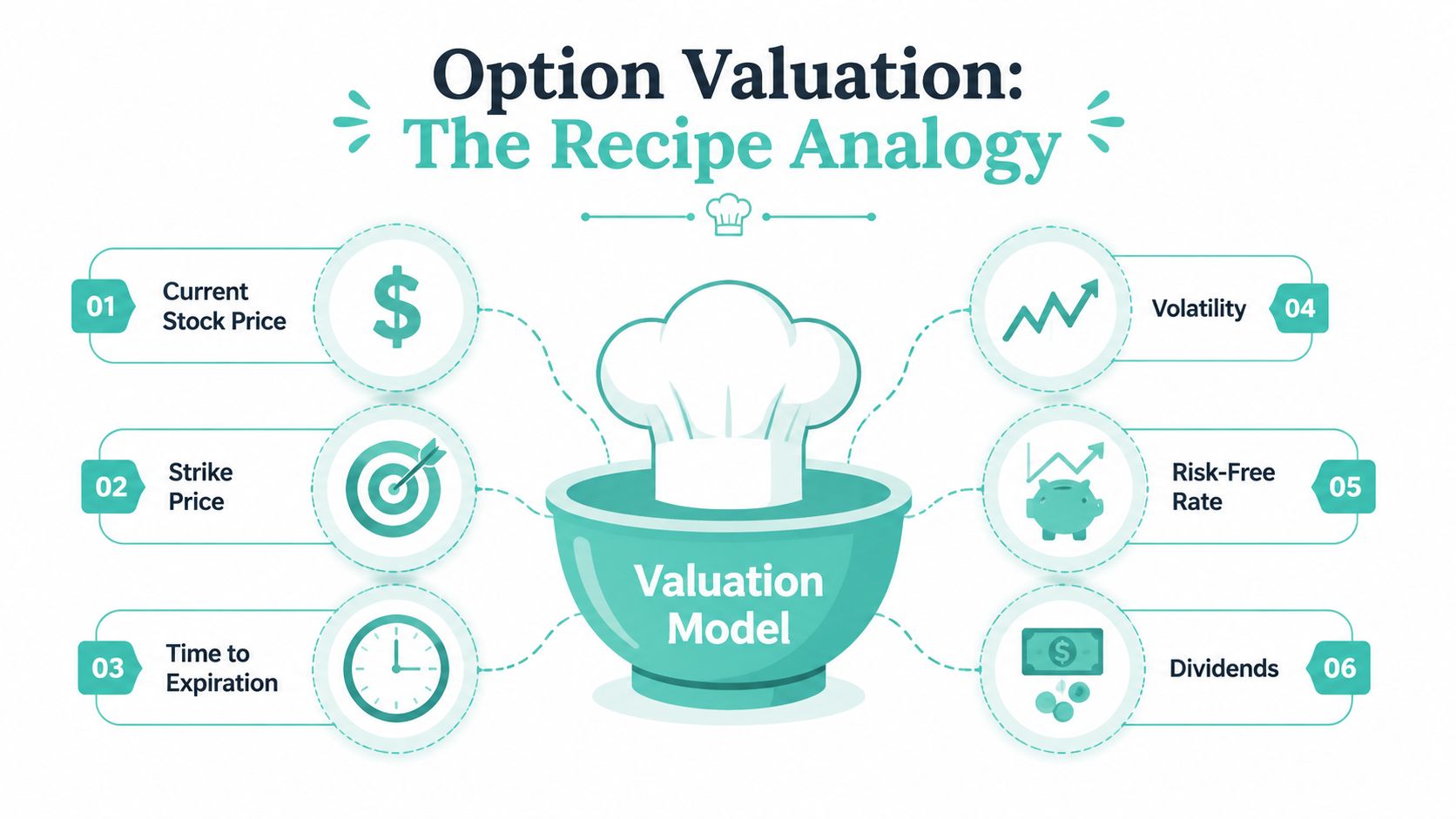

Before you touch a spreadsheet, understand the two pieces that drive option value. According to Merrill's overview of option pricing and valuation, stock option valuation is driven by two components: intrinsic value and extrinsic (time) value. Intrinsic value equals the difference between the underlying stock price and the strike price for in-the-money options, while extrinsic value reflects time until expiration, implied volatility, dividends, and risk-free interest rates.

Intrinsic value is the easy part. If a share is worth more than your strike price, the gap is value you could capture by exercising and selling. If the share value is below the strike price, intrinsic value is zero.

That's why early startup options often feel confusing. A grant can have little or no current intrinsic value and still matter a lot. You're being given the right to buy into a future outcome, not a cash bonus today.

Consider a ticket to a concert from a band that might get huge before the show date. The ticket's current resale value may be modest. Its potential value comes from what might happen before the event.

Time value is where option grants become interesting. More time gives the company more chances to grow, raise capital, launch products, and create a future spread between share value and strike price.

Volatility matters here too. A company with a wider range of possible future outcomes gives the option more potential upside. That doesn't mean the company is safer. It means the option itself can be more valuable because big upside remains possible.

An option can be worth something even when exercising it today would make no sense.

This distinction helps you avoid a common bad conclusion. Candidates sometimes hear that the current common share value is close to the strike price and assume the grant has no value. That skips the whole point of startup equity.

Use this lens instead:

| Component | What it means to you |

|---|---|

| Intrinsic value | What the option would be worth if there were immediate liquidity and the share price exceeded the strike price |

| Time value | What you're being paid for the possibility that the company grows before the option expires |

If you only look at today's spread, you'll undervalue promising grants. If you only look at dream outcomes, you'll overvalue them. Good stock option valuation sits between those two extremes.

Formal stock option valuation models sound intimidating because people lead with the formula. That's the wrong way to learn them. A better way is to think of valuation as a recipe. If the ingredients change, the result changes.

According to NASPP's explanation of ASC 718 inputs, stock option valuation relies on six mandatory inputs required by ASC 718 for option-pricing models: fair market value, exercise price, expected life, expected volatility, risk-free interest rate, and expected dividend yield. The Black-Scholes model is the most widely used closed-form solution for this calculation.

Each input changes the estimated fair value in a way that's intuitive once you strip away the jargon.

For startup candidates, volatility is one of the most important ideas to grasp. A stable asset leaves less room for a dramatic increase. A company with a broad range of future outcomes gives the option more upside possibility.

That's one reason private company valuation gets tricky. Startups don't trade on public markets, so inputs aren't always clean. Some awards also include features that are awkward to capture in simpler models.

The practical takeaway isn't that you should calculate Black-Scholes by hand. It's that you should recognize which variables matter when a company talks about “fair value.”

What works is using these inputs to understand the direction of value.

What doesn't work is treating a valuation model like an oracle. The output is only as good as the assumptions, and private company assumptions are often the hard part.

What to remember: Models estimate fair value. They don't predict your future payout.

Candidates don't need perfect model precision. They need enough fluency to ask sharper questions and detect when an offer sounds attractive only because nobody has translated it into ownership, cost, and timing.

Public-company options are easier to reason about because the stock trades daily. Startup options are different because the company's current paper value, legal valuation, and future exit value can be far apart.

For candidate-level math, the most useful framework is the ownership method described in Secfi's guide to startup stock option value: In startup contexts, stock option value is best estimated by projecting the company's future valuation at exit, then multiplying the employee's ownership stake by that exit value and subtracting costs. For example, 1,000 options in a firm with 100 million shares outstanding equates to a 0.001% ownership stake; if the company's current valuation is $1 billion, the theoretical option value is $10,000 before deducting costs.

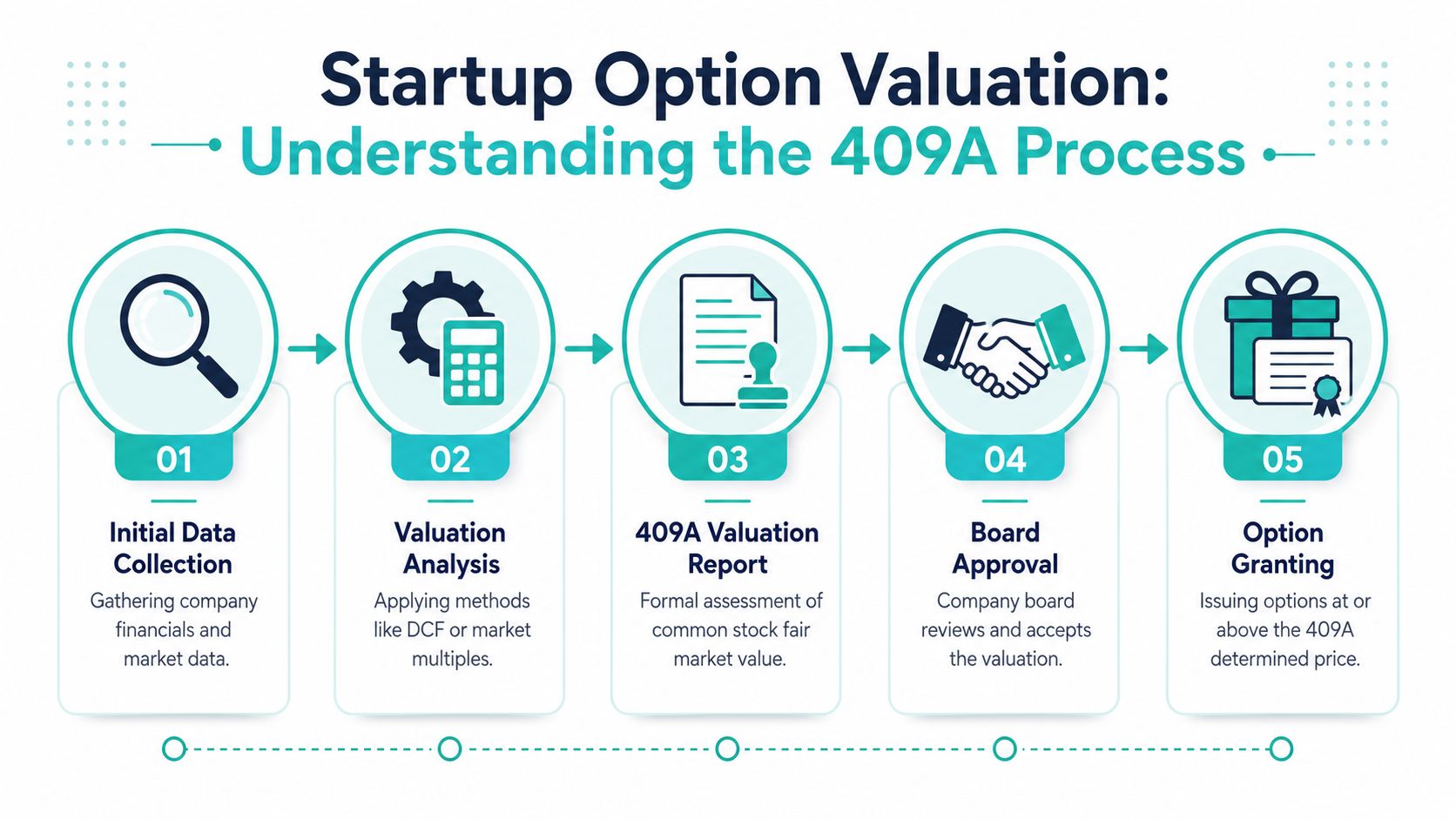

Most startup candidates eventually hear about the 409A valuation. In plain English, it's the company's formal estimate of common stock fair market value for setting option strike prices. It matters because it affects your exercise cost.

It does not tell you what your grant will be worth at exit.

That difference matters because a conservative common stock value used for compliance and a future acquisition or IPO outcome are solving different problems. One sets a defensible grant price. The other determines whether your options eventually turn into money.

If you want a grounded reference point for how private companies approach valuation work, firms that handle Everglow Prosperity valuation services can give useful context on the types of methods businesses use to assess value in less liquid settings.

Ownership today won't be your ownership forever. Future financing rounds, expanded option pools, and new hires usually dilute existing holders.

A pizza analogy works because it's literal. You may keep the same number of slices, but if the company keeps cutting the pizza into more slices, your percentage of the whole gets smaller.

This is why I push candidates to read about equity dilution before they anchor on a payout number. The grant can still be great. You just need to model a smaller future ownership percentage than the one on day one.

Use a three-part approach:

If you don't model dilution, you're usually valuing the grant as if the company will never raise money, never hire aggressively, and never expand the option pool. That's rarely how startups scale.

That's the hidden variable that changes “this could be worth a lot” into “this could be worth a lot, but probably less than the raw headline suggests.”

The cleanest way to evaluate an offer is to build a simple spreadsheet. Not a fancy cap table model. Just something that turns your grant into a range of outcomes.

I'd set up columns for ownership, a few exit cases, exercise cost, and estimated taxes. The point isn't to predict the future. The point is to stop thinking in vague upside language.

Start with the core company data:

If you want a candidate-friendly reference for the structure, a startup equity calculator guide is a good place to sanity-check the layout of your model.

Once the sheet is set up, create multiple exit scenarios. Don't force one “expected” outcome. Use a conservative case, a strong case, and a stretch case. Then haircut your ownership for dilution rather than pretending your day-one stake survives untouched.

The gross value is often the first number calculated. That's fine, but it's incomplete. The better question is what lands in your account after you pay to acquire the shares.

As Morgan Stanley's employee stock option explainer notes, costs to acquire options can significantly reduce net gains. Their example shows that if future gains total $30,000 but the cost to acquire shares is $5,000, the projected net gain is only $25,000 before taxes.

That's a small example, but the lesson scales. Exercise cost isn't bookkeeping noise. It directly changes whether an outcome feels meaningful.

I like to add a notes column with questions such as:

If you've ever looked at option payoff tools in public markets, something like the Rize Trade straddle tool can be a useful mental comparison for scenario thinking. It's built for a different type of option, but it reinforces the habit of mapping outcomes instead of staring at one headline number.

A good spreadsheet does something simple but powerful. It converts “20,000 options” from startup theater into a working estimate of personal wealth under several plausible futures. That's enough to negotiate intelligently.

Equity value on paper and money you keep after taxes are two different things. Candidates often spend all their energy on valuation and almost none on tax treatment, which is a mistake.

The first thing to know is that not all options are taxed the same way. Companies may grant ISOs or NSOs, and the timing of exercise can matter a lot. The detailed rules depend on your situation, and a tax advisor quickly earns their fee by clarifying these.

For many startup employees, the biggest practical tax choice isn't “Is this grant good?” It's “If this works, when should I exercise, and how long can I hold?”

That's where IRC Section 1202 enters the conversation. According to RBCX's discussion of startup stock option value and QSBS, IRC Section 1202 allows up to 100% of the gain, capped at $10M or 10x investment, to be excluded from federal taxes for Qualified Small Business stock, but it requires a 5-year holding period, creating a trade-off between liquidity and tax efficiency.

That's a massive difference in after-tax outcome if you qualify. It's also exactly the kind of detail that gets omitted when equity is discussed only in terms of strike price and headline upside.

The five-year hold requirement creates a real tension. You may want liquidity sooner. You may not want to commit capital early. You may not want to hold concentrated exposure to one startup for that long.

So the right question isn't “Can this become tax-advantaged?” The right question is “Does the path to that tax treatment fit my cash, risk tolerance, and timeline?”

A strong equity package can still be a poor personal decision if the exercise timing and holding requirements don't fit your finances.

Bring these questions into the conversation with your tax advisor and the company:

| Question | Why it matters |

|---|---|

| Are these ISOs or NSOs? | The tax treatment can differ materially |

| What's the current exercise cost? | You need to know how much capital is required to act |

| Could early exercise change my tax position? | Timing decisions can matter as much as headline grant size |

| Might QSBS treatment apply? | The after-tax difference can be significant if you qualify |

A startup grant only becomes personal wealth when the tax path is workable. Don't leave that part for later.

Most equity mistakes happen before you sign, not after. Candidates often accept startup options with less information than they'd require for a laptop purchase.

The biggest trap is being impressed by the option count. The second biggest is assuming the recruiter's excitement is the same thing as valuation clarity. It isn't. You need the denominator, the strike price, and context on the company's financing.

According to Jeffrey Bussgang's guidance on determining stock option value, to accurately assess the actual value of a stock option grant, an employee must obtain four specific data points from the company: the number of shares granted, the total number of fully diluted shares, the common stock strike price, and the preferred post-money valuation of the last financing round.

A few show up constantly:

If you want a broader plain-English resource on understanding trader income taxes, it can help sharpen your instincts on how tax treatment changes net results, even though startup equity has its own separate rules and complexities.

Bring direct questions to the hiring manager or recruiter. Not aggressive ones. Specific ones.

Ask for the data politely and matter-of-factly. Good companies expect strong candidates to care about this.

Negotiate from reasoning, not from buzzwords. Instead of saying “I want more upside,” say that you've modeled the grant against ownership, exercise cost, and likely dilution, and you'd like the equity package adjusted to better reflect the role.

That approach works because it signals maturity. You're not dazzled by option count. You understand how startup option valuation connects to personal wealth, and you're evaluating the package like an operator would.

The best candidates do this well. The best startups respect it.

If you're exploring startup roles and want to compare offers from companies that fit your background, Underdog.io makes that process much cleaner. One application puts you in front of vetted startups, and the conversations tend to start from real role fit, not random outbound noise.